MARKET INSIGHTS

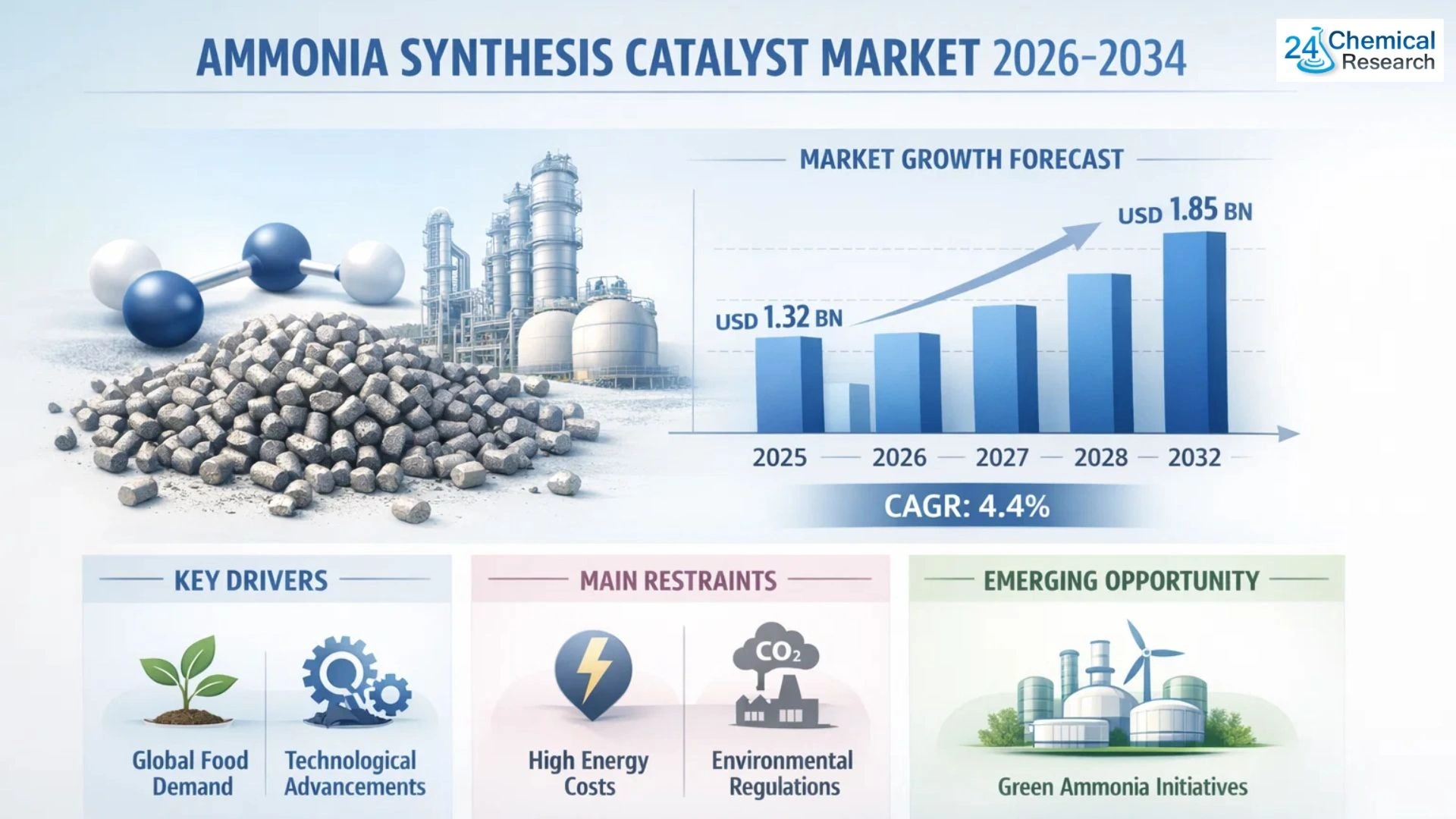

Global Ammonia Synthesis Catalyst market size was valued at USD 1.27 billion in 2024. The market is projected to grow from USD 1.32 billion in 2025 to USD 1.85 billion by 2032, exhibiting a CAGR of 4.4% during the forecast period.

Ammonia synthesis catalysts are specialized materials that accelerate the chemical conversion of nitrogen and hydrogen into ammonia through the Haber‑Bosch process. These catalysts predominantly use iron‑based formulations, though magnetite and other advanced materials are gaining traction. The catalysts play a critical role in industrial‑scale ammonia production, which is essential for fertilizers, chemicals, and emerging energy applications like green hydrogen storage.

The market growth is driven by increasing fertilizer demand to support global food production, coupled with investments in sustainable ammonia technologies. While traditional applications dominate, new opportunities emerge in energy storage where ammonia serves as a carbon‑free fuel. However, high production costs and stringent emissions regulations present challenges. Major players like BASF and Haldor Topsoe are investing in next‑generation catalysts to improve efficiency and reduce environmental impact, signaling strong future potential for innovation‑driven growth.

Ammonia Synthesis Catalyst Market – View in Detailed Research Report

MARKET DYNAMICS

MARKET DRIVERS

Global Food Security Demands to Accelerate Ammonia Catalyst Adoption

The persistent global population growth, projected to reach 9.7 billion by 2032, continues to exert tremendous pressure on agricultural systems. Ammonia‑based fertilizers remain indispensable for maintaining crop yields, with nitrogen fertilizers accounting for approximately 60% of total fertilizer consumption globally. This sustains strong demand for ammonia synthesis catalysts as over 80% of industrially produced ammonia is dedicated to fertilizer applications. Emerging economies are particularly active in expanding their agricultural output, with fertilizer consumption in regions like Southeast Asia growing at nearly 5% annually.

Technological Advancements in Catalyst Formulations Driving Efficiency

Significant R&D investments by industry leaders are yielding breakthrough catalysts with enhanced activity and longevity. Modern iron‑based catalysts now demonstrate 20‑30% greater efficiency compared to conventional formulations, while ruthenium‑based alternatives are achieving even higher performance metrics in specialized applications. These technological improvements directly translate to reduced energy consumption in ammonia plants, where catalyst performance can influence overall energy usage by 15‑20%. With the average ammonia plant consuming about 33 gigajoules per ton of product, even marginal efficiency gains generate substantial operational savings.

Furthermore, the development of cobalt‑promoted catalysts has opened new possibilities for low‑pressure synthesis, potentially revolutionizing small‑scale ammonia production. As sustainability becomes paramount, these innovations align perfectly with industry needs.

MARKET RESTRAINTS

High Energy Intensity of Ammonia Production Constrains Market Expansion

Ammonia synthesis remains one of the most energy‑intensive industrial processes, with conventional Haber‑Bosch plants requiring significant natural gas inputs. Energy costs frequently constitute 70‑90% of total production expenses, making the industry highly vulnerable to fuel price volatility. The recent global energy crisis demonstrated this sensitivity, with European ammonia production declining by nearly 40% during peak price periods. While catalysts can improve efficiency, they cannot entirely mitigate the fundamental energy requirements of the nitrogen fixation process.

Environmental Regulations Increasing Production Costs

Stringent emissions standards are compelling ammonia producers to invest heavily in pollution control systems, indirectly affecting catalyst markets. Modern environmental regulations now mandate CO₂ capture in many jurisdictions, adding 20‑30% to capital expenditures for new plants. While this drives demand for more efficient catalysts to offset costs, it simultaneously raises barriers to market entry. The transition to green ammonia production methods, though promising long‑term, currently requires substantial upfront investments that many operators find prohibitive without government support mechanisms.

MARKET OPPORTUNITIES

Green Ammonia Initiatives Creating New Catalyst Development Pathways

The emerging green ammonia sector presents transformative opportunities for catalyst innovation. Electrochemical ammonia synthesis, while currently accounting for less than 1% of global production, is projected to grow at over 60% annually through 2032. This rapidly evolving segment demands entirely new catalyst formulations optimized for renewable energy inputs and intermittent operation. Several major chemical companies have already established dedicated R&D programs, with pilot plants demonstrating promising results using novel catalyst‑electrode combinations.

Furthermore, the maritime sector’s decarbonization efforts are driving demand for ammonia as a marine fuel. The International Maritime Organization’s 2050 emissions targets could require 30‑40 million tons of clean ammonia annually by 2040, creating substantial catalyst demand. This emerging application is spurring innovation in catalyst durability and poison resistance to accommodate fuel‑grade specifications.

MARKET CHALLENGES

Supply Chain Vulnerabilities Impacting Rare Metal Availability

The ammonia catalyst industry faces growing material security concerns, particularly for ruthenium and cobalt used in advanced formulations. Nearly 85% of global ruthenium supply originates from just three countries, creating concentrated geopolitical risks. Recent supply chain disruptions have caused price fluctuations exceeding 300% for some platinum group metals. Such volatility complicates long‑term planning and may delay adoption of next‑generation catalysts despite their performance advantages.

Technological Transition Period Creates Market Uncertainty

The ammonia industry currently straddles traditional and emerging production methods, creating challenges for catalyst developers. While conventional Haber‑Bosch plants will dominate for the foreseeable future, the parallel development of electrochemical and bio‑catalytic routes introduces strategic complexities. Companies must balance immediate customer needs with long‑term R&D investments, requiring careful resource allocation. This transition period may temporarily slow catalyst innovation as manufacturers cautiously evaluate technology pathways.

Segment Analysis:

| Segment Category | Sub‑Segments | Key Insights |

|---|---|---|

| By Type |

|

Iron‑based catalysts hold dominant position due to widespread adoption and cost‑efficiency in large‑scale ammonia production. |

| By Process |

|

Haber‑Bosch process remains the primary application segment, accounting for majority of catalyst consumption globally. |

| By Application |

|

Fertilizer production drives majority demand as ammonia is a key raw material for nitrogen‑based fertilizers. |

| By End‑User |

|

Fertilizer companies constitute the largest consumer segment due to continuous agricultural demand. |

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Catalyst Manufacturers Invest in Innovation to Maintain Market Position

The global ammonia synthesis catalyst market is moderately concentrated, with established chemical giants and specialized catalyst producers competing for market share. BASF SE dominates the sector with its cutting‑edge magnetite‑based catalysts and extensive distribution network spanning Europe, Asia‑Pacific, and North America. The company recently expanded its Ludwigshafen production facility to meet growing ammonia demand in fertilizer applications.

Haldor Topsoe and Johnson Matthey collectively account for approximately 35% of the market share as of 2025, leveraging their proprietary catalyst formulations and decades of ammonia plant expertise. Their technological leadership in iron‑based catalysts continues to drive adoption across large‑scale industrial ammonia facilities.

Emerging players like Linqu Taifeng Chemical are gaining traction through cost‑competitive offerings, particularly in price‑sensitive Asian markets. Meanwhile, Clariant (Süd‑Chemie) has strengthened its position through strategic collaborations with ammonia producers to develop next‑generation catalysts with improved energy efficiency and longer operational lifespans.

List of Key Ammonia Synthesis Catalyst Manufacturers

-

BASF SE (Germany)

-

Haldor Topsoe A/S (Denmark)

-

Clariant AG (Switzerland)

-

Johnson Matthey PLC (UK)

-

Linqu Taifeng Chemical Co., Ltd. (China)

-

Umicore (Belgium)

AMMONIA SYNTHESIS CATALYST MARKET TRENDS

Green Ammonia Production Driving Catalyst Innovation

The global shift towards sustainable energy solutions is significantly impacting the ammonia synthesis catalyst market. With ammonia being a key component in fertilizers and emerging as a carbon‑free fuel, demand for efficient catalysts has surged. The green ammonia segment, produced using renewable energy‑powered electrolysis rather than traditional Haber‑Bosch processes, is projected to grow at 62% CAGR between 2024‑2032. This transition requires advanced catalysts capable of operating at lower temperatures and pressures while maintaining high conversion efficiency. Manufacturers are investing heavily in developing ruthenium‑based and nanostructured catalysts that reduce energy consumption by up to 30% compared to conventional iron catalysts.

Other Key Trends

Smart Catalyst Formulations

Advanced material science is revolutionizing catalyst compositions through machine learning‑driven molecular modeling. New formulations combining iron oxides with rare earth promoters (like cerium or lanthanum) show 15‑20% higher activity rates at moderate conditions. These smart catalysts self‑optimize their surface structures during operation, addressing the perennial challenge of thermal deactivation in ammonia plants. Major producers are integrating IoT sensors in catalyst beds to monitor real‑time performance metrics, enabling predictive maintenance cycles that extend catalyst life by 3‑5 years.

Regional Manufacturing Shifts Reshaping Supply Chains

Strategic localization of ammonia production is creating demand variations across regions. While China dominates with 31% of global catalyst consumption in 2024, Middle Eastern countries are emerging as high‑growth markets investing in mega ammonia projects. Europe’s focus on decarbonization is driving adoption of novel catalyst systems compatible with hydrogen‑based synthesis routes. The North American market, though mature, is seeing renewed activity due to government incentives supporting clean ammonia projects worth USD 12 billion announced through 2027. These geographical shifts are compelling catalyst manufacturers to establish regional production hubs and technical service centers.

Integration with Carbon Capture Technologies

Modern ammonia plants are increasingly being designed with integrated carbon capture systems, necessitating catalyst adaptations. New generation materials maintain stable performance despite CO₂ impurities in syngas streams, with some formulations showing 98% selectivity towards ammonia even with 5‑8% CO₂ concentrations. The development of bifunctional catalysts that simultaneously optimize ammonia synthesis and carbon capture could potentially reduce capital costs by 18‑22% for new facilities. This technological convergence positions ammonia as a critical vector in the emerging hydrogen economy while sustaining demand for specialized catalysts through 2032.

Regional Analysis: Ammonia Synthesis Catalyst Market

With over 1.4 billion people to feed, India and China’s fertilizer production heavily relies on ammonia synthesis catalysts. The region accounts for nearly 60% of global fertilizer consumption, creating sustained demand for efficient catalyst technologies.

Rapid industrialization across APAC is driving demand for ammonia in chemical manufacturing, particularly in China’s coal‑to‑chemicals sector and India’s growing petrochemical industry, both requiring high‑performance catalysts.

Local manufacturers are increasingly adopting magnetite‑based catalysts for their cost‑effectiveness, while multinational players are introducing advanced iron‑based formulations to improve process efficiency in existing ammonia plants.

While demand is strong, the market faces pressures from overcapacity in China’s fertilizer sector and tightening environmental regulations that require catalyst manufacturers to develop cleaner production methods. Additionally, price sensitivity among local buyers remains a persistent challenge.

North America

The North American ammonia synthesis catalyst market is characterized by technological sophistication and stable demand from the agricultural sector. The United States, with its extensive corn belt requiring nitrogen fertilizers, accounts for about 80% of regional demand. Recent developments include collaborations between catalyst manufacturers and ammonia producers to develop greener synthesis processes, particularly for blue and green ammonia projects in response to decarbonization initiatives.

Europe

Europe’s market is transitioning toward sustainable ammonia production, driving demand for specialized catalysts suitable for green hydrogen‑based processes. The EU’s commitment to carbon neutrality by 2050 is accelerating investments in catalyst technologies that can operate efficiently with renewable energy inputs. Germany and the Netherlands lead in adopting these advanced solutions, supported by strong chemical industry clusters and government incentives.

Middle East & Africa

This region is emerging as an important market due to large‑scale ammonia production facilities in Saudi Arabia, Qatar, and Morocco. The Middle East benefits from low‑cost natural gas feedstocks, while African nations are building ammonia capacity to support domestic agriculture. Both regions are attracting investments from global catalyst suppliers looking to expand their presence in these growth markets.

South America

Brazil dominates the South American market, with its vast agricultural sector driving consistent demand for ammonia‑based fertilizers. However, economic volatility and infrastructure limitations have slowed investment in new ammonia plants, leading to steady but moderate growth in catalyst demand. Recent focus has been on improving catalyst lifetimes to reduce operating costs for existing facilities.

Key Report Takeaways

- Steady Market Expansion – The ammonia synthesis catalyst market is projected to grow from USD 1.27 billion (2024) to USD 1.85 billion (2032) at a 4.4% CAGR, fueled by rising agricultural demand and green energy initiatives.

- Food Security & Technological Advancements – With global population reaching 9.7 billion by 2032, fertilizer demand remains the primary driver, while 20‑30% efficiency gains in modern catalyst formulations optimize production economics.

- Dual Application Growth – Traditional fertilizer production (80% of ammonia use) coexists with emerging energy storage applications, requiring specialized catalyst solutions for both sectors.

- Operational & Regulatory Challenges – Market faces 70‑90% energy cost exposure in production and stringent CO₂ capture mandates adding 20‑30% to new plant costs, testing industry profitability.

- Green Transition Opportunities – Electrochemical ammonia (projected 60% CAGR) and maritime fuel applications (30‑40 million tons by 2040) are driving catalyst innovation for renewable energy integration.

- Strategic Competition – Market leadership shared between BASF and Haldor Topsoe (≈35% combined share), with Chinese players accelerating through cost‑competitive magnetite catalysts in Asia’s growth markets.

Report Scope

This report presents a comprehensive analysis of the global and regional markets for Ammonia Synthesis Catalyst, covering the period from 2024 to 2032. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

-

Sales, sales volume, and revenue forecasts

-

Detailed segmentation by type and application

In addition, the report offers in‑depth profiles of key industry players, including:

-

Company profiles

-

Product specifications

-

Production capacity and sales

-

Revenue, pricing, gross margins

-

Sales performance

It further examines the competitive landscape, highlighting the major vendors and identifying the critical factors expected to challenge market growth.

As part of this research, we surveyed Ammonia Synthesis Catalyst companies and industry experts. The survey covered various aspects, including:

-

Revenue and demand trends

-

Product types and recent developments

-

Strategic plans and market drivers

-

Industry challenges, obstacles, and potential risks

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Ammonia Synthesis Catalyst Market?

-> Global Ammonia Synthesis Catalyst market was valued at USD 1.27 billion in 2024 and is projected to reach USD 1.85 billion by 2032, growing at a CAGR of 4.4% during 2025‑2032.

Which key companies operate in Global Ammonia Synthesis Catalyst Market?

-> Key players include BASF, Haldor Topsoe, Clariant (Süd‑Chemie), Johnson Matthey, Linqu Taifeng Chemical, and Umicore.

What are the key growth drivers?

-> Key growth drivers include rising demand for fertilizers, increasing agricultural production needs, and development of green ammonia technologies.

Which region dominates the market?

-> Asia‑Pacific leads in market share due to high agricultural demand, while Europe shows strong growth in sustainable ammonia production.

What are the emerging trends?

-> Emerging trends include development of low‑energy catalysts, integration of renewable energy in ammonia production, and increasing R&D in ruthenium‑based catalysts.

Ammonia Synthesis Catalyst Market – View in Detailed Research Report

Outlook

The ammonia synthesis catalyst market is undergoing a dynamic shift. While traditional fertilizers remain the primary driver, the rise of green ammonia and maritime fuel applications is reshaping demand. Manufacturers are investing heavily in advanced catalyst technologies to meet energy efficiency and regulatory requirements, positioning the market for steady growth at a 4.4% CAGR through 2032.

Future Trends

- Electrochemical ammonia synthesis projected at >60% CAGR, driving demand for novel catalyst‑electrode systems.

- Maritime decarbonization requiring 30‑40 million tons of clean ammonia by 2040, spurring durability‑focused catalyst development.

- Integration of AI and IoT for predictive catalyst maintenance, extending operational lifespans.

- Carbon capture‑enabled catalysts reducing capital costs by up to 22% in new plants.

- Geopolitical supply chain diversification to mitigate rare‑metal price volatility.

- Top 10 Companies in the Sustainable Supply Chain Inorganic Materials Market (2026): Market Leaders Powering Global Supply Chain Sustainability - June 29, 2026

- Top 10 Companies in the United States N-Formylmorpholine (NFM) Sales Market (2026): Market Leaders Driving Industrial Solvent Innovation - June 29, 2026

- Top 10 Companies in the Heat-treated Wheat Flour Market (2026): Market Leaders Driving Global Food Innovation - June 29, 2026