MARKET INSIGHTS

Global ammonia aqueous market size was valued at USD 4.3 billion in 2025. The market is projected to grow from an estimated USD 4.5 billion in 2026 to USD 6.2 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 4.1% during the forecast period.

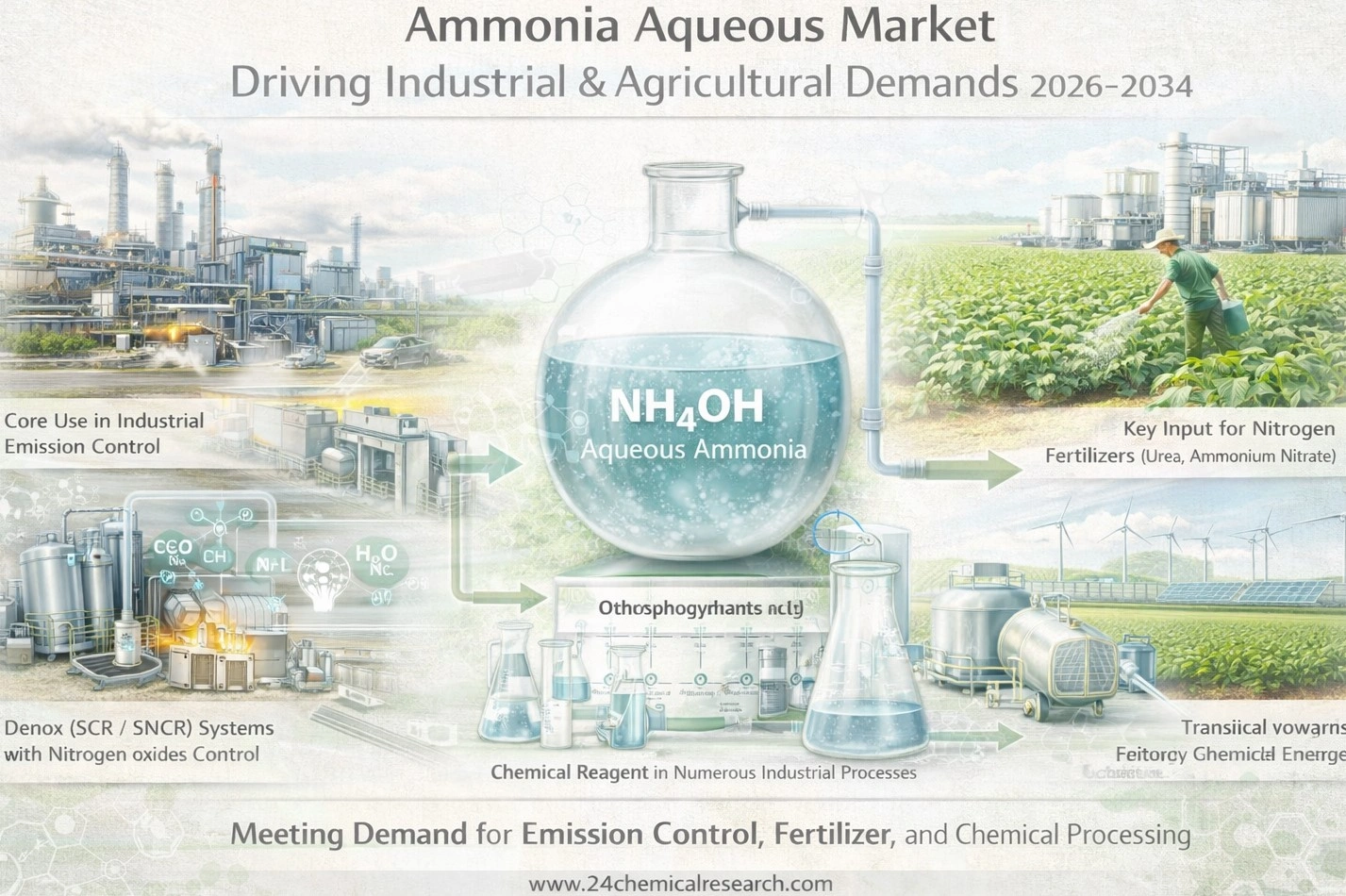

Ammonia aqueous, commonly known as ammonium hydroxide, is a solution of ammonia gas dissolved in water. This inorganic compound is a crucial industrial chemical characterized by its pungent odor and strong alkaline properties. It is produced in various concentration grades, including Industrial Grade, Electronic Grade, and Pharmaceutical Grade, to meet the stringent requirements of different applications. The versatility of ammonia aqueous makes it a fundamental feedstock and processing agent across numerous sectors.

The market’s steady growth is driven by its indispensable role in the agricultural sector as a source of nitrogen in fertilizers, which is critical for global food security. Furthermore, demand from the chemical industry for the production of various chemicals and its use in water treatment processes are significant contributors. However, the market faces challenges, including stringent environmental regulations concerning ammonia emissions and the handling of hazardous chemicals. Leading players such as Yara, CF Industries, and DuPont dominate the market, focusing on production capacity expansions and sustainable manufacturing practices to maintain their competitive edge and meet evolving global demand.

Ammonia Aqueous Market – View in Detailed Research Report

MARKET DRIVERS

Expanding Applications in Fertilizer Production

Global demand for food security remains a powerful driver for the ammonia aqueous market. As the world’s population continues to grow, the agricultural sector relies heavily on nitrogen-based fertilizers, for which aqueous ammonia is a key feedstock. The production of fertilizers like ammonium nitrate and urea consumes a significant portion of the global ammonia supply. This sustained demand from the agricultural industry provides a stable foundation for market growth.

Growing Utilization in Industrial Processes

Beyond agriculture, aqueous ammonia is indispensable in various industrial applications. It serves as a crucial reagent in water treatment plants for pH adjustment and chloramine formation. The chemical industry utilizes it in the production of numerous compounds, including nitric acid and various plastics. The expansion of manufacturing and infrastructure development, particularly in emerging economies, is fueling consumption in these sectors.

➤ The versatility of ammonia aqueous ensures its relevance across multiple, non‑cyclical industries, creating a resilient demand base.

Furthermore, advancements in refrigeration technology are creating niches for ammonia‑based systems. While safety regulations are stringent, the high efficiency and low environmental impact of ammonia as a natural refrigerant are driving its adoption in large‑scale industrial refrigeration, offering a growth avenue distinct from traditional chemical uses.

MARKET CHALLENGES

Stringent Health, Safety, and Environmental Regulations

The handling, storage, and transportation of aqueous ammonia present significant challenges due to its corrosive and toxic nature. Strict regulations govern its use to prevent accidental releases that could harm human health or the environment. Compliance with these regulations, such as those from occupational safety and environmental protection agencies, increases operational costs for producers and end‑users. These costs include investments in specialized storage tanks, safety equipment, and employee training programs.

Other Challenges

Volatility in Raw Material Costs

The production of ammonia aqueous is energy‑intensive, primarily relying on natural gas as a feedstock. Fluctuations in natural gas prices directly impact production costs, creating pricing instability in the market. This volatility makes budgeting and long‑term planning difficult for both manufacturers and their customers, affecting profit margins and competitive positioning.

Logistical and Handling Complexities

Transporting aqueous ammonia requires specialized infrastructure, including dedicated pipelines, tanker trucks, and railcars designed to handle corrosive materials. This logistical complexity adds to the overall cost and can limit market penetration in regions lacking the necessary infrastructure, creating supply chain bottlenecks.

MARKET RESTRAINTS

Environmental Concerns and the Green Transition

The conventional production of ammonia, known as grey ammonia, is a major source of carbon dioxide emissions. As global focus intensifies on decarbonization and achieving net‑zero targets, this carbon footprint acts as a significant restraint on the market. Pressure is mounting to shift towards green ammonia, produced using renewable energy, which currently involves higher production costs and is not yet available at the scale of traditional methods. This environmental scrutiny could potentially limit the growth of the conventional ammonia aqueous market in the long term.

Competition from Alternative Nitrogen Sources

The market faces competition from alternative nitrogen fertilizers and chemicals. For certain applications, products like urea ammonium nitrate (UAN) solutions or other solid fertilizers can be substituted for aqueous ammonia. The choice between these alternatives often comes down to factors like application efficiency, cost, and handling preferences, creating a competitive landscape that can restrain demand growth for aqueous ammonia specifically.

MARKET OPPORTUNITIES

Decarbonization and Green Ammonia Development

The very challenge of decarbonization presents the largest opportunity for market transformation. The development and scaling of green ammonia production create a massive new market segment. Green ammonia is not only a sustainable fertilizer but is also being explored as a carbon‑free fuel and an efficient hydrogen carrier. This dual role in energy and agriculture positions green aqueous ammonia for substantial growth, attracting significant investment in research and production facilities.

Precision Agriculture and Efficiency Gains

Advancements in precision agriculture are creating opportunities for more efficient and targeted use of aqueous ammonia. Technologies like soil sensing and variable‑rate application allow farmers to apply nitrogen fertilizers more precisely, reducing waste and environmental runoff. This efficiency can enhance the value proposition of aqueous ammonia, making it a more attractive option for modern, sustainable farming operations and potentially increasing its market share against less precise alternatives.

Top 10 Companies in the Ammonia Aqueous Market

1️⃣ Yara International

Headquarters: Oslo, Norway

Key Offering: Industrial‑grade ammonia aqueous for fertilizer production, high‑purity grades for pharmaceuticals and electronics

Yara’s global footprint in crop nutrition provides it with an entrenched position in the agricultural supply chain. Its ammonia aqueous production is integrated with large‑scale nitrogen fertiliser manufacturing, enabling cost efficiencies and rapid response to seasonal demand spikes.

Sustainability Initiatives:

- Investment in low‑emission ammonia synthesis plants

- Partnerships with farmers to implement precision fertilisation

- Commitment to carbon‑neutral operations by 2035

2️⃣ CF Industries Holdings, Inc.

Headquarters: Omaha, Nebraska, USA

Key Offering: Bulk ammonia aqueous for North American fertilizer markets, specialty grades for industrial applications

CF Industries’ extensive refinery network and strong logistics capabilities position it as the primary supplier of ammonia aqueous across the United States and Canada. The company’s focus on process optimisation has lowered production costs, allowing it to undercut competitors on price while maintaining margins.

Sustainability Initiatives:

- Deployment of renewable natural gas in ammonia synthesis

- Enhanced safety protocols to reduce accidental releases

- Research into ammonia‑based hydrogen carriers

3️⃣ DuPont de Nemours, Inc.

Headquarters: Wilmington, Delaware, USA

Key Offering: High‑purity ammonia aqueous for electronics, pharmaceuticals, and specialty chemicals

DuPont’s legacy in chemical innovation allows it to supply ammonia aqueous with stringent impurity controls, essential for semiconductor manufacturing and drug synthesis. Its integrated research and development pipeline keeps it ahead of emerging quality standards.

Sustainability Initiatives:

- Zero‑emission production lines for high‑purity grades

- Collaborations with semiconductor fabs to reduce water usage

- Investment in circular economy projects for ammonia waste recycling

4️⃣ Shandong Everlast AC Chemical Co., Ltd.

Headquarters: Shandong, China

Key Offering: Industrial‑grade ammonia aqueous for fertilizer and chemical feedstock, tailored grades for regional markets

Operating within China’s largest chemical cluster, Shandong Everlast benefits from proximity to raw‑material supplies and a dense network of downstream manufacturers. Its flexible production scheduling allows it to serve both bulk and specialty customers efficiently.

Sustainability Initiatives:

- Implementation of ammonia‑capture technology to reduce fugitive emissions

- Adoption of digital monitoring for process optimisation

- Community engagement programs focused on agricultural education

5️⃣ Hangzhou Hengmao Chemical Co., Ltd.

Headquarters: Hangzhou, China

Key Offering: Industrial and electronic‑grade ammonia aqueous for local manufacturing and export

Hengmao’s strategic location near major logistics hubs supports rapid distribution across East Asia. Its focus on product consistency has earned it a reputation for reliability among electronics manufacturers.

Sustainability Initiatives:

- Adoption of green ammonia pilot projects

- Investment in waste‑heat recovery systems

- Supply‑chain transparency through blockchain tracking

6️⃣ GAC (China)

Headquarters: Shanghai, China

Key Offering: Industrial ammonia aqueous for fertilizer production, high‑purity grades for specialty chemicals

GAC’s diversified portfolio and strong R&D base enable it to deliver ammonia aqueous that meets evolving regulatory standards. Its integrated logistics network ensures consistent supply to key industrial clusters.

Sustainability Initiatives:

- Carbon‑offset programs for ammonia production

- Development of low‑energy synthesis routes

- Partnerships with universities for green chemistry research

7️⃣ Malanadu Ammonia Private Limited

Headquarters: Kerala, India

Key Offering: Industrial ammonia aqueous for Indian fertilizer market, tailored grades for local chemical plants

As a domestic leader, Malanadu Ammonia leverages local natural gas supplies and an established distribution network to maintain competitive pricing against imported alternatives.

Sustainability Initiatives:

- Implementation of eco‑friendly storage solutions

- Collaboration with Indian agriculture ministries to promote efficient nitrogen use

- Community outreach on safe handling practices

8️⃣ KMG Chemicals, Inc.

Headquarters: San Francisco, California, USA

Key Offering: High‑purity ammonia aqueous for electronics and water treatment, specialty formulations for niche markets

KMG’s expertise in chemical purification positions it to supply ammonia aqueous that meets the tightest impurity specifications required by semiconductor fabs and pharmaceutical manufacturers.

Sustainability Initiatives:

- Zero‑liquid‑discharge processes

- Research into ammonia‑based green solvents

- Supplier certification for environmental compliance

9️⃣ Lonza Group AG

Headquarters: Basel, Switzerland

Key Offering: Ultra‑high‑purity ammonia aqueous for biopharmaceuticals, precision chemical synthesis

Lonza’s global presence in the life‑sciences sector ensures it can deliver ammonia aqueous that satisfies the most demanding purity standards, supporting advanced drug development pipelines.

Sustainability Initiatives:

- Closed‑loop production for high‑purity grades

- Investment in renewable energy for manufacturing sites

- Collaboration with biotech firms on green chemistry initiatives

🔟 FCI (USA)

Headquarters: New York, New York, USA

Key Offering: Industrial ammonia aqueous for chemical synthesis, specialty grades for industrial processes

FCI’s extensive network of chemical plants across North America enables it to supply ammonia aqueous at competitive volumes while maintaining stringent quality controls.

Sustainability Initiatives:

- Implementation of ammonia‑capture systems

- Energy‑efficiency upgrades across production facilities

- Stakeholder engagement on sustainable nitrogen management

Download FREE Sample Report

Ammonia Aqueous Market – View in Detailed Research Report

Get Full Report

Ammonia Aqueous Market – View in Detailed Research Report

🌍 Outlook: The Future of Ammonia Aqueous Market

The trajectory of the ammonia aqueous market reflects a balancing act between traditional industrial demand and a growing emphasis on sustainability. While the agricultural sector remains the backbone of consumption, the shift towards green ammonia and the integration of ammonia as a hydrogen carrier are reshaping the value chain. Companies that can combine cost‑effective production with low‑emission technologies are poised to capture the expanding green niche, while those that maintain strong ties to established fertilizer and chemical markets will continue to thrive in the short to medium term.

📈 Key Trends Shaping the Market

- Rapid adoption of precision fertilisation practices in agriculture

- Expansion of ammonia‑based refrigeration systems in industrial settings

- Strategic investments in green ammonia pilots across Asia and North America

- Digitalisation of supply chains to improve traceability and safety

- Emerging regulatory frameworks targeting ammonia emissions in the EU and China

- Top 10 Companies in the HDPE Geomembrane Market (2026): Market Leaders Driving Global Infrastructure - July 15, 2026

- Top 10 Companies in the Low Carbon Disinfectants Market (2026): Market Leaders Powering Sustainable Hygiene - July 15, 2026

- Top 10 Companies in the 2 Part Acrylic Adhesive Market (2026): Market Leaders Driving Advanced Bonding - July 15, 2026