MARKET INSIGHTS

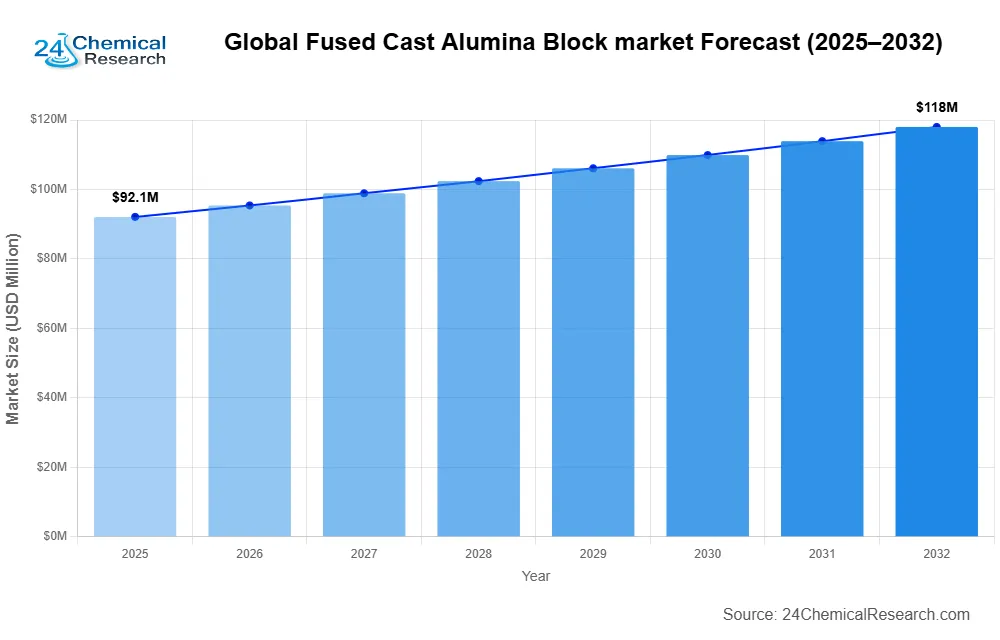

Global Fused Cast Alumina Block market size was valued at USD 92.1 million in 2025 and is projected to reach USD 117 million by 2026, growing at a CAGR of 3.6% during the forecast period.

Fused cast alumina blocks are high-performance refractory materials manufactured by melting high-purity calcined alumina (over 95% Al₂O₃ content) in electric arc furnaces at temperatures exceeding 2350°C. These blocks undergo precise casting, annealing, and finishing processes to achieve exceptional thermal and chemical stability. Their unique properties make them indispensable in high-temperature industrial applications where glass contamination must be minimized.

The market growth is primarily driven by increasing demand from the glass manufacturing industry, particularly for furnace linings in clarification and cooling sections. While the construction sector’s expansion contributes to demand, challenges like volatile raw material prices and energy-intensive production processes may restrain growth. Key manufacturers are focusing on process optimization and product innovation to maintain competitiveness in this specialized refractory segment.

Fused Cast Alumina Block Market – View in Detailed Research Report

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand from Glass Manufacturing Industry to Fuel Market Expansion

Global glass industry is experiencing steady growth, with production volumes exceeding 130 million tons annually, creating substantial demand for high-performance refractory materials like fused cast alumina blocks. These specialized blocks offer superior resistance to glass corrosion at temperatures above 1350°C, making them indispensable for critical furnace zones. Modern glass manufacturing requires increasingly sophisticated refractory solutions due to higher operational temperatures and extended furnace campaigns. A significant 78% of fused cast alumina block applications are concentrated in glass furnace construction, particularly in the float glass sector where product purity is paramount.

Advancements in Non-Ferrous Metal Production Driving Adoption

Non-ferrous metal smelting operations are progressively adopting fused cast alumina blocks for their exceptional thermal shock resistance and chemical inertness. The aluminum production sector alone accounts for nearly 15% of global consumption, as these blocks demonstrate remarkable performance in environments with aggressive molten salts and metals. Recent industry shifts toward cleaner production methods have increased the preference for high-purity alumina refractories that minimize contamination. With global aluminum output projected to grow at 3.2% CAGR through 2030, this application segment presents sustained growth potential for market players.

Technological Improvements in Production Processes

Manufacturers are implementing advanced electric arc furnace technologies that enable more precise temperature control during the casting process, resulting in blocks with tighter crystalline structures and improved performance characteristics. Recent process optimizations have reduced energy consumption by approximately 18% while increasing yield rates. These advancements allow producers to offer competitive pricing while maintaining the high purity standards (≥95% Al₂O₃ content) required by end-users. The development of specialized α‑β alumina blends has further expanded the material’s applicability across different thermal shock scenarios.

MARKET RESTRAINTS

High Production Costs Limiting Market Penetration

The energy-intensive nature of fused cast alumina block manufacturing, requiring sustained temperatures exceeding 2350°C, creates significant cost barriers. Production expenses account for nearly 60-70% of final product pricing, making these refractories considerably more expensive than conventional options. Small and medium-sized glass manufacturers often find the capital expenditure prohibitive, particularly in price-sensitive emerging markets. While long-term durability offsets some cost concerns, the initial investment remains a substantial deterrent for many potential adopters.

Raw Material Price Volatility Affecting Profit Margins

Calcined alumina prices have exhibited 12-15% annual fluctuations in recent years, directly impacting production costs. The market relies heavily on consistent supplies of high-purity alumina (≥99.5%), with limited alternative material options. Geopolitical factors affecting bauxite supplies and energy costs for calcination further compound pricing uncertainties. These variables make long-term cost forecasting challenging, compelling manufacturers to maintain conservative pricing strategies that may limit market growth potential.

Technical Complexities in Installation and Maintenance

Proper installation of fused cast alumina blocks requires specialized knowledge and skilled labor, with improper assembly potentially reducing service life by 30-40%. The precision fitting demands during furnace construction add significant labor costs, while replacement procedures in operational furnaces present additional technical challenges. Limited availability of qualified installation teams in developing markets restricts adoption rates, despite clear performance advantages. These operational complexities create hesitancy among some end-users considering upgrades to advanced refractory systems.

MARKET OPPORTUNITIES

Emerging Applications in Specialty Glass Production

The rapid expansion of specialty glass segments, particularly in electronics (cover glass) and pharmaceutical packaging, presents new growth avenues. These high-value applications demand ultra-pure refractory materials to maintain glass quality, with fused cast alumina blocks uniquely positioned to meet these requirements. The pharmaceutical glass packaging market alone is projected to exceed $22 billion by 2030, creating substantial downstream demand. Manufacturers developing specialized alumina formulations for these niche applications can command premium pricing and establish long-term supply agreements.

Geographic Expansion in Developing Markets

Asia-Pacific represents the fastest-growing regional market, with China and India driving 65% of new capacity additions in glass and metal production. Localized production facilities and strategic partnerships with regional distributors enable international suppliers to capitalize on this growth. The establishment of technical support centers in these regions helps overcome adoption barriers by providing installation expertise and maintenance training. With Asia-Pacific accounting for nearly 40% of global glass production, targeted expansion in these markets offers significant revenue potential.

Development of Eco-Friendly Production Methods

Sustainability initiatives are creating demand for refractory solutions with lower environmental impact across the product lifecycle. Manufacturers investing in energy-efficient smelting technologies and recycled material integration can differentiate their offerings. The development of alumina blocks with extended service lives reduces replacement frequency and associated waste generation. These environmentally conscious innovations align with broader industry trends and can command 10-15% price premiums in regulated markets with stringent sustainability requirements.

MARKET CHALLENGES

Intense Competition from Alternative Refractory Materials

Fused cast AZS blocks continue to dominate certain furnace applications due to their lower cost structure, particularly in container glass production. While alumina blocks offer purity advantages, price sensitivity in certain market segments limits conversion rates. The development of advanced bonded alumina products with competitive performance characteristics at lower price points presents additional competitive pressure. Market penetration strategies must carefully balance performance benefits against cost considerations across different application scenarios.

Technological Limitations in Extreme Operating Conditions

While excelling in corrosion resistance, fused cast alumina blocks face performance constraints in applications with extreme thermal cycling requirements. The material’s relatively low thermal shock resistance compared to some composite refractories limits suitability for certain furnace designs. Ongoing research into modified crystalline structures aims to address these limitations, but current technology boundaries constrain addressable market size. Manufacturers must clearly communicate optimal operating parameters to prevent performance issues that could damage product reputation.

Supply Chain Vulnerabilities for Critical Inputs

The reliance on high-purity alumina creates supply chain risks, with few suppliers capable of meeting the stringent quality specifications. Transportation and logistics challenges for both raw materials and finished products add complexity, particularly for international shipments of these dense, fragile materials. Recent global supply chain disruptions have highlighted the importance of regional stockpiling strategies and alternative sourcing options, requiring significant working capital investments from manufacturers to ensure reliable delivery capabilities.

MARKET TRENDS

Expansion of Glass Manufacturing to Drive Market Growth

Global fused cast alumina block market is experiencing steady growth, primarily driven by increasing demand from the glass manufacturing industry. With fused cast alumina blocks being essential for high-temperature applications in glass furnaces, the rise in construction and automotive sectors has significantly boosted glass production worldwide. The market was valued at $92.1 million in 2025, with projections indicating growth to $117 million by 2026 at a 3.6% CAGR. These refractory materials, capable of withstanding temperatures above 1350°C, are favored for their superior erosion resistance and minimal contamination of molten glass, making them indispensable for modern glass furnaces.

Other Trends

Adoption of High-Purity Alumina Blocks

Manufacturers are increasingly shifting toward high-purity fused cast α‑alumina blocks due to their exceptional thermal stability and corrosion resistance in aggressive glass melt environments. These blocks, composed of over 95% calcined alumina, offer extended lifespans in furnaces, reducing operational downtime and maintenance costs. The segment accounted for nearly 40% of market share in 2024, with demand surging as glass producers seek materials that enhance energy efficiency and product quality. Additionally, the adoption of β‑alumina and α‑β hybrid blocks is gaining traction for specialized applications in non-ferrous metal smelting and chemical industries.

Technological Advancements in Refractory Solutions

Recent innovations in casting techniques and thermal processing are enhancing the performance characteristics of fused cast alumina blocks. Leading manufacturers are investing in electric arc furnace optimizations to achieve more uniform material structures, improving resistance to thermal shocks and alkali vapor attacks. The development of pre-assembled block solutions has also streamlined furnace construction, reducing installation time by up to 30%. Furthermore, integration of advanced quality control systems ensures consistent product performance, addressing the stringent requirements of float glass and specialty glass production lines.

COMPETITIVE LANDSCAPE

Key Industry Players

Manufacturers Focus on High-Temperature Performance to Gain Market Edge

Global fused cast alumina block market exhibits a moderately consolidated competitive structure, with established refractory specialists dominating the revenue share. Market leaders maintain their position through continuous product innovation and strategic expansions into high-growth glass manufacturing regions across Asia and Europe. While the top five players accounted for approximately 42% of 2024 market revenue, several regional manufacturers are gaining traction through cost-competitive offerings.

Top 10 Companies in the Fused Cast Alumina Block Market (2026)

1️⃣ 1. AGC Ceramics Co., Ltd.

Headquarters: Osaka, Japan

Key Offering: High-purity α‑Alumina blocks for float glass furnaces

AGC Ceramics has been a pioneer in refractory technology, delivering advanced alumina blocks that offer superior thermal stability and chemical resistance. Their flagship products are widely used in high-temperature glass production, providing extended service life and reduced contamination risks.

Sustainability Initiatives:

- Investing in energy‑efficient electric arc furnace processes

- Reducing carbon footprint through optimized calcination

- Developing recyclable alumina‑based refractory solutions

2️⃣ 2. Monofrax LLC

Headquarters: Chicago, USA

Key Offering: High‑purity fused cast alumina blocks for glass and metal furnaces

Monofrax specializes in producing refractory blocks with exceptional resistance to high temperatures and aggressive molten environments. Their products are integral to modern glass and non‑ferrous metal production, ensuring minimal contamination and extended furnace life.

Sustainability Initiatives:

- Optimizing electric arc furnace temperature control to cut energy use

- Implementing waste‑reduction programs in calcination

- Collaborating with glass manufacturers on carbon‑neutral furnace upgrades

3️⃣ 3. Termo Refractaires

Headquarters: Lyon, France

Key Offering: Specialty alumina blocks for optical and specialty glass production

Termo Refractaires focuses on high‑purity alumina solutions for optical glass and specialty applications, addressing challenges such as bubble formation and surface defects that affect glass quality.

Sustainability Initiatives:

- Developing low‑energy calcination processes

- Partnering with glass manufacturers to reduce furnace downtime

- Researching recyclable alumina additives

4️⃣ 4. DF Refratek GmbH

Headquarters: Stuttgart, Germany

Key Offering: Advanced bonded alumina blocks for high‑temperature metal smelting

DF Refratek offers bonded alumina solutions that combine high thermal shock resistance with chemical inertness, catering to the demanding conditions of non‑ferrous metal production.

Sustainability Initiatives:

- Enhancing furnace efficiency through improved block design

- Reducing emissions in calcination processes

- Investing in renewable energy for production facilities

5️⃣ 5. Yuhua Refractory Technology Co.

Headquarters: Guangzhou, China

Key Offering: Cost‑effective high‑purity alumina blocks for glass and metal furnaces

Yuhua provides competitively priced alumina blocks that meet stringent purity requirements, enabling Chinese and regional manufacturers to upgrade their refractory systems without prohibitive costs.

Sustainability Initiatives:

- Implementing energy‑saving calcination techniques

- Optimizing raw material sourcing to reduce carbon emissions

- Providing technical support for efficient furnace operation

6️⃣ 6. Zhengzhou Sunrise Refractory Co.

Headquarters: Zhengzhou, China

Key Offering: High‑purity fused cast alumina blocks for glass and metal industries

Zhengzhou Sunrise focuses on expanding capacity to meet domestic demand, offering blocks that balance performance and affordability for a growing market.

Sustainability Initiatives:

- Reducing energy consumption in electric arc furnaces

- Developing recyclable alumina composites

- Collaborating with local governments on green manufacturing initiatives

7️⃣ 7. Altingoz Ates Tugla

Headquarters: Istanbul, Turkey

Key Offering: High‑purity alumina blocks for glass and specialty applications

Altingoz provides advanced alumina solutions tailored for the Turkish and regional glass markets, emphasizing purity and performance.

Sustainability Initiatives:

- Optimizing furnace design for lower energy use

- Implementing waste‑reduction programs in calcination

- Partnering with industry associations on sustainability standards

8️⃣ 8. SIGMA Srl

Headquarters: Milan, Italy

Key Offering: High‑purity fused cast alumina blocks for glass and metal furnaces

SIGMA focuses on delivering high‑performance refractory solutions with a strong emphasis on quality and reliability for European manufacturers.

Sustainability Initiatives:

- Investing in energy‑efficient calcination technologies

- Reducing carbon emissions through process optimization

- Providing training programs for efficient furnace operation

9️⃣ 9. YINGKOU LMM YOTIA

Headquarters: Yunnan, China

Key Offering: High‑purity fused cast alumina blocks for glass and metal industries

YINGKOU offers cost‑effective, high‑quality refractory solutions that cater to the diverse needs of Chinese manufacturers.

Sustainability Initiatives:

- Optimizing electric arc furnace operations

- Reducing waste in calcination processes

- Developing recyclable alumina composites

🔟 10. Rongsheng Kiln Refractory Co.

Headquarters: Shenyang, China

Key Offering: High‑purity fused cast alumina blocks for glass and metal furnaces

Rongsheng focuses on providing high‑performance refractory solutions with an emphasis on durability and cost‑effectiveness for the Chinese market.

Sustainability Initiatives:

- Implementing energy‑saving calcination processes

- Reducing emissions in electric arc furnace operations

- Collaborating with industry partners on green manufacturing

Download FREE Sample Report: Fused Cast Alumina Block Market – View in Detailed Research Report

Get Full Report Here: Fused Cast Alumina Block Market – View in Detailed Research Report

🌍 Outlook: The Future of Fused Cast Alumina Block Market

As the glass manufacturing sector continues to expand, the demand for high‑performance fused cast alumina blocks is expected to rise. Technological advancements in electric arc furnace processes and the development of specialized α‑β alumina blends will drive performance improvements, while growing focus on sustainability will push manufacturers toward greener production methods. Regional expansion, particularly in Asia‑Pacific, will further accelerate market growth, supported by increasing infrastructure investments and the adoption of advanced glass technologies.

📈 Key Trends Shaping the Market:

- Rapid growth of specialty glass segments, such as electronics and pharmaceutical packaging

- Expansion of high‑purity alumina solutions in non‑ferrous metal smelting

- Adoption of energy‑efficient and low‑carbon production processes

- Increased focus on pre‑assembled block solutions to reduce installation time

- Growing demand for recyclable and sustainable refractory materials

- Top 10 Companies in the Russia Soy-Based Chemicals Market (2026): Market Leaders Driving Innovation - July 28, 2026

- Top 10 Companies in the Global Galvanised Steel Wire Market (2026): Market Leaders Powering Infrastructure Growth - July 28, 2026

- Top 10 Companies in the Soft Fibre Ceiling System Market (2026): Market Leaders Powering Acoustic Innovation - July 28, 2026