MARKET INSIGHTS

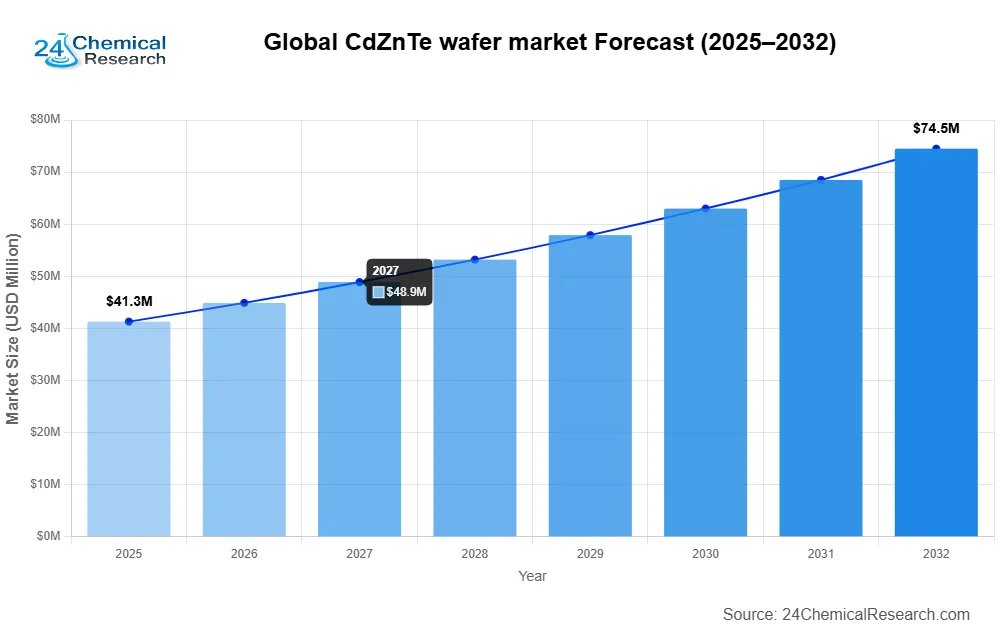

Global CdZnTe wafer market size was valued at USD 41.3 million in 2024 and is projected to reach USD 75 million by 2032, growing at a CAGR of 8.8% during the forecast period. The U.S. accounts for a significant portion of the market share, while China is emerging as a high‑growth region with increasing demand for advanced semiconductor materials.

CdZnTe (Cadmium Zinc Telluride) wafers are compound semiconductor materials known for their superior electrical and optical properties. These wafers demonstrate high resistivity and excellent energy resolution at room temperature, making them particularly valuable for radiation detection applications in medical imaging (such as CT and PET scanners), nuclear security systems, and space exploration equipment. The material’s wide bandgap and high stopping power for photons also enable applications in infrared optics and optoelectronic devices.

Market growth is primarily driven by increasing demand for non‑invasive medical diagnostics and expanding applications in homeland security radiation detectors. However, challenges such as high production costs and material defects during crystal growth may restrain growth. Technological advancements in wafer fabrication processes by key players like II‑VI Incorporated and Redlen Technologies are addressing these limitations through improved crystal growth techniques.

CdZnTe Wafer Market – View in Detailed Research Report

MARKET DYNAMICS

MARKET DRIVERS

Expanding Medical Imaging Applications to Fuel CdZnTe Wafer Demand

Global healthcare sector’s increasing reliance on advanced imaging technologies is driving substantial growth in the CdZnTe wafer market. With its superior energy resolution and room‑temperature operational capabilities, CdZnTe has become the material of choice for next‑generation X‑ray and gamma‑ray detectors. Medical imaging modalities utilizing these wafers are witnessing adoption rates growing at approximately 12‑15% annually. The technology’s ability to provide sharper images with lower radiation doses positions it as critical infrastructure in modern diagnostic centers. Recent breakthroughs in wafer production techniques have enabled thickness uniformity within ±5 microns, significantly enhancing detection accuracy.

Nuclear Security Concerns Accelerating Radiation Detection Adoption

Heightened global security requirements are creating robust demand for radiation detection solutions powered by CdZnTe wafers. Governments worldwide are investing heavily in nuclear threat detection systems, with defense‑related applications accounting for nearly 30% of current market revenue. The material’s capability to discriminate between different radiation types with over 95% accuracy makes it indispensable for border security and nuclear facility monitoring. Several countries have mandated the installation of advanced radiation portals at major transit hubs, creating a consistent demand pipeline for high‑quality wafers.

Semiconductor Industry Advancements Driving Material Innovation

The semiconductor sector’s relentless pursuit of superior electronic materials has positioned CdZnTe wafers as a critical component for specialized applications. With traditional silicon reaching performance limits in certain high‑frequency and optoelectronic applications, wafer manufacturers have achieved defect densities below 104 cm-2 through improved crystal growth techniques. This enables superior charge carrier mobility exceeding 1000 cm2/V·s, making the material ideal for cutting‑edge photonic devices. The telecom industry’s transition to higher frequency bands has particularly benefited from these advancements.

MARKET RESTRAINTS

High Production Costs and Material Scarcity Limiting Market Penetration

While CdZnTe wafers offer unparalleled performance characteristics, their widespread adoption faces significant cost barriers. The complex crystal growth process requires specialized equipment with yields typically below 60%, leading to wafer prices that can exceed $500/cm2 for premium grades. Tellurium scarcity compounds this challenge, with global production volumes struggling to meet the projected annual demand growth rate of 9‑11%. These economic factors currently restrict the technology to high‑value applications where performance justifies the premium pricing.

Technical Complexities in Large‑Area Wafer Production

Manufacturing challenges present another substantial restraint for the CdZnTe wafer market. Achieving uniform crystal properties across diameters exceeding 100mm remains technically demanding, with only a handful of producers capable of consistent quality output. The inherent brittleness of the material results in breakage rates averaging 15‑20% during standard processing steps. These technical hurdles limit production scalability and contribute to lengthy lead times that occasionally exceed six months for custom specifications.

MARKET CHALLENGES

Intellectual Property Barriers Creating Market Entry Obstacles

The CdZnTe wafer sector faces significant challenges stemming from concentrated intellectual property ownership. Over 75% of critical patents remain held by just three major manufacturers, creating steep barriers for new entrants. This patent thicket extends across the entire value chain—from crystal growth techniques to specialized doping methods—requiring potential competitors to navigate complex licensing arrangements. The situation has resulted in limited competition and slower price erosion compared to other semiconductor materials.

Workforce Shortages Impacting Production Capacity

Specialized labor shortages represent another pressing challenge for the industry. The complex nature of CdZnTe crystal growth demands experienced materials scientists and process engineers—skill sets that require 5‑7 years of specific training. Industry surveys indicate vacancy rates exceeding 25% for these critical positions, directly constraining production expansion efforts. The situation is particularly acute in regions lacking established semiconductor manufacturing ecosystems, forcing companies to invest heavily in internal training programs.

MARKET OPPORTUNITIES

Space Exploration Initiatives Creating New Application Frontiers

Emerging opportunities in space technology present significant growth potential for CdZnTe wafers. The material’s radiation hardness and excellent spectral resolution make it ideal for satellite‑based gamma‑ray telescopes and planetary exploration instruments. With global space agency budgets increasing by 8‑10% annually, demand for space‑grade wafers has grown correspondingly. Recent missions have demonstrated detector lifetimes exceeding 5 years in harsh orbital environments, validating the technology’s reliability for critical space applications.

Energy Sector Modernization Driving New Demand

The global transition toward advanced energy infrastructure is creating substantial opportunities for CdZnTe wafer applications. Next‑generation nuclear reactor designs require sophisticated radiation monitoring systems, while solar energy research benefits from the material’s unique optoelectronic properties. Pilot projects investigating CdZnTe‑based photovoltaic concepts have achieved conversion efficiencies surpassing 22%, suggesting potential for disruptive energy harvesting technologies. These developments position the wafer market for diversified growth beyond traditional detector applications.

MARKET TRENDS

Medical Imaging Advancements Drive Demand for CdZnTe Wafers

The growing adoption of CdZnTe (Cadmium Zinc Telluride) wafers in medical imaging applications is emerging as a dominant trend in the semiconductor market. The global market, valued at USD 41.3 million in 2024, is projected to reach USD 75 million by 2032 at an 8.8% CAGR, with medical applications accounting for approximately 45% of total demand. This surge is primarily due to CdZnTe’s ability to operate at room temperature while delivering high‑resolution X‑ray and gamma‑ray detection—critical for digital radiography and nuclear medicine. Recent innovations in single‑crystal CZT wafers have improved energy resolution to below 1%, making them indispensable for next‑generation diagnostic equipment.

Other Trends

Expansion in Homeland Security and Defense Applications

Security and defense sectors are increasingly utilizing CdZnTe wafers for radiation detection systems, driven by heightened global security concerns. Portable radiation detectors incorporating CZT technology now represent nearly 30% of the market’s non‑medical applications, with demand growing at 11% annually. The material’s superior stopping power for gamma rays and compact form factor make it ideal for border security and nuclear monitoring. Further, ongoing military modernization programs worldwide are accelerating the deployment of CZT‑based spectrometers for battlefield radiation mapping.

Technological Improvements in Wafer Manufacturing

Manufacturing process optimizations are significantly enhancing CdZnTe wafer quality and yield rates. Industry leaders have reduced defect densities by over 40% since 2020 through advanced crystal growth techniques like the Modified Vertical Bridgman method. While production challenges persist due to material purity requirements exceeding 99.999%, new purification approaches have increased usable wafer area to 85‑90% compared to 70% five years ago. These improvements are critical as the electronics sector demands larger wafer diameters—current R&D focuses on scaling from 100mm to 150mm wafers without compromising the material’s exceptional resistivity properties (typically >1010 Ω·cm).

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation Drives Competition in the CdZnTe Wafer Market

Global CdZnTe wafer market is moderately consolidated, featuring a mix of established semiconductor material suppliers and specialized manufacturers. II‑VI Incorporated (now Coherent Corp.) leads the market with its vertically integrated production capabilities and strong foothold in medical imaging applications. The company’s acquisition of Innovion Corporation in 2023 further strengthened its position in high‑purity crystal growth technologies.

Redlen Technologies Inc. and JX Nippon Mining & Metals Corporation have emerged as key challengers, particularly in radiation detection applications. Redlen’s proprietary crystal growth technology enables production of large‑volume, high‑performance CZT wafers, making it a preferred supplier for security screening equipment manufacturers.

While some players focus on volume production, others like Stanford Advanced Materials specialize in customized wafer solutions for research institutions. This diversification creates multiple competitive fronts—from price competition in standard wafers to technology races in high‑performance segments. The market saw increased R&D investments in 2023, particularly in defect reduction techniques to improve wafer yield rates.

Geographical expansion is another strategic focus, with Japanese and Chinese manufacturers aggressively entering Western markets. MTI Corporation recently expanded its California production facility to meet growing North American demand, while Kinheng Crystal established European distribution partnerships to supply medical device OEMs.

List of Key CdZnTe Wafer Manufacturers Profiled

-

II‑VI Incorporated (U.S.)

-

Redlen Technologies Inc. (Canada)

-

JX Nippon Mining & Metals Corporation (Japan)

-

MTI Corporation (Japan)

-

Stanford Advanced Materials (U.S.)

-

MSE Supplies LLC (U.S.)

-

Shalom EO (China)

-

Ganwafer (China)

-

PWAM (Japan)

-

Kinheng Crystal (China)

Segment Analysis:

By Type

Single Crystal CZT Wafer Segment Dominates Owing to Superior Performance in High‑Precision Applications

The market is segmented based on type into:

-

Single Crystal CZT Wafer

-

Polycrystalline CZT Wafer

-

Others

By Application

Medical Imaging Segment Leads Due to Rising Demand for Advanced Diagnostic Technologies

The market is segmented based on application into:

-

Medical Imaging

-

Electronics & Semiconductors

-

Energy

-

Others

Regional Analysis: CdZnTe Wafer Market

North America

North America, particularly the U.S., leads in technological advancements and adoption of CdZnTe wafers, driven by strong demand in medical imaging and homeland security applications. The region benefits from robust R&D investments from key players like II‑VI Incorporated and Redlen Technologies, coupled with supportive government funding for nuclear detection technologies. With the U.S. Department of Energy actively promoting next‑generation semiconductor materials, growth is further accelerated. However, high manufacturing costs and stringent regulatory frameworks for cadmium‑containing materials pose challenges. The presence of established healthcare infrastructure and increasing adoption of digital radiography systems continue to propel market expansion.

Europe

Europe’s market thrives on stringent regulatory standards for medical and nuclear safety, creating steady demand for high‑performance CdZnTe wafers. Countries like Germany and France dominate due to their advanced healthcare systems and investments in non‑invasive diagnostic technologies. The European Space Agency also contributes to demand through space‑based radiation detection applications. Environmental concerns related to cadmium usage, however, necessitate compliance with REACH and RoHS directives, pushing manufacturers toward sustainable production methods. Collaborative research initiatives between universities and industry players bolster innovation, enhancing wafer quality and application diversity.

Asia‑Pacific

As the fastest‑growing region, Asia‑Pacific leverages rapid industrialization and booming electronics manufacturing. China and Japan are at the forefront, with China prioritizing domestic semiconductor production to reduce import reliance. The proliferation of nuclear power plants and expanding healthcare infrastructure in India further drives demand. While cost sensitivity favors polycrystalline CdZnTe wafers, rising environmental awareness and government incentives for clean energy technologies are gradually shifting focus toward high‑purity single‑crystal variants. Japan’s expertise in optoelectronics and South Korea’s semiconductor industry add competitive momentum, though supply chain weaknesses in Southeast Asia intermittently disrupt production.

South America

South America exhibits nascent but promising growth, primarily in Brazil and Argentina, where budget allocations for nuclear energy and medical modernization are increasing. The lack of local manufacturing capabilities forces dependency on imports, inflating costs. Political and economic instability further constrains large‑scale investments, limiting market penetration. Nonetheless, partnerships with global suppliers and gradual infrastructure improvements signal long‑term potential, especially for radiation detection in mining and oil exploration sectors.

Middle East & Africa

The region remains underpenetrated but shows incremental adoption in defense and oilfield applications. The UAE and Saudi Arabia lead with investments in healthcare digitization and radiation monitoring for industrial safety. Limited technical expertise and minimal local production hinder market scalability, though partnerships with North American and European firms aim to bridge this gap. Africa’s growth is sporadic, focused primarily on South Africa’s nuclear research programs, while broader regional adoption awaits economic stabilization and infrastructure development.

Report Scope

This report presents a comprehensive analysis of the global and regional markets for CdZnTe wafer, covering the period from 2024 to 2032. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

-

Sales, sales volume, and revenue forecasts

-

Detailed segmentation by type and application

In addition, the report offers in‑depth profiles of key industry players, including:

-

Company profiles

-

Product specifications

-

Production capacity and sales

-

Revenue, pricing, gross margins

-

Sales performance

It further examines the competitive landscape, highlighting the major vendors and identifying the critical factors expected to challenge market growth.

As part of this research, we surveyed CdZnTe wafer manufacturers, suppliers, distributors, and industry experts. The survey covered various aspects, including:

-

Revenue and demand trends

-

Product types and recent developments

-

Strategic plans and market drivers

-

Industry challenges, obstacles, and potential risks

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global CdZnTe Wafer Market?

-> Global CdZnTe wafer market was valued at USD 41.3 million in 2024 and is projected to reach USD 75 million by 2032, growing at a CAGR of 8.8% during the forecast period.

Which key companies operate in Global CdZnTe Wafer Market?

-> Key players include Stanford Advanced Materials, MSE Supplies LLC, II‑VI Incorporated, JX Nippon Mining & Metals Corporation, Shalom EO, Redlen Technologies Inc., MTI Corporation, Ganwafer, PWAM, and Kinheng Crystal, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand for radiation detection in medical imaging, advancements in semiconductor technologies, and rising adoption in defense and security applications.

Which region dominates the market?

-> North America holds the largest market share, while Asia‑Pacific is expected to witness the highest growth rate due to expanding electronics and healthcare industries.

What are the emerging trends?

-> Emerging trends include development of high-performance CZT wafers for space applications, integration with AI for enhanced imaging systems, and increased focus on sustainable manufacturing processes.

Download FREE Sample Report: CdZnTe Wafer Market – View in Detailed Research Report

Get Full Report Here: CdZnTe Wafer Market – View in Detailed Research Report

Outlook: The Future of CdZnTe Wafer Market Is Growing and Innovating

The CdZnTe wafer market is poised for sustained growth, driven by escalating demand in medical imaging, homeland security, and space exploration. Continued investment in advanced crystal growth technologies and a shift toward high‑purity single‑crystal wafers are expected to enhance performance and reduce production costs. Regional dynamics will see North America maintaining a leadership position, while Asia‑Pacific’s rapid industrialization and government support will accelerate adoption. The market’s trajectory suggests a robust expansion, with opportunities for new entrants to innovate in sustainability and cost‑efficiency.

Future Trends Shaping the Market

Key trends include:

-

Development of high‑performance CZT wafers for space applications

-

Integration with AI and machine learning for enhanced imaging systems

-

Increased focus on sustainable manufacturing processes and material recycling

-

Expansion of energy sector applications, including nuclear monitoring and photovoltaic research

- Top 10 Companies in the Vegetal Concrete Market (2026): Market Leaders Shaping Sustainable Construction - July 29, 2026

- Top 10 Companies in the Flupyradifurone Market (2026): Market Leaders Driving Modern Pest Management - July 29, 2026

- Top 10 Companies in the Global Anionic Fluorosurfactant Market (2026): Market Leaders Driving Innovation - July 29, 2026