MARKET INSIGHTS

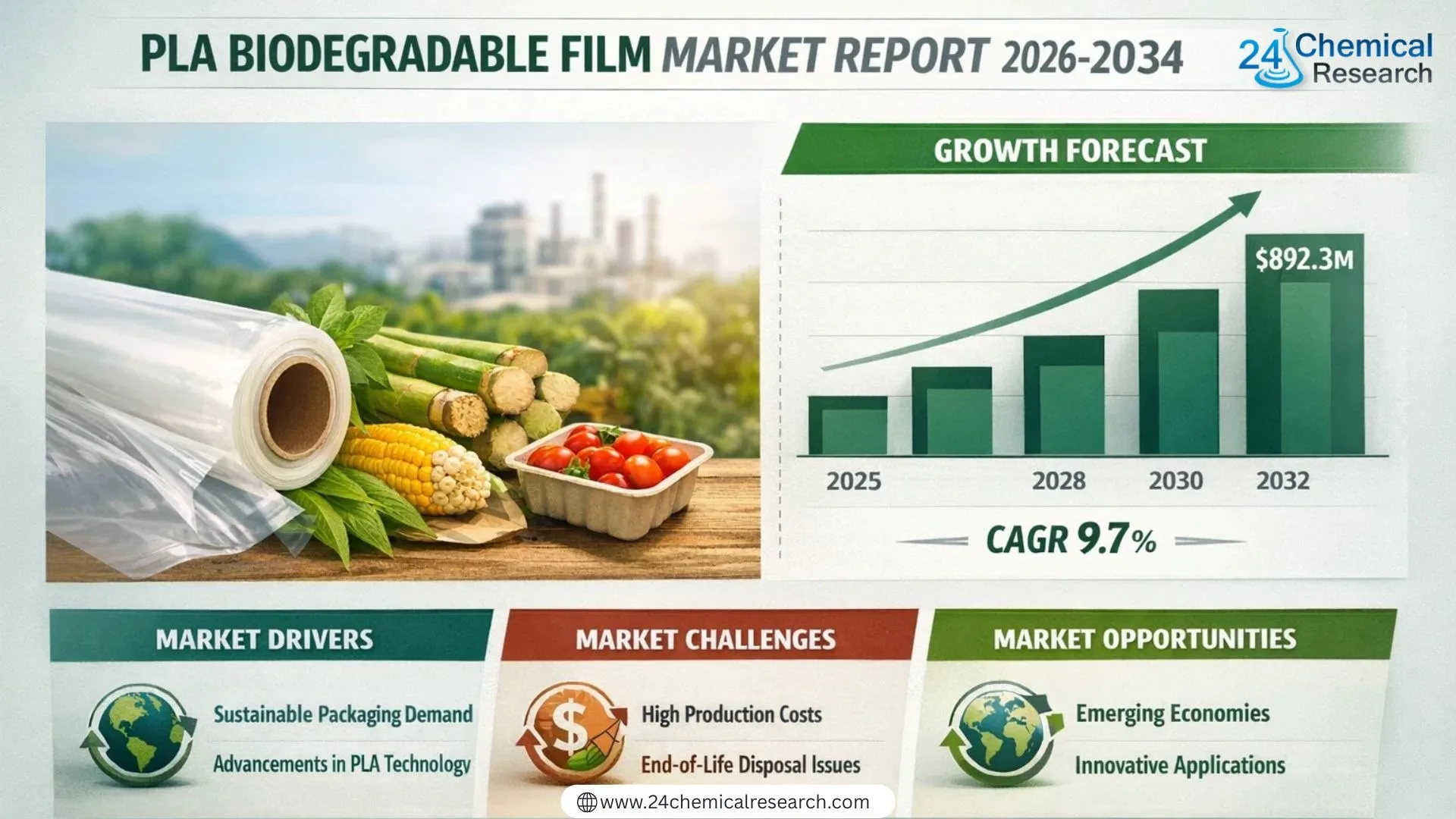

Global PLA biodegradable film market size was valued at USD 427.8 million in 2024. The market is projected to grow from USD 468.5 million in 2025 to USD 892.3 million by 2032, exhibiting a CAGR of 9.7% during the forecast period.

PLA (polylactic acid) biodegradable films are sustainable packaging solutions derived from renewable resources like corn starch or sugarcane. These films offer properties comparable to conventional plastics while being compostable under industrial conditions, making them crucial for circular economy initiatives. Common applications include food packaging, agricultural films, and personal care product wraps.

The market growth is driven by stringent plastic regulations worldwide and increasing consumer preference for eco-friendly packaging. However, higher production costs compared to conventional plastics remain a challenge. Key players like Amcor and Toray Industries are investing in R&D to improve film performance – Amcor recently launched a new high‑barrier PLA film variant in Q1 2024 for extended shelf‑life applications, demonstrating ongoing market innovation.

PLA Biodegradable Film Market – View in Detailed Research Report

MARKET DRIVERS

Global Push for Sustainable Packaging Solutions

Growing consumer awareness and stringent government regulations against single‑use plastics are compelling brands to adopt biodegradable alternatives. The PLA film market is a prime beneficiary of this shift, experiencing a compound annual growth rate (CAGR) projected to exceed 15% over the next five years. This demand is particularly strong in the food packaging and agriculture sectors, where the need for environmentally responsible materials is most acute. Legislation like the EU’s Single‑Use Plastics Directive is a significant catalyst, creating a non‑negotiable market driver.

Advancements in Material Performance

Technological improvements in polylactic acid (PLA) resin production have significantly enhanced the functional properties of PLA films. Modern formulations offer better clarity, tensile strength, and barrier properties against moisture and oxygen, making them a more viable substitute for conventional petroleum‑based films in a wider range of applications. Investment in research and development has led to the creation of high‑performance PLA blends that can compete effectively on durability and shelf‑life preservation.

➤ The expansion of composting infrastructure, particularly in North America and Europe, is a critical enabler, as it provides the necessary end‑of‑life pathway for PLA products to fulfill their biodegradable promise.

This infrastructure development, coupled with increasing brand commitments to sustainability goals, creates a powerful, self‑reinforcing cycle of demand and supply. Major corporations are publicly pledging to transition their packaging portfolios, directly fueling market growth.

MARKET CHALLENGES

High Cost and Production Limitations

Despite growing demand, PLA biodegradable film remains more expensive to produce than its traditional plastic counterparts, often costing 20‑50% more. This price disparity presents a significant barrier to widespread adoption, especially for cost‑sensitive applications. The primary challenge stems from the high cost of raw materials, primarily corn starch or sugarcane, and the complex fermentation and polymerization processes required. Furthermore, production capacity is still limited compared to the massive scale of conventional plastic film manufacturing, which can lead to supply chain constraints.

Other Challenges

Performance Under Specific Conditions

While performance has improved, standard PLA films can be sensitive to heat and moisture, limiting their use in certain applications like hot‑fill packaging or products requiring long‑term moisture barrier protection. This necessitates the development of more advanced, and often more expensive, copolymer blends.

End‑of‑Life Confusion

A major hurdle is consumer and waste management confusion. PLA requires industrial composting facilities to biodegrade effectively, and it does not break down in home compost systems or natural environments at a meaningful rate. Misplacement in recycling streams can contaminate other plastics, creating significant sorting and processing issues for recyclers.

MARKET RESTRAINTS

Competition from Other Bioplastics

The PLA biodegradable film market does not operate in a vacuum; it faces stiff competition from other bio‑based and biodegradable polymers like PHA (polyhydroxyalkanoates), PBAT (polybutylene adipate terephthalate), and starch blends. Each alternative has its own set of advantages, such as better biodegradability in various environments or superior mechanical properties. This competitive landscape forces PLA producers to continuously innovate and justify their market position, potentially restraining market share growth if they cannot keep pace with rival material advancements. Price competition among bioplastics themselves also exerts downward pressure on profit margins.

Volatility in Raw Material Supply

The dependence on agricultural feedstocks like corn introduces a layer of volatility linked to crop yields, weather patterns, and competing demand from the food and biofuel industries. Fluctuations in the price and availability of these raw materials can directly impact the stability of PLA film manufacturing costs and pricing, creating uncertainty for both producers and buyers. This agricultural link also subjects the market to geopolitical and trade policy risks that can disrupt supply chains.

MARKET OPPORTUNITIES

Expansion into Emerging Economies

As environmental awareness and regulatory frameworks mature in Asia‑Pacific and Latin American countries, immense growth opportunities emerge. These regions have large populations and rapidly growing packaging sectors, representing a largely untapped market for PLA films. Establishing local production facilities in these regions could also mitigate raw material and cost challenges by leveraging regional agricultural resources and reducing logistics expenses. Strategic partnerships with local players are key to navigating these new markets successfully.

Innovation in High‑Value Applications

Beyond standard packaging, there is significant potential for high‑margin, specialized applications. The medical and pharmaceutical industries present a promising avenue for PLA films used in drug delivery systems, surgical drapes, and biodegradable implants, where performance and biocompatibility are paramount. Similarly, the development of high‑barrier PLA films for premium food products and active packaging that extends shelf‑life can open up new, less price‑sensitive market segments. Continuous innovation in nanotechnology and polymer science is expected to unlock these advanced functionalities.

Segment Analysis:

| Segment Category | Sub‑Segments | Key Insights |

| By Type |

|

The 20‑40 Microns segment exhibits significant demand due to its versatility and suitability for a wide range of primary packaging applications, such as bags and overwraps, where a balance of strength, flexibility, and material efficiency is paramount. Thinner films are often preferred for their cost‑effectiveness and reduced environmental footprint per unit of packaging. The development of advanced extrusion technologies has enabled the production of high‑performance thin‑gauge PLA films that maintain excellent barrier properties, driving their preference in markets with stringent sustainability mandates. |

| By Application |

|

The Food & Beverage application leads the market, driven by a potent combination of consumer demand for sustainable packaging and regulatory pressures to reduce plastic waste. PLA films are extensively used for wrapping fresh produce, bakery items, and snack foods, offering clarity and adequate moisture barriers. The compatibility of PLA with existing packaging machinery and its certification for food contact make it a practical choice for brands seeking to enhance their environmental credentials. The segment’s growth is further propelled by innovations in compostable multilayer films that extend the shelf‑life of perishable goods. |

| By End User |

|

Brand Owners and Retailers are the predominant end‑users, as they are at the forefront of responding to consumer activism and regulatory demands for sustainable packaging solutions. Major consumer goods corporations and grocery chains are actively integrating PLA biodegradable films into their packaging portfolios to meet public commitments to reduce virgin plastic use. This segment’s influence is critical, as their sourcing decisions and specifications directly drive innovation and scale‑up in the supply chain, creating a pull‑effect that encourages converters to develop and offer a wider array of PLA film products. |

| By Distribution Channel |

|

Direct Sales (B2B) represents the dominant channel for PLA biodegradable film, as the product is typically a specialized industrial material sold in large volumes. Manufacturers establish direct relationships with large converters and major brand owners to provide customized solutions, technical support, and ensure supply chain reliability. This channel facilitates collaborative development of film specifications tailored to specific packaging lines and performance requirements. The complexity of product offerings and the need for consistent quality control make direct engagement the preferred model for securing large, long‑term contracts in this market. |

| By Degradation Profile |

|

Industrial Compostable films are the leading segment, as they align with established waste management infrastructure in many developed regions. These films are certified to break down completely in controlled composting facilities within a specific timeframe, offering a clear end‑of‑life solution. This profile is particularly attractive for food service packaging and items likely to be contaminated with food waste. The segment’s prominence is bolstered by growing municipal composting programs and the ability of industrial composting to handle a higher volume and variety of compostable materials reliably, providing a verifiable circular pathway for packaging waste. |

Competitive Landscape

Key Industry Players

A consolidated market led by global packaging giants and specialty material producers.

The global PLA Biodegradable Film market is moderately consolidated, with the top five players accounting for a significant portion of the global revenue as of 2023. Market leadership is held by a combination of global packaging corporations and specialized material science companies. Amcor plc, a global leader in packaging solutions, leverages its extensive R&D capabilities and global supply chain to offer a wide range of sustainable packaging options, including PLA‑based films. Similarly, Toray Industries, Inc. and DuPont de Nemours, Inc. bring their formidable expertise in advanced polymers and material science to the forefront, developing high‑performance PLA films for demanding applications. These established players compete on the basis of technological innovation, product performance, and the ability to serve multinational clients across diverse end‑markets like food and beverage packaging.

The competitive landscape also features several prominent niche and emerging players that focus on specific technologies or regional markets. Companies like BI‑AX International Inc. specialize in biaxially oriented films, offering specialized PLA film solutions. European firms such as Germany’s Bleher Folientechnik GmbH and the Netherlands‑based Polyesline B.V. are key regional manufacturers with strong technical expertise. A notable trend is the emergence of companies dedicated entirely to compostable packaging solutions, such as TIPA Corp., which offers fully compostable laminates. Other significant specialized manufacturers include Futamura, known for its cellulose‑based and compostable polymers, and Taghleef Industries, a major global producer of bi‑axially oriented films that has expanded into bio‑based offerings. These players often compete by addressing specific application needs, offering customized solutions, and capitalizing on regional regulatory drivers promoting biodegradable alternatives.

List of Key PLA Biodegradable Film Companies Profiled

-

Amcor plc (Switzerland/Australia)

-

Toray Industries, Inc. (Japan)

-

DuPont de Nemours, Inc. (USA)

-

Bleher Folientechnik GmbH (Germany)

-

BI‑AX International Inc. (Canada)

-

Plastic Union GmbH (Germany)

-

Polyesline B.V. (Netherlands)

-

TIPA Corp. (Israel)

-

Treofan Group (Germany)

-

Taghleef Industries LLC (UAE)

PLA Biodegradable Film Market Trends

Surging Demand Driven by Global Sustainability Mandates

The PLA biodegradable film market is experiencing robust growth, primarily propelled by stringent government regulations aimed at reducing single‑use plastic waste. Policies such as plastic bans and extended producer responsibility (EPR) frameworks in North America and Europe are compelling brands to adopt sustainable packaging solutions, directly increasing the adoption of PLA films. Concurrently, heightened consumer awareness and a strong preference for environmentally friendly products are creating sustained demand across end‑use industries, particularly in food packaging. The market is further advancing due to continuous innovation in material science, leading to improved film properties like better barrier performance and enhanced compostability, which are crucial for expanding application scope.

Other Trends

Expansion into High‑Growth Application Segments

A significant trend is the rapid expansion of PLA biodegradable films beyond traditional food packaging into new, high‑value applications. The personal care and cosmetics industry is increasingly utilizing these films for product wrappers and secondary packaging, aligning with brand sustainability goals. The agricultural sector is also emerging as a key growth area, with PLA films being used for mulch films and crop covers, offering a biodegradable alternative to conventional polyethylene. The 20‑40 microns segment is witnessing particularly strong growth due to its versatility and cost‑effectiveness for flexible packaging applications.

Regional Market Dynamics and Competitive Landscape

Market growth is geographically concentrated, with the Asia‑Pacific region projected to be the fastest‑growing market, fueled by large‑scale manufacturing capabilities in China and supportive government initiatives in countries like India and Japan. North America and Europe remain mature markets with high adoption rates driven by strict regulatory environments. The competitive landscape is characterized by the presence of both global players like Amcor and Toray Industries, and specialized manufacturers, who are focusing on capacity expansions, strategic collaborations, and new product development featuring advanced PLA blends to maintain market share and drive further innovation.

Regional Analysis: PLA Biodegradable Film Market

Europe’s Packaging and Packaging Waste Directive establishes strict biodegradability standards that favor PLA films over conventional plastics, creating a stable demand environment for compliant solutions.

European consumers demonstrate high awareness of sustainable packaging, with many retailers voluntarily switching to PLA films for fresh produce and bakery products to meet eco‑conscious buyer expectations.

The region hosts several PLA film technology leaders developing advanced barrier properties and printing compatibility, addressing previous limitations for broader commercial applications.

Well‑developed industrial composting facilities across Western Europe provide effective end‑of‑life solutions for PLA films, completing the sustainability value proposition demanded by regulators and consumers.

North America

North America represents the second largest market, driven by sustainability initiatives in food service packaging and agricultural applications. The U.S. sees growing adoption in premium food packaging segments, while Canada benefits from provincial bans on certain single‑use plastics. Retailers and brand owners are increasingly specifying PLA films to meet corporate sustainability targets. Flexible packaging converters are investing in PLA‑compatible equipment to serve this demand.

Asia‑Pacific

The Asia‑Pacific region shows the fastest growth potential, particularly in China and Japan where government policies promote biodegradable materials. China’s developing organic food market and e‑commerce packaging needs create opportunities. Japan leads in technical film applications for electronics packaging. Southeast Asian countries are emerging as manufacturing hubs for PLA films serving both domestic and export markets.

South America

South America exhibits moderate but growing adoption, with Brazil and Argentina leading market development. Food export requirements and domestic sustainability initiatives drive demand. The region benefits from local PLA resin production capacity, though film conversion infrastructure remains underdeveloped compared to other regions.

Middle East & Africa

This region shows nascent but promising growth, with UAE and South Africa as early adopters. Supermarkets and hospitality sectors are exploring PLA films for premium packaging applications. Market development is constrained by limited composting infrastructure and cost sensitivity, though regulatory changes may accelerate adoption.

Report Scope

This report presents a comprehensive analysis of the global and regional markets for PLA Biodegradable Film, covering the period from 2025 to 2032. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

- Sales, sales volume, and revenue forecasts

- Detailed segmentation by type and application

In addition, the report offers in‑depth profiles of key industry players, including:

- Company profiles

- Product specifications

- Production capacity and sales

- Revenue, pricing, gross margins

- Sales performance

It further examines the competitive landscape, highlighting the major vendors and identifying the critical factors expected to challenge market growth.

As part of this research, we surveyed PLA Biodegradable Film companies and industry experts. The survey covered various aspects, including:

- Revenue and demand trends

- Product types and recent developments

- Strategic plans and market drivers

- Industry challenges, obstacles, and potential risks

FREQUENTLY ASKED QUESTIONS:

What is the current market size of PLA Biodegradable Film Market?

-> The PLA Biodegradable Film Market was valued at USD 468.5 million in 2025 and is expected to reach USD 892.3 million by 2032, growing at a CAGR of 9.7% during the forecast period.

Which key companies operate in PLA Biodegradable Film Market?

-> Key players include Amcor, Toray Industries, DuPont, Bleher Folientechnik, BI‑AX International, Plastic Union, Polyesline, TIPA Corp., Treofan Group, and Taghleef Industries, among others.

What are the key growth drivers of PLA Biodegradable Film Market?

-> Key growth drivers include stringent plastic regulations worldwide, increasing consumer preference for eco‑friendly packaging, and corporate sustainability initiatives.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, driven by China’s rapid adoption, while Europe leads in regulatory adoption and market penetration.

What are the emerging trends?

-> Emerging trends include development of high‑barrier PLA films for extended shelf‑life applications, innovations in compostable packaging solutions, and increasing R&D investments by major players.

PLA Biodegradable Film Market – View in Detailed Research Report

Outlook: The Future of PLA Biodegradable Film is Cleaner and Smarter

The PLA biodegradable film market is undergoing a dynamic shift. While traditional plastics still dominate in volume, the industry is investing billions in low‑carbon alternatives, refining technologies, and expanding composting infrastructure.

📈 Key Trends Shaping the Market:

- Rapid expansion of composting facilities in North America and Europe, providing a clear end‑of‑life pathway.

- Regulatory push for 10–20% renewable content mandates by 2030, driving adoption of PLA films.

- Digitalization of supply chains and emissions tracking, enabling brands to prove sustainability claims.

- Strategic alliances between global packaging firms and bioplastic innovators, accelerating product development.

Get Full Report Here: https://www.24chemicalresearch.com/reports/268903/global-pla-biodegradable-film-forecast-market

- Top 10 Companies in the Phosphorus Pentasulfide Market (2026): Market Leaders Driving Global Demand - August 8, 2026

- Top 10 Companies in the Global 2‑Aminophenol Market (2026): Market Leaders Driving Chemical Innovation - August 8, 2026

- Top 10 Companies in the Sustainable Rubber and Plastics Market (2026): Market Leaders Powering Global Innovation - August 8, 2026