MARKET INSIGHTS

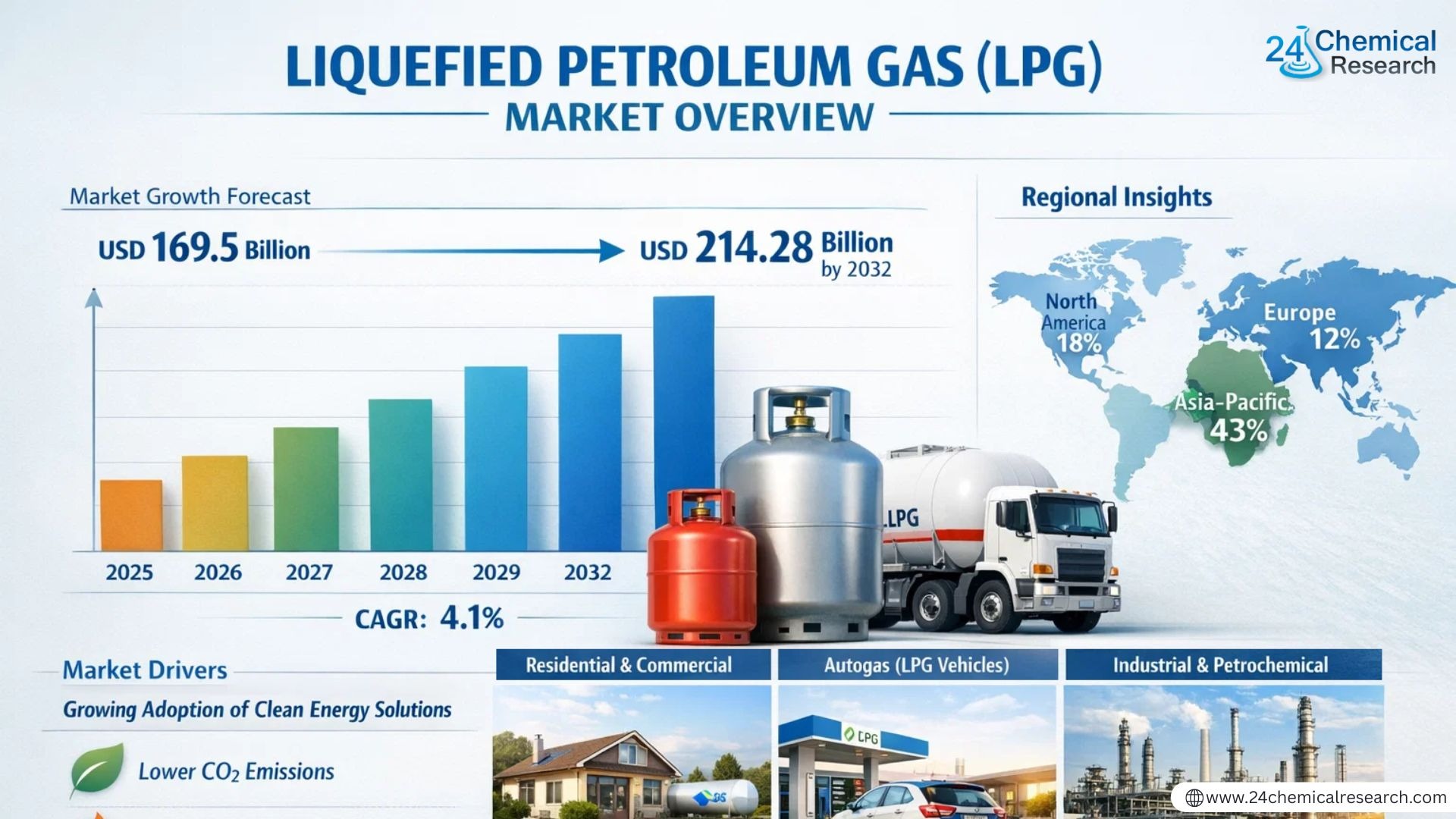

Global Liquefied Petroleum Gas (LPG) market size was valued at USD 162.67 billion in 2024. The market is projected to grow from USD 169.5 billion in 2025 to USD 214.28 billion by 2032, exhibiting a CAGR of 4.1% during the forecast period.

Liquefied Petroleum Gas (LPG) Market – View in Detailed Research Report

Liquefied Petroleum Gas (LPG) is a versatile energy source comprising flammable hydrocarbon gases, primarily propane and butane. These portable fuels are widely used in residential, commercial, and industrial applications, including heating, cooking, automotive fuel, and petrochemical feedstock. LPG offers significant advantages over traditional fuels due to its clean‑burning properties and high energy efficiency.

The market growth is driven by increasing urbanization, government initiatives promoting clean energy adoption, and rising demand for alternative fuel sources. Asia‑Pacific dominates the global market with a 43% share, while key players like Saudi Aramco, Sinopec, and ADNOC collectively hold about 25% market share. The Gas Purification Method segment leads production technologies with 62% market share, reflecting industry preferences for this cost‑effective approach. Meanwhile, civil applications account for 58% of consumption, underscoring LPG’s importance in household energy needs.

MARKET DYNAMICS

MARKET DRIVERS

Growing Adoption of Clean Energy Solutions to Propel LPG Market Expansion

The global shift toward cleaner energy sources is significantly driving the liquefied petroleum gas market. With increasing environmental concerns and stringent emission regulations, LPG has emerged as a preferred transitional fuel due to its lower carbon footprint compared to traditional fossil fuels. Recent data indicates that LPG produces up to 20% lower CO2 emissions than oil and 50% less than coal when used for heating applications. This environmental advantage positions LPG as a key component in national energy transition strategies across both developed and developing economies. Furthermore, government initiatives promoting clean cooking fuels in emerging markets are accelerating LPG adoption, particularly in regions where biomass remains the primary energy source.

Expanding Automotive Sector Utilization to Fuel Demand Growth

The automotive industry’s increasing adoption of LPG as an alternative vehicle fuel is creating substantial market opportunities. Known as autogas when used in vehicles, LPG offers cost savings of approximately 40% compared to gasoline while reducing harmful emissions by up to 15%. This economic and environmental benefit has driven autogas adoption across fleet operators, taxis, and private vehicles. Several countries have implemented favorable policies, including tax incentives and subsidies, to encourage autogas conversions. The European autogas market alone accounts for nearly 30% of global LPG consumption in transportation, demonstrating the sector’s significant contribution to overall market growth. Recent infrastructure developments, including expanded refueling networks, are further facilitating this transition.

Rural Electrification and Energy Access Programs Driving Emerging Market Growth

Government‑led energy access programs in developing nations are creating robust demand growth for LPG. Approximately 2.4 billion people worldwide still rely on traditional biomass for cooking, representing a massive untapped market for LPG distribution. Numerous national programs aim to replace hazardous cooking fuels with LPG cylinders through subsidy schemes and distribution network expansions. For instance, several South Asian and African countries have implemented cylinder recirculation models to improve accessibility in remote areas. These initiatives are expected to generate sustained demand growth as new consumer segments gain access to LPG for household use. The combination of public health benefits, reduced deforestation pressures, and improved energy security continues to drive policy support for LPG adoption in emerging economies.

MARKET CHALLENGES

Infrastructure Limitations and Distribution Challenges Constraining Market Potential

Despite strong demand fundamentals, the LPG market faces significant distribution and infrastructure hurdles. Many emerging markets lack adequate storage facilities, transportation networks, and cylinder distribution systems to support widespread adoption. The capital‑intensive nature of LPG infrastructure requires substantial upfront investment – a typical bulk storage facility costs approximately $5‑10 million depending on capacity. This financial barrier limits rapid market expansion in price‑sensitive regions where energy access is most needed. Furthermore, logistical challenges in remote areas increase final consumer costs, potentially pricing out lower‑income households despite subsidy programs.

Other Challenges

Price Volatility Impacting Consumer Adoption

LPG markets remain susceptible to global price fluctuations due to their connection to crude oil and natural gas markets. Recent geopolitical tensions have demonstrated how sudden price spikes can significantly impact affordability and adoption rates. When international LPG prices increase by just 10%, demand in price‑sensitive markets typically contracts by 3‑5%, illustrating the market’s sensitivity to cost considerations.

Competition from Alternative Energy Sources

The growing availability of renewable energy solutions and natural gas networks presents increasing competition for LPG in certain applications. While LPG maintains advantages in portability and infrastructure requirements, the long‑term threat from electrification and biogas solutions continues to influence market dynamics.

MARKET RESTRAINTS

Regulatory Complexities and Safety Concerns Limiting Market Expansion

Stringent safety regulations governing LPG storage, transportation, and usage present significant barriers to market growth. Compliance with diverse national and international standards requires substantial investment in safety systems and employee training programs. Recent changes in safety protocols, particularly following industrial accidents, have increased compliance costs by an estimated 15‑20% for market participants. This regulatory burden disproportionately affects smaller distributors and emerging markets where enforcement capabilities are developing. Furthermore, persistent public safety concerns regarding LPG cylinder use continue to influence consumer perception and adoption rates, despite significant improvements in container technology and safety mechanisms.

MARKET OPPORTUNITIES

Technological Innovations Creating New Application Areas

The development of advanced LPG technologies is unlocking new market opportunities across multiple sectors. Innovations in LPG refrigeration systems, power generation applications, and industrial processes are expanding the fuel’s usage beyond traditional heating and cooking applications. Emerging hybrid systems that combine LPG with renewable energy sources demonstrate particular promise, offering both environmental and operational benefits. The marine sector represents another growing opportunity, with LPG emerging as a transitional marine fuel that meets increasingly stringent emissions standards. These technological advancements are supported by ongoing research into bio‑LPG production methods, which could further enhance the fuel’s sustainability profile and market potential.

Strategic Partnerships Strengthening Market Position

Increasing collaboration between energy companies, distributors, and technology providers is creating robust opportunities for market expansion. Major players are forming strategic alliances to develop integrated energy solutions and expand distribution networks into underserved regions. These partnerships enable knowledge sharing, risk mitigation, and accelerated market penetration. Recent initiatives combining digital payment systems with LPG distribution illustrate how technological integration can improve accessibility and affordability in emerging markets. The growing focus on last‑mile distribution solutions and smart cylinder technologies further demonstrates the industry’s commitment to overcoming traditional market barriers through innovation and cooperation.

Segment Analysis:

By Type

Gas Purification Method Dominates Due to Higher Efficiency in Processing Natural Gas

The market is segmented based on type into:

-

Petroleum Cracking Method

-

Gas Purification Method

By Application

Civil Segment Leads the Market Owning to High Consumer Demand for Household Fuel

The market is segmented based on application into:

-

Civil

-

Industrial

-

Others

By End User

Residential Sector Holds Major Share Due to Widespread LPG Adoption for Cooking and Heating

The market is segmented based on end user into:

-

Residential

-

Commercial

-

Transportation

-

Industrial

COMPETITIVE LANDSCAPE

Key Industry Players

Oil & Gas Giants Dominate While Regional Players Expand Strategically

The global Liquefied Petroleum Gas (LPG) market exhibits an oligopolistic structure, where Saudi Aramco, Sinopec, ADNOC, CNPC, Exxon Mobil, and KNPC collectively control approximately 25% of market share as of 2024. These integrated energy companies leverage their upstream production capabilities and vast distribution networks to maintain market dominance, particularly in the Middle East and Asia‑Pacific regions where LPG demand is growing at 5.2% annually.

List of Major LPG Market Participants

-

Saudi Aramco (Saudi Arabia)

-

Sinopec (China)

-

ADNOC (UAE)

-

CNPC (China)

-

Exxon Mobil (U.S.)

-

KNPC (Kuwait)

-

Phillips66 (U.S.)

-

Bharat Petroleum (India)

-

TotalEnergies (France)

-

Chevron (U.S.)

LIQUEFIED PETROLEUM GAS (LPG) MARKET TRENDS

Expanding Applications in Emerging Economies Driving Market Growth

The global LPG market is witnessing robust growth, with emerging economies becoming key demand drivers. Asia‑Pacific, accounting for 43% of global consumption, is experiencing accelerated adoption due to urbanization and government‑led clean energy initiatives. With over 300 million metric tons (MMT) consumed globally in 2024, LPG has emerged as a transitional fuel in energy‑deficient regions where pipeline infrastructure remains underdeveloped. The affordability and portability of LPG cylinders make them indispensable across residential and commercial sectors, particularly in India and China, where campaign policies favor clean cooking solutions.

Other Trends

Shift Toward Sustainable Energy Alternatives

Environmental regulations are pushing industries toward cleaner energy sources, positioning LPG as a preferred fuel due to its lower carbon emissions compared to coal and diesel. Autogas (LPG for vehicles) has gained traction in Europe and parts of Asia, with countries like South Korea and Turkey leading adoption, supported by tax incentives. The industrial sector, which holds 38% of LPG applications, increasingly leverages it for feedstock in petrochemical production, notably for propylene and butylene derivatives. Additionally, the emergence of bio‑LPG, derived from renewable sources, reflects the industry’s commitment to decarbonization.

Technological Advancements in Storage & Distribution

Innovations in LPG logistics and storage are enhancing market accessibility, particularly in remote regions. Modular LPG plants and smart cylinder tracking systems optimize supply chain efficiency, reducing distribution gaps. The gas purification method, representing 62% of production globally, benefits from improved refining technologies that minimize impurities, making LPG safer for household use. Meanwhile, growing investments in small‑scale LNG and LPG terminals are addressing regional supply deficits, with Saudi Aramco, ADNOC, and CNPC collectively controlling 25% of the global supply to ensure steady availability. These infrastructure developments align with rising demand, projected to reach 214,280 million by 2032.

Regional Analysis: Liquefied Petroleum Gas (LPG) Market

North America

The North American LPG market, holding 18% of global share, demonstrates steady growth driven by shale gas production and widespread adoption in residential and commercial applications. The U.S., as the largest regional consumer, benefits from extensive pipeline infrastructure and government initiatives promoting cleaner fuels. While demand for autogas (LPG in vehicles) remains niche, the industrial sector leverages LPG for feedstock and heating due to competitive pricing against natural gas. However, market growth faces headwinds from electrification trends in home heating and increasing renewable energy adoption. Key players like Exxon Mobil and Chevron continue strengthening supply chains to meet regional demand.

Europe

Europe’s LPG market, currently representing 12% of global consumption, is shaped by stringent EU environmental policies and decarbonization targets. Countries like Germany and France prioritize LPG as a transitional fuel for off‑grid heating, with subsidized cylinder exchange programs boosting rural adoption. The maritime sector’s shift toward low‑sulfur fuels presents new opportunities for LPG bunkering, particularly in Nordic countries. However, market growth faces constraints from high taxation on LPG compared to natural gas and ambitious biogas substitution plans. Strategic investments by TotalEnergies and SHV Energy in bio‑LPG production aim to align the fuel with Europe’s net‑zero ambitions.

Asia‑Pacific

Dominating 43% of global LPG volume, the APAC region exhibits the highest growth potential, led by China and India’s expanding urban populations. Government initiatives like India’s PMUY (Pradhan Mantri Ujjwala Yojana), which distributed over 90 million LPG connections, have transformed energy access. China’s petrochemical sector drives industrial demand, while Southeast Asian nations increasingly adopt LPG for cooking to reduce deforestation. Despite this growth, price volatility and inconsistent distribution networks in emerging economies pose challenges. Regional producers (Sinopec, CNPC) and Middle Eastern exporters compete fiercely in this price‑sensitive market through long‑term supply agreements.

South America

South America’s LPG market thrives due to widespread residential use in countries like Brazil, where it serves as the primary cooking fuel for over 70% of households. Argentina and Chile demonstrate growing autogas adoption, supported by favorable taxation policies. The region benefits from proximity to U.S. and local production (Pemex, Petrobras), but economic instability often leads to subsidy reductions that depress demand. Venezuela’s refining capacity collapse has created supply gaps filled by regional imports. Infrastructure limitations in Andean nations hinder market expansion, though Brazil’s ongoing gas network developments signal long‑term growth potential.

Middle East & Africa

The MEA region presents a bifurcated market: Gulf Cooperation Council (GCC) countries lead production (Saudi Aramco, ADNOC), while Sub‑Saharan Africa shows untapped demand. Africa’s LPG adoption is accelerating through World Bank‑backed clean cooking initiatives, though per‑capita consumption remains low at ~3kg annually versus the global average of 25kg. The Middle East’s industrial demand grows alongside petrochemical expansions, particularly in Saudi Arabia’s Jubail Industrial City. Distribution challenges persist in Africa due to inadequate cylinder circulation systems, while Middle Eastern nations prioritize exports over domestic consumption despite government‑led residential conversion programs.

Report Scope

This report presents a comprehensive analysis of the global and regional markets for Liquefied Petroleum Gas (LPG), covering the period from 2024 to 2032. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

-

Sales, sales volume, and revenue forecasts

-

Detailed segmentation by type and application

In addition, the report offers in-depth profiles of key industry players, including:

-

Company profiles

-

Product specifications

-

Production capacity and sales

-

Revenue, pricing, gross margins

-

Sales performance

It further examines the competitive landscape, highlighting the major vendors and identifying the critical factors expected to challenge market growth.

As part of this research, we surveyed Liquefied Petroleum Gas (LPG) manufacturers, suppliers, and industry experts. The survey covered various aspects, including:

-

Revenue and demand trends

-

Product types and recent developments

-

Strategic plans and market drivers

-

Industry challenges, obstacles, and potential risks

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Liquefied Petroleum Gas (LPG) Market?

-> The global LPG market was valued at USD 162.67 billion in 2024 and is projected to reach USD 214.28 billion by 2032, growing at a CAGR of 4.1% during the forecast period.

Which key companies operate in Global Liquefied Petroleum Gas (LPG) Market?

-> Key players include Saudi Aramco, Sinopec, ADNOC, CNPC, Exxon Mobil, and KNPC, which collectively hold about 25% of the global market share.

What are the key growth drivers?

-> Key growth drivers include rising demand for clean energy, increasing adoption in residential and industrial applications, and government initiatives promoting LPG as an alternative fuel.

Which region dominates the market?

-> Asia‑Pacific is the largest market, accounting for 43% of global LPG consumption, while North America holds an 18% share.

What are the emerging trends?

-> Emerging trends include expansion of LPG infrastructure, growing automotive applications, and increasing focus on bio‑LPG production.

🔟 1. Saudi Aramco

Headquarters: Dhahran, Saudi Arabia

Key Offering: LPG Production, Distribution, LNG Export

Saudi Aramco remains the world’s largest oil producer, leveraging its vast upstream assets to secure a leading position in LPG supply. The company’s integrated refining and petrochemical complexes enable efficient gas purification and high‑quality LPG output for domestic and international markets.

Sustainability Initiatives:

- Investment in carbon capture and storage (CCS) for LPG facilities

- Partnerships with global utilities to expand LPG distribution networks in emerging economies

- Commitment to reducing methane emissions across the supply chain by 30% by 2030

Download FREE Sample Report: Liquefied Petroleum Gas (LPG) Market – View in Detailed Research Report

9️⃣ 2. Sinopec

Headquarters: Beijing, China

Key Offering: LPG Refining, Petrochemical Feedstock

Sinopec’s extensive refining network positions it as a major LPG producer in Asia. The company focuses on gas purification technologies that enhance product purity and reduce impurities, supporting clean cooking initiatives across China and neighboring countries.

Sustainability Initiatives:

- Development of bio‑LPG projects to diversify renewable fuel mix

- Implementation of smart cylinder tracking to improve distribution efficiency

- Reduction of flaring and venting through advanced gas capture systems

Download FREE Sample Report: Liquefied Petroleum Gas (LPG) Market – View in Detailed Research Report

8️⃣ 3. ADNOC

Headquarters: Abu Dhabi, UAE

Key Offering: LPG Production, LNG Export

ADNOC’s strategic investments in gas purification and storage infrastructure support the UAE’s goal of becoming a leading LPG exporter in the Middle East. The company’s modern bulk storage facilities ensure consistent supply to regional and global markets.

Sustainability Initiatives:

- Deployment of low‑emission LPG plants across the Gulf region

- Collaboration with local governments to expand LPG distribution in rural communities

- Adoption of digital payment platforms for cylinder sales to enhance consumer accessibility

Download FREE Sample Report: Liquefied Petroleum Gas (LPG) Market – View in Detailed Research Report

7️⃣ 4. CNPC

Headquarters: Beijing, China

Key Offering: LPG Refining, Petrochemical Feedstock

CNPC’s large refining footprint and advanced gas purification capabilities position it as a key LPG supplier in China and export markets. The company focuses on enhancing product purity to meet stringent safety and environmental standards.

Sustainability Initiatives:

- Investment in renewable LPG projects to support China’s clean‑energy targets

- Implementation of smart cylinder logistics to reduce distribution gaps

- Participation in international carbon reduction agreements

Download FREE Sample Report: Liquefied Petroleum Gas (LPG) Market – View in Detailed Research Report

6️⃣ 5. Exxon Mobil

Headquarters: Irving, Texas, USA

Key Offering: LPG Production, LNG, Autogas

Exxon Mobil’s diversified energy portfolio includes significant LPG production and distribution. The company is expanding its autogas fleet to support global transportation electrification trends, offering cost‑effective and low‑emission alternatives for fleet operators.

Sustainability Initiatives:

- Investment in carbon‑neutral LPG projects and bio‑LPG research

- Deployment of advanced gas purification technologies to enhance product quality

- Commitment to reducing overall greenhouse gas emissions by 30% by 2035

Download FREE Sample Report: Liquefied Petroleum Gas (LPG) Market – View in Detailed Research Report

5️⃣ 6. KNPC

Headquarters: Kuwait City, Kuwait

Key Offering: LPG Production, LNG Export

KNPC’s focus on efficient gas purification and large‑scale storage facilities supports the Gulf’s growing LPG demand. The company’s integrated supply chain ensures timely delivery to domestic and international markets.

Sustainability Initiatives:

- Deployment of low‑emission LPG plants to reduce carbon footprint

- Partnerships with local distributors to improve last‑mile delivery in remote areas

- Investment in digital monitoring systems for safety and efficiency

Download FREE Sample Report: Liquefied Petroleum Gas (LPG) Market – View in Detailed Research Report

4️⃣ 7. Phillips66

Headquarters: Houston, Texas, USA

Key Offering: LPG Refining, Distribution

Phillips66’s robust refining network and strategic partnerships enable it to supply high‑quality LPG across North America and emerging markets. The company is expanding its distribution channels to reach underserved regions.

Sustainability Initiatives:

- Investment in energy‑efficient refining technologies to reduce emissions

- Collaboration with local utilities to enhance LPG accessibility in rural areas

- Development of smart cylinder tracking for improved supply chain transparency

Download FREE Sample Report: Liquefied Petroleum Gas (LPG) Market – View in Detailed Research Report

3️⃣ 8. Bharat Petroleum

Headquarters: New Delhi, India

Key Offering: LPG Bottling, Distribution

Bharat Petroleum’s expansion of LPG bottling capacity supports India’s PM Ujjwala Yojana program, delivering clean cooking fuel to millions of households. The company’s focus on efficient logistics and safety standards ensures reliable supply across the sub‑continent.

Sustainability Initiatives:

- Expansion of LPG bottling plants to increase domestic supply

- Implementation of safety training programs for distribution personnel

- Partnerships with local NGOs to promote clean cooking practices

Download FREE Sample Report: Liquefied Petroleum Gas (LPG) Market – View in Detailed Research Report

2️⃣ 9. TotalEnergies

Headquarters: Paris, France

Key Offering: LPG Production, Bio‑LPG Projects

TotalEnergies is advancing its bio‑LPG initiatives in partnership with SHV Energy, positioning itself as a leader in sustainable LPG solutions. The company’s integrated energy portfolio supports both conventional LPG supply and renewable alternatives.

Sustainability Initiatives:

- Investment in bio‑LPG production capacity in Europe

- Collaboration with local governments to expand LPG distribution in rural areas

- Commitment to achieving net‑zero emissions by 2050 across all operations

Download FREE Sample Report: Liquefied Petroleum Gas (LPG) Market – View in Detailed Research Report

1️⃣ 10. Chevron

Headquarters: San Ramon, California, USA

Key Offering: LPG Refining, LNG Export, Autogas

Chevron’s integrated refining and distribution capabilities enable it to supply high‑quality LPG across North America and global markets. The company is expanding its autogas fleet to support fleet operators and reduce transportation emissions.

Sustainability Initiatives:

- Investment in carbon‑capture technologies for LPG plants

- Development of smart cylinder solutions to improve distribution efficiency

- Commitment to reducing overall carbon intensity by 25% by 2035

Download FREE Sample Report: Liquefied Petroleum Gas (LPG) Market – View in Detailed Research Report

Get Full Report: Liquefied Petroleum Gas (LPG) Market – View in Detailed Research Report

🌍 Outlook: The Future of LPG Market

The LPG market is poised for steady growth, driven by clean‑energy adoption, urbanization, and expanding automotive applications. Forecasts indicate that the market will reach USD 214.28 billion by 2034, with a CAGR of 4.1% from 2025 to 2034. Key growth drivers include continued investment in gas purification technologies, expansion of autogas networks, and supportive government policies in emerging economies.

📈 Key Trends Shaping the Market:

- Expansion of LPG infrastructure and smart distribution networks

- Growth of autogas as a low‑emission vehicle fuel

- Increasing focus on bio‑LPG and renewable LPG alternatives

- Strategic partnerships between oil majors and technology firms to enhance safety and efficiency

- Digitalization of supply chains to improve transparency and reduce costs

- Top 10 Companies in the (S)-2-Octylamine (CAS 34566-04-6) Market (2026): Market Leaders Driving Chiral Innovation - August 3, 2026

- Top 10 Companies in the Global Digital Printing Ink for Textile Market (2026): Market Leaders Powering Innovation - August 3, 2026

- Top 10 Companies in the Green Chemistry and Sustainable Materials Market (2026): Market Leaders Powering the Transition to a Circular Economy - August 3, 2026