The Modified Aromatic Hydrocarbon Resin Market

Modified Aromatic Hydrocarbon Resin Market – View in Detailed Research Report

Modified Aromatic Hydrocarbon Resin Market – View in Detailed Research Report

MARKET INSIGHTS

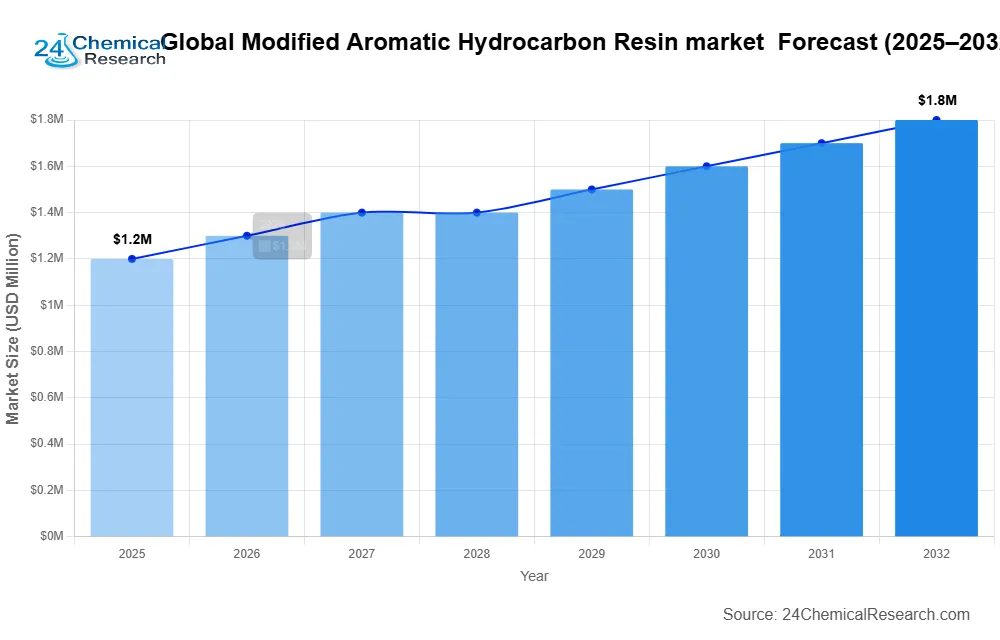

Global Modified Aromatic Hydrocarbon Resin market size was valued at USD 1.23 billion in 2024 and is projected to reach USD 1.78 billion by 2032, growing at a CAGR of 5.3% during the forecast period (2025‑2032). The U.S. market accounted for approximately 28% of global revenue in 2024, while China is expected to emerge as the fastest‑growing regional market with an estimated CAGR of 6.1% through 2032.

Modified aromatic hydrocarbon resins are specialized polymers derived from petroleum feedstocks that undergo chemical modification to enhance their adhesion, thermal stability, and compatibility properties. These synthetic resins primarily function as tackifiers and modifiers in industrial applications, improving the performance characteristics of end products across multiple industries. The product variants include C5 aliphatic, C9 aromatic, and hybrid formulations, each offering distinct viscosity and solubility profiles tailored for specific applications.

Market growth is being driven by expanding demand from the adhesives and sealants industry, which accounted for 42% of total consumption in 2024. The increasing adoption in road marking applications, particularly in emerging economies, is contributing significantly to market expansion. Furthermore, technological advancements in resin modification processes have enabled manufacturers to develop eco‑friendly variants with reduced volatile organic compound (VOC) emissions, aligning with stringent environmental regulations. Leading players like Eastman Chemical Company and Arakawa Chemical Industries are investing in capacity expansions to meet the growing demand from Asia‑Pacific markets.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Adhesives and Sealants Industry Accelerates Market Growth

Global adhesives and sealants industry, valued at over $60 billion, represents the largest application segment for modified aromatic hydrocarbon resins. These resins enhance key properties like tackiness, flexibility, and thermal stability in adhesive formulations. With construction activities rebounding post‑pandemic (global construction output projected to grow by 3.5% annually through 2030), demand for high‑performance adhesives in flooring, insulation, and panel bonding applications is surging. Recent innovations in pressure‑sensitive adhesives for automotive and packaging applications further drive resin consumption, with modified aromatic variants offering superior bonding strength compared to conventional alternatives.

Infrastructure Development Projects Fuel Demand for Road Marking Applications

Government investments in transportation infrastructure are creating substantial demand for modified aromatic hydrocarbon resins in road marking applications. The U.S. Infrastructure Investment and Jobs Act allocated $110 billion for roads and bridges, while China’s Belt and Road Initiative continues to drive asphalt modification requirements. These resins improve pavement markings’ durability and reflectivity, with performance enhancements of up to 30% in weather resistance compared to unmodified formulations. The global road marking materials market, growing at 5.8% CAGR, increasingly specifies modified aromatic resins for their balance of cost and performance.

Shift Toward Sustainable Packaging Solutions Creates New Growth Avenues

The packaging industry’s transition toward sustainable solutions presents significant opportunities for modified aromatic hydrocarbon resins. With the Global flexible packaging market expected to reach $270 billion by 2027, manufacturers are adopting these resins to develop recyclable hot melt adhesives for paper‑based packaging. Recent formulations demonstrate a 25% reduction in energy consumption during application while maintaining superior bond strength. Additionally, innovations in water‑based systems incorporating modified resins are addressing regulatory pressures on VOC emissions, particularly in North America and European markets with stringent environmental policies.

MARKET RESTRAINTS

Volatility in Raw Material Prices Impacts Profit Margins

The modified aromatic hydrocarbon resin market faces significant pressure from fluctuations in petrochemical feedstock costs. Crude C9 streams, a primary raw material, have experienced price variations exceeding 40% year‑over‑year due to geopolitical tensions and supply chain disruptions. This volatility challenges manufacturers’ ability to maintain stable pricing, particularly for long‑term contracts in the adhesives and coatings sectors. While forward pricing agreements provide some stability, the capital‑intensive nature of resin production limits flexibility in responding to sudden raw material cost increases.

Stringent Environmental Regulations Hinder Market Expansion

Increasing environmental regulations on aromatic compounds present growing challenges for market participants. The European Chemicals Agency’s REACH regulations have classified certain aromatic hydrocarbons as Substances of Very High Concern, requiring costly alternatives. Similar regulations in North America and Asia are pushing manufacturers toward complex reformulation processes, with development costs for compliant products ranging 20‑30% higher than conventional formulations. These regulatory hurdles are particularly impactful in the coatings sector, where evaporation during application triggers VOC emission concerns.

Competition from Alternative Resin Systems Limits Growth Potential

The market faces growing competition from bio‑based and hybrid resin systems that offer comparable performance characteristics. Polyterpene resins derived from pine chemicals are gaining traction in adhesive applications, with some formulations achieving 80‑90% renewable content. While modified aromatic resins currently maintain cost advantages in bulk applications, technological advancements in alternative systems combined with sustainability mandates are driving adoption shifts, particularly among environmentally conscious brand owners in consumer packaging applications.

MARKET OPPORTUNITIES

Development of High‑Performance Rubber Compounding Applications Presents Growth Potential

The rubber industry’s shift toward specialty applications creates significant opportunities for modified aromatic hydrocarbon resins. Tire manufacturers are increasingly adopting these resins to improve wet grip performance without compromising rolling resistance – a critical balance for electric vehicle tires where efficiency is paramount. Recent formulations have demonstrated 15% improvement in tread compound performance while meeting stringent EU tire labeling requirements. With the Global tire market projected to exceed 3 billion units annually by 2025, this application segment offers substantial expansion potential for resin producers.

Expansion in Emerging Markets Offers Untapped Potential

Rapid industrialization in Southeast Asia and Africa presents compelling growth opportunities for modified aromatic hydrocarbon resin manufacturers. Countries like Vietnam and Indonesia are experiencing double‑digit growth in adhesive and coating demand, driven by expanding manufacturing sectors and infrastructure development. Localized production facilities combined with strategic partnerships with regional distributors could capture this emerging demand, particularly as these markets increasingly adopt international quality standards for construction and industrial materials.

Technological Advancements in Resin Modification Processes Create Competitive Advantages

Innovations in catalytic polymerization and hydrogenation technologies enable producers to develop next‑generation modified aromatic resins with enhanced properties. Recent breakthroughs have yielded resins with 20% higher thermal stability while reducing undesirable odor characteristics – a critical factor in consumer packaging applications. These technological advancements allow manufacturers to command premium pricing in specialty applications while addressing evolving performance requirements in traditional end‑uses. Continued R&D investment in molecular weight control and functionality modification presents ongoing opportunities for product differentiation.

MARKET CHALLENGES

Supply Chain Vulnerabilities Impact Production Consistency

The modified aromatic hydrocarbon resin industry faces persistent supply chain challenges that disrupt production schedules and inventory management. Specialty chemical precursors often have limited supplier bases, with regional disruptions potentially causing months‑long lead time extensions. The 2023 Suez Canal congestion demonstrated these vulnerabilities, delaying shipments of key intermediates by up to six weeks. Manufacturers must balance just‑in‑time production efficiency with buffer stock requirements, increasing working capital needs by 15‑20% compared to pre‑pandemic levels.

Customer Consolidation Increases Pricing Pressure

Increasing consolidation among end‑user industries, particularly in the adhesives and coatings sectors, has significantly strengthened buyer power in negotiations. Large multinational customers now frequently demand annual price decreases despite raw material cost fluctuations, squeezing manufacturer margins. This trend is particularly pronounced in Europe and North America, where industry consolidation has reduced the number of significant buyers by approximately 30% over the past decade while increasing their purchasing volumes.

Technological Substitution Risks Threaten Long‑Term Demand

Emerging alternative technologies present long‑term challenges for traditional modified aromatic hydrocarbon resins. UV‑curable adhesive systems, while currently more expensive, offer faster processing speeds and eliminate VOC concerns. Initial adoption in electronics assembly and specialty packaging applications could expand to broader markets as costs decline. Manufacturers must actively invest in product innovation to maintain value propositions, with failure to adapt potentially leading to significant market share erosion in key application segments over the next decade.

Segment Analysis:

By Type

C9 Aromatic Resins Segment Leads the Market Due to Widespread Use in Adhesives and Coatings

The modified aromatic hydrocarbon resin market is segmented based on type into:

- C5 Aliphatic

- C9 Aromatic Resins

- Others

By Application

Adhesives Segment Dominates Owing to Increasing Demand from Construction and Automotive Industries

The market is segmented based on application into:

- Adhesives

- Packaging Tape

- Coating

- Road Asphalt

- Others

By End‑Use Industry

Construction Sector Drives Growth Due to Extensive Use in Adhesives and Coatings

The market is segmented based on end‑use industry into:

- Construction

- Automotive

- Packaging

- Printing Inks

- Others

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovations and Capacity Expansions Drive Market Competition

Global modified aromatic hydrocarbon resin market exhibits a moderately consolidated structure, with established chemical giants competing alongside regional specialists. Eastman Chemical Company and Arakawa Chemical Industries collectively commanded approximately 28% market share in 2024, owing to their vertically integrated production facilities and extensive distribution networks spanning North America, Europe, and Asia‑Pacific.

While Japanese players like Mitsui Chemicals dominate the high‑performance resin segment for automotive adhesives, American firms such as Neville Chemical Company lead in road‑marking applications. This geographic and application specialization creates pockets of intense competition within broader market segments.

Recent years have seen Chinese manufacturers like Qingdao Bater Chemical and Shanghai Qilong Chemical aggressively expand their production capacities. Their growth stems from cost‑effective manufacturing and government support for domestic specialty chemical production. However, these players face challenges in penetrating regulated Western markets that demand stringent quality certifications.

The competitive intensity is further heightened by ongoing R&D investments in bio‑based alternatives and low‑VOC formulations. Market leaders are actively acquiring smaller technology specialists – as seen in Rain Carbon’s 2023 acquisition of a German polymer additives producer – to bolster their innovation pipelines while neutralizing emerging threats.

List of Key Modified Aromatic Hydrocarbon Resin Manufacturers

- Eastman Chemical Company (U.S.)

- Arakawa Chemical Industries (Japan)

- Mitsui Chemicals (Japan)

- Neville Chemical Company (U.S.)

- Novotrade Invest AS (Norway)

- Qingdao Bater Chemical (China)

- Guangzhou ECOPOWER New Material (China)

- Rain Carbon Germany (Germany)

- Shanghai Qilong Chemical (China)

- Henghe Materials & Science Technology (China)

- Teckrez (U.S.)

- QINGDAO HWALONG CHEMICAL (China)

- Lesco Chemical Limited (Canada)

- Shandong Huike Petrochemical (China)

- Nanjing Yangzi Eastman Chemical (China)

MARKET TRENDS

Growing Demand in Adhesive and Sealant Applications to Emerge as a Key Trend

The increasing demand for high‑performance adhesives and sealants is driving significant growth in the modified aromatic hydrocarbon resin market. These resins enhance properties such as tackiness, durability, and heat resistance in adhesive formulations, making them indispensable in sectors like automotive, construction, and packaging. The packaging industry alone accounts for over 35% of Global resin consumption, propelled by rising e‑commerce activities and demand for protective packaging solutions. While traditional hydrocarbon resins remain widely used, modified variants are gaining traction due to their superior compatibility with rubber and polymer blends. Furthermore, stricter environmental regulations are pushing manufacturers to develop low‑VOC (volatile organic compound) resin solutions, accelerating innovation in this segment.

Other Trends

Sustainability and Bio‑based Alternatives

The shift toward sustainable materials is reshaping the modified aromatic hydrocarbon resin landscape, with bio‑based alternatives witnessing accelerated adoption. Although synthetic resins dominate the market with nearly 80% share, bio‑derived counterparts are projected to grow at a CAGR of 6.8% through 2032. Key players are investing in R&D to develop resins from renewable feedstocks like terpenes and rosin esters, which offer comparable performance while reducing carbon footprints. This trend aligns with global sustainability goals and responds to tightening regulations on petrochemical‑based products in regions like Europe and North America.

Technological Advancements in Road Construction Materials

Modified aromatic hydrocarbon resins are increasingly being utilized in road construction applications, particularly in polymer‑modified asphalt (PMA). These resins improve pavement elasticity and resistance to thermal cracking, extending road lifespans by 20–30% compared to conventional asphalt. The Asia‑Pacific region, where infrastructure development projects are surging, represents the fastest‑growing market for this application segment. China’s annual road construction investments alone exceed $150 billion, creating substantial demand for high‑performance asphalt modifiers. Additionally, cold‑mix asphalt technologies incorporating these resins are gaining popularity due to reduced energy consumption during installation. Market players are actively developing specialized resin grades to meet the evolving requirements of modern infrastructure projects.

Regional Analysis: Modified Aromatic Hydrocarbon Resin Market

North America

North America remains a mature yet steady market for modified aromatic hydrocarbon resins, primarily due to the region’s robust demand from adhesive and coating industries, which account for over 40% of consumption. The U.S., the largest market in the region, benefits from significant investments in infrastructure upgrades and stringent VOC regulations that promote the adoption of high‑performance, low‑emission resins. Major players like Eastman Chemical Company and Neville Chemical Company dominate supply chains with specialized formulations for automotive and construction sealants. However, the market faces pressure from rising raw material costs and competition from bio‑based alternatives gaining traction in sustainable packaging applications.

Europe

Europe’s market is shaped by rigid environmental policies under REACH and the Circular Economy Action Plan, driving innovation in water‑based and recyclable resin solutions. Germany and France lead demand, particularly for road‑marking and tire compounding applications. The region’s emphasis on closed‑loop manufacturing has compelled producers like Rain Carbon Germany to develop low‑carbon‑footprint variants. A notable trend is the shift from C9 aromatic resins toward blended C5/C9 products, offering balanced cost‑performance ratios for adhesives. Growth is tempered, however, by high energy costs and competition from Asian imports, pushing local manufacturers to focus on premium, high‑purity grades.

Asia‑Pacific

Accounting for over 50% of Global consumption, Asia‑Pacific is the fastest‑growing market, fueled by China’s booming adhesive and road construction sectors. Local production capacities are expanding rapidly, with Chinese firms like Shanghai Qilong Chemical increasing output by 8–10% annually. India’s packaging tape industry presents strong opportunities, though price sensitivity keeps demand skewed toward standard C9 resins. Japan remains a hub for high‑end electronic adhesives, with Mitsui Chemicals leading in halogen‑free resin development. Challenges include raw material supply volatility and fragmented local competition, but infrastructure growth across Southeast Asia ensures sustained demand.

South America

The region shows niche potential, with Brazil’s adhesive and asphalt modification sectors driving most demand. Modified resins are increasingly used in flexible packaging and footwear production, though economic instability slows investment in advanced formulations. Mexico benefits from near‑shoring trends, supplying resins to North American automotive OEMs. Limited local production capacity results in reliance on imports, particularly from the U.S. and Europe, creating opportunities for distributors. Market growth is further hindered by underdeveloped recycling infrastructure and fluctuating petrochemical feedstock prices.

Middle East & Africa

An emerging market with fragmented demand, the region sees growth in UAE‑based adhesive manufacturing and South Africa’s construction sector. GCC countries leverage low‑cost hydrocarbon feedstocks to attract resin investments, though most output is exported. Local consumption remains limited to basic road‑marking and rubber compounding applications due to underdeveloped downstream industries. While Saudi Arabia’s Vision 2030 promises industrialization‑led demand, progress is slow, with price competition from Asian imports restricting premium product adoption. However, strategic partnerships with global suppliers like Arakawa Chemical signal long‑term potential.

Report Scope

This report presents a comprehensive analysis of the Global Modified Aromatic Hydrocarbon Resin market, covering the period from 2024 to 2032. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

- Sales, sales volume, and revenue forecasts

- Detailed segmentation by type and application

In addition, the report offers in‑depth profiles of key industry players, including:

- Company profiles

- Product specifications

- Production capacity and sales

- Revenue, pricing, gross margins

- Sales performance

It further examines the competitive landscape, highlighting the major vendors and identifying the critical factors expected to challenge market growth.

As part of this research, we surveyed Modified Aromatic Hydrocarbon Resin manufacturers and industry experts. The survey covered various aspects, including:

- Revenue and demand trends

- Product types and recent developments

- Strategic plans and market drivers

- Industry challenges, obstacles, and potential risks

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Modified Aromatic Hydrocarbon Resin Market?

→ Global Modified Aromatic Hydrocarbon Resin market was valued at USD 1.23 billion in 2024 and is projected to reach USD 1.78 billion by 2032, growing at a CAGR of 5.3% during 2025‑2032.

Which key companies operate in Global Modified Aromatic Hydrocarbon Resin Market?

→ Key players include Arakawa Chemical Industries, Eastman Chemical Company, Mitsui Chemicals, Neville Chemical Company, Novotrade Invest AS, Qingdao Bater Chemical, and Guangzhou ECOPOWER New Material, among others.

What are the key growth drivers?

→ Key growth drivers include rising demand from adhesives and coatings industries, infrastructure development, and increasing applications in packaging tapes and road asphalt.

Which region dominates the market?

→ Asia‑Pacific is the largest and fastest‑growing market, while North America remains a significant revenue contributor.

What are the emerging trends?

→ Emerging trends include development of eco‑friendly resin formulations, technological advancements in production processes, and increasing adoption in specialty applications.

Download FREE Sample Report

Get Full Report

Outlook: The Future of Modified Aromatic Hydrocarbon Resin Market

The modified aromatic hydrocarbon resin market is poised for steady growth, driven by expanding demand in adhesives, road marking, and sustainable packaging. Technological innovation, capacity expansion, and strategic partnerships will be key enablers for players seeking to capture market share amid increasing regulatory scrutiny and supply chain volatility.

Future Trends Shaping the Market

- Rapid adoption of low‑VOC and bio‑based resin solutions to meet environmental regulations.

- Growth in high‑performance rubber compounding for electric vehicle tires.

- Expansion of polymer‑modified asphalt applications in emerging economies.

- Digitalization of supply chains and real‑time monitoring of resin performance.

- Strategic acquisitions of niche technology providers to bolster innovation pipelines.

- Top 10 Companies in the Global Oyster Peptide Market (2026): Market Leaders Powering the Emerging Protein Sector - August 9, 2026

- Top 10 Companies in the Bio‑Based Dyes Market (2026): Market Leaders Driving Sustainable Colour Solutions - August 9, 2026

- Top 10 Companies in the Electromagnetic Absorbers Market (2026): Market Leaders Powering Global Innovation - August 9, 2026