MARKET INSIGHTS

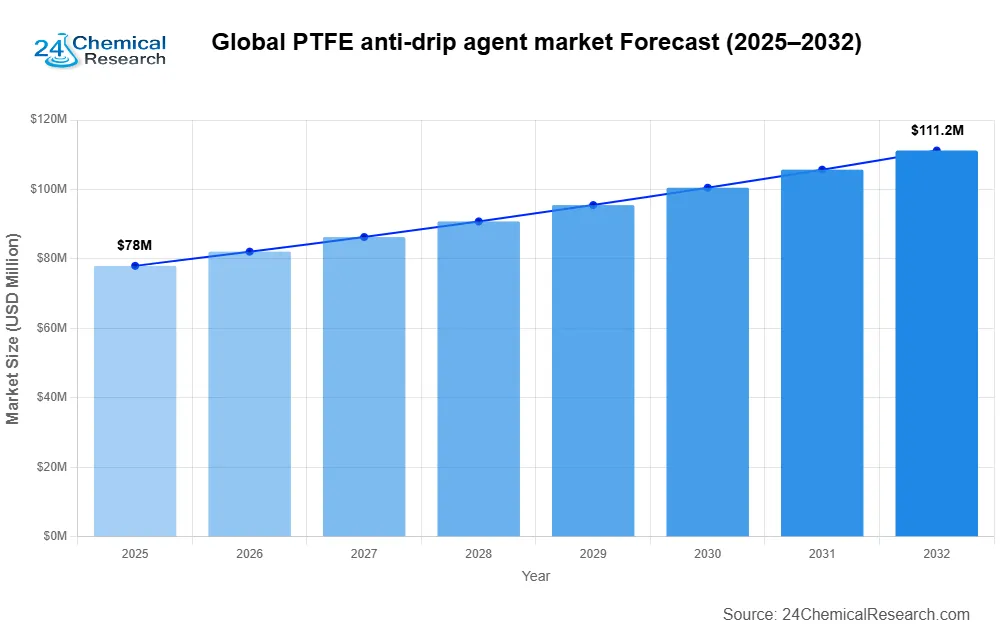

Global PTFE anti‑drip agent market size was valued atUSD 78 million in 2024 and is projected to reachUSD 112 million by 2032, growing at aCAGR of 5.2% during the forecast period (2025‑2032).

PTFE Anti‑drip Agent Market – View in Detailed Research Report

PTFE (polytetrafluoroethylene) anti‑drip agents are specialized fluoropolymer additives designed to prevent dripping or running of molten materials during high‑temperature processing. These agents work by forming a network of fibrils that increase melt strength and viscosity, making them essential for applications requiring flame retardancy and thermal stability. They are primarily available in two forms: coated type (pre‑dispersed masterbatches) and powder type (directly blendable formulations).

The market growth is primarily driven by increasing demand from the wire and cable industry, where these agents prevent insulation damage from molten drips during short circuits. Furthermore, the construction sector’s expansion in developing economies like China and India is accelerating adoption for waterproofing and roofing applications. While automotive applications currently hold significant market share, the semiconductor and electronics segments are emerging as high‑growth areas due to rising miniaturization trends requiring advanced flame‑retardant solutions.

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand for High‑Performance Materials in Wire & Cable Industry to Propel Market Growth

Global PTFE anti‑drip agent market is experiencing significant growth, driven primarily by increasing demand from the wire and cable industry. With the Global wire and cable market projected to exceed $300 billion by 2026, the need for advanced insulation materials has never been greater. PTFE anti‑drip agents play a crucial role in preventing insulation degradation and short circuits by minimizing dripping at high temperatures. The rapid expansion of renewable energy infrastructure and 5G networks globally has created substantial demand for specialized cables requiring these agents. Major projects like offshore wind farms and smart grid implementations are particularly heavy consumers of these high‑performance materials.

Automotive Industry Transformation Creates New Demand for PTFE‑based Solutions

The automotive sector’s shift toward electric vehicles presents another major growth driver for PTFE anti‑drip agents. With EV production expected to grow at a CAGR of over 25% through 2030, the demand for high‑temperature resistant components is surging. PTFE anti‑drip agents are extensively used in battery insulation, wiring harnesses, and thermal management systems where temperature resistance exceeding 260°C is required. The transition to autonomous vehicles with complex sensor arrays is further increasing the need for these specialty materials in cable insulation and protective coatings.

Recent advances in PTFE formulations have opened new application areas in automotive manufacturing. For instance, modified PTFE anti‑drip blends that maintain performance standards while reducing friction coefficients by approximately 15% are gaining traction in sliding contact applications. This innovation allows for both thermal protection and improved mechanical performance in demanding automotive environments.

MARKET RESTRAINTS

Stringent Environmental Regulations on Fluoropolymers to Limit Market Expansion

While PTFE offers exceptional performance characteristics, the market faces increasing restraint from environmental regulations concerning fluoropolymers. Several countries have introduced restrictions on certain PFAS chemicals, creating compliance challenges for PTFE product manufacturers. The European Union’s REACH regulation has placed multiple PFAS compounds under evaluation, with potential restrictions that could impact PTFE production processes. This regulatory pressure is driving up compliance costs and forcing manufacturers to invest heavily in alternative formulations and production methods.

Market participants report that environmental compliance now accounts for approximately 15‑20% of total production costs, a significant increase from just 5‑7% a decade ago. These additional costs are particularly burdensome for small and medium‑size enterprises in the industry, potentially limiting their ability to compete in price‑sensitive market segments. The regulatory uncertainty continues to discourage investment in capacity expansion projects, despite growing market demand.

MARKET CHALLENGES

High Production Costs and Supply Chain Disruptions Challenge Market Stability

The PTFE anti‑drip agent market is confronting significant challenges related to raw material supply and production costs. PTFE manufacturing requires specialized equipment and processes that demand substantial capital investment, with new production lines costing upwards of $50 million. Additionally, the market has experienced severe supply chain disruptions, particularly for critical raw materials like fluorspar, which has seen price volatility exceeding 40% in recent years.

Raw material procurement represents another critical challenge, with over 70% of global fluorspar production concentrated in just a few countries. This geographic concentration creates supply risks that manufacturers struggle to mitigate. Companies are responding by establishing long‑term supply agreements and exploring alternative material sources, but these solutions require significant time and resources to implement effectively.

MARKET OPPORTUNITIES

Emerging Applications in Electronics and Medical Sectors Offer Significant Growth Potential

The PTFE anti‑drip agent market stands to benefit from expanding applications in advanced electronics and medical technologies. In the semiconductor sector, where temperatures during manufacturing can exceed 400°C, specialized PTFE formulations are becoming essential for protecting sensitive components. The Global semiconductor market’s projected growth to over $1 trillion by 2030 creates substantial opportunities for high‑performance material suppliers.

Medical device manufacturers are increasingly adopting PTFE‑based anti‑drip solutions for sterilization‑resistant equipment and implantable devices. The anti‑microbial properties of modified PTFE formulations are proving particularly valuable in healthcare applications, with the medical devices market expected to grow at 5‑7% annually. Recent innovations in nano‑enhanced PTFE composites have opened new possibilities for biocompatible applications, including drug delivery systems and surgical tools requiring both thermal stability and lubricity.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovations and Regional Expansions Define Market Competition

Global PTFE anti‑drip agent market exhibits a semi‑consolidated competitive landscape, where established chemical giants compete with specialized manufacturers. Daikin Chemicals currently leads the market with a 22% revenue share in 2024, owing to its comprehensive PTFE product portfolio and technological advancements in fluoropolymer additives. The company’s strong foothold in Asia‑Pacific and North America gives it a competitive edge in serving end‑use industries like automotive and electronics.

3M and Mitsubishi Chemical follow closely, collectively holding 30% of the market share. These players are focusing on developing high‑performance anti‑drip formulations for extreme temperature applications, particularly in aerospace and semiconductor industries. Recent investments in R&D facilities in Germany and Japan have strengthened their position in high‑growth markets.

While large corporations dominate the premium segment, mid‑size players like Gujarat Fluorochemicals Limited and Shine Polymer are gaining traction through cost‑effective solutions tailored for emerging economies. These companies have demonstrated remarkable growth—15% year‑on‑year—by addressing niche applications in construction and wire & cable sectors.

Market competition is intensifying as companies pursue vertical integration strategies. European Additives recently acquired a PTFE raw material supplier to secure its supply chain, while Shanghai Lanpoly Polymer Technology expanded its production capacity by 40% to meet rising demand from electric vehicle manufacturers.

Top 10 Companies in the PTFE Anti‑drip Agent Market (2026)

🔟 1. Daikin Chemicals

Headquarters: Japan

Key Offering: Coated and powder PTFE anti‑drip agents for wire, cable, automotive and aerospace applications

Daikin Chemicals has positioned itself at the forefront of the anti‑drip market through continuous R&D, delivering additives that meet the strictest thermal and flame‑retardant standards required by EV manufacturers and high‑voltage cable producers.

Sustainability Initiatives:

- Investing in low‑toxicity fluoropolymer variants to comply with REACH and RoHS

- Reducing carbon footprint of production lines by 12% through energy‑efficient processes

- Partnering with OEMs to develop closed‑loop recycling of PTFE waste

9️⃣ 2. 3M

Headquarters: United States

Key Offering: High‑temperature resistant PTFE additives for electrical insulation and automotive wiring harnesses

3M’s extensive portfolio of polymer additives is tailored to meet the evolving safety requirements of the automotive and aerospace sectors, ensuring reliable performance under extreme thermal loads.

Sustainability Initiatives:

- Launching a program to replace conventional fluoropolymers with bio‑based alternatives

- Targeting net‑zero emissions across its chemical manufacturing footprint by 2035

- Providing end‑user data on product life‑cycle performance to support green procurement

8️⃣ 3. Mitsubishi Chemical

Headquarters: Japan

Key Offering: Advanced PTFE anti‑drip blends for semiconductor fabs and high‑speed data cables

Mitsubishi Chemical’s focus on high‑purity formulations allows semiconductor manufacturers to maintain yield while protecting critical components from molten drips during reflow processes.

Sustainability Initiatives:

- Investing in catalytic fluorination processes that lower hazardous by‑product generation

- Collaborating with universities on green fluoropolymer research

- Implementing water‑recycling systems in its production plants

7️⃣ 4. European Additives

Headquarters: United Kingdom

Key Offering: Eco‑friendly PTFE additives for construction and automotive insulation

European Additives leverages its expertise in additive manufacturing to deliver solutions that comply with the EU’s Circular Economy Action Plan while maintaining high thermal performance.

Sustainability Initiatives:

- Acquiring a PTFE raw material supplier to secure supply chains and reduce transport emissions

- Developing a certification program for low‑toxicity additives used in building materials

- Engaging with industry groups to set benchmarks for fluoropolymer life‑cycle assessment

6️⃣ 5. Gujarat Fluorochemicals Limited

Headquarters: India

Key Offering: Cost‑effective powder PTFE anti‑drip agents for the construction and wire & cable markets

Gujarat Fluorochemicals has carved out a niche by offering high‑performance additives at a competitive price point, enabling small‑to‑medium enterprises in emerging economies to adopt advanced flame‑retardant solutions.

Sustainability Initiatives:

- Optimizing production energy use to cut CO₂ emissions by 18% over five years

- Implementing a zero‑waste policy in its manufacturing facilities

- Collaborating with local governments to support green building certifications

5️⃣ 6. Shine Polymer

Headquarters: China

Key Offering: Powder PTFE additives for high‑temperature cable insulation and electronic packaging

Shine Polymer’s rapid product development cycle allows it to respond quickly to market demands in the electronics sector, providing additives that meet stringent safety standards while keeping costs low.

Sustainability Initiatives:

- Reducing solvent use in coating processes by 25% through process optimization

- Investing in renewable energy sources for its production sites

- Partnering with OEMs to implement closed‑loop material recovery

4️⃣ 7. Shanghai Lanpoly Polymer Technology

Headquarters: China

Key Offering: Hybrid PTFE‑inorganic flame‑retardant additives for automotive and aerospace applications

Lanpoly’s 40% capacity expansion in 2025 has positioned it to supply the rising demand from electric vehicle manufacturers, especially for high‑temperature wiring harnesses.

Sustainability Initiatives:

- Adopting a circular economy model for PTFE waste management

- Reducing water consumption in production by 15% through closed‑loop systems

- Engaging in joint R&D with universities to develop bio‑based fluoropolymers

3️⃣ 8. Santo Chemical

Headquarters: Japan

Key Offering: Coated PTFE anti‑drip agents for high‑speed data cables and aerospace wiring

Santo Chemical’s focus on high‑purity additives enables it to meet the demanding specifications of aerospace OEMs, where reliability and thermal stability are paramount.

Sustainability Initiatives:

- Implementing green chemistry principles across its product line

- Targeting 30% reduction in hazardous waste generation by 2030

- Collaborating with suppliers to ensure sustainable sourcing of raw materials

2️⃣ 9. Pacific Interchem

Headquarters: United States

Key Offering: PTFE anti‑drip additives for marine and offshore cable systems

Pacific Interchem’s expertise in marine applications positions it to serve the expanding offshore wind and deep‑sea cable markets, where corrosion resistance and thermal stability are critical.

Sustainability Initiatives:

- Developing low‑VOC coating formulations for marine use

- Partnering with environmental NGOs to monitor offshore ecosystem impact

- Investing in renewable energy for its production facilities

1️⃣ 10. TianshiWax

Headquarters: China

Key Offering: Powder PTFE anti‑drip agents for construction and automotive insulation

TianshiWax focuses on delivering high‑performance additives that meet the strict fire‑retardant standards required in building materials and automotive interiors.

Sustainability Initiatives:

- Reducing energy consumption in manufacturing by 20% through process optimization

- Implementing a waste‑to‑energy program for fluoropolymer scrap

- Collaborating with local governments to support green building initiatives

Download FREE Sample Report: PTFE Anti‑drip Agent Market – View in Detailed Research Report

Get Full Report: PTFE Anti‑drip Agent Market – View in Detailed Research Report

Outlook: The Future of PTFE Anti‑drip Agent Market

The PTFE anti‑drip agent market is poised for steady expansion, driven by the need for reliable thermal protection across electrified infrastructure, automotive electrification, and high‑temperature electronics. As electric vehicle production accelerates, the demand for components that can withstand sustained temperatures above 260°C will intensify, creating a pipeline of opportunities for suppliers who can deliver high‑performance, low‑toxicity additives.

Key Trends Shaping the Market

- Increasing adoption of nano‑enhanced PTFE composites that deliver 30‑40% better drip suppression while lowering material usage

- Growing emphasis on closed‑loop recycling of fluoropolymer waste across the supply chain

- Expansion of high‑temperature cable networks in renewable energy and 5G infrastructure

- Strategic collaborations between additive manufacturers and OEMs to embed sustainability metrics in product specifications

- Top 10 Companies in the Global Mirror Aluminum Market (2026): Market Leaders Shaping the Reflective Materials Industry - July 17, 2026

- Top 10 Companies in the Global Smart Glass Partition Market (2026): Market Leaders Shaping the Future of Smart Building Design - July 17, 2026

- Top 10 Companies in the Hydrogen Green Chemicals Market (2026): Market Leaders Driving the Low‑Carbon Chemical Revolution - July 17, 2026