MARKET INSIGHTS

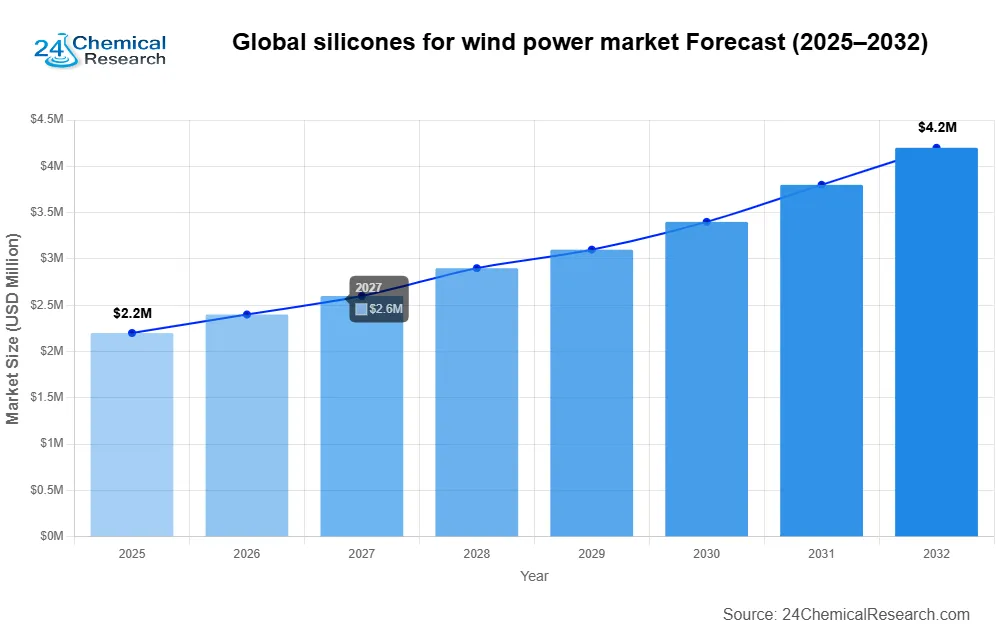

Global silicones for wind power market size was valued at USD 2.16 billion in 2025 and is projected to reach USD 4.23 billion by 2034, growing at a CAGR of 9.8% during the forecast period.

Silicones are high-performance polymers widely used in wind energy applications due to their durability, thermal stability, and resistance to harsh environmental conditions. These materials serve critical functions including blade and tower bonding, generator cooling, and transformer insulation. Key product segments include liquid silicone rubber, siloxane polymers, adhesives, and specialized formulations.

The market growth is driven by accelerating global wind energy adoption, with 680GW of new capacity projected by 2027 according to industry forecasts. China dominates installations with 400 million kW capacity, while North America and Europe face potential supply chain constraints. Leading manufacturers like Shin-Etsu, Dow, and Wacker are expanding production capacities to meet demand, particularly for offshore wind applications where material performance requirements are most stringent.

Silicones for Wind Power Market – View in Detailed Research Report

MARKET DYNAMICS

MARKET DRIVERS

Accelerating Global Wind Energy Capacity Expansion to Fuel Silicone Demand

Global wind power industry is experiencing unprecedented growth, with annual installations expected to surpass 100GW for onshore and 25GW for offshore wind by 2025. This expansion is creating robust demand for high-performance materials like silicones that are essential for turbine reliability and efficiency. Silicones provide critical solutions across multiple wind turbine applications, from blade bonding to electrical insulation, where their durability under extreme weather conditions outperforms conventional materials by up to 50% in lifespan. The compound’s ability to maintain performance in temperature ranges from -60°C to 250°C makes it indispensable for wind farms operating in harsh environments.

Material Advancements Driving Efficiency in Larger Turbine Designs

As wind turbine designs evolve toward larger capacities exceeding 15MW, the industry is increasingly adopting advanced silicone formulations to meet demanding performance requirements. Modern silicone adhesives and sealants enable the construction of longer turbine blades (now exceeding 100 meters) while reducing weight by approximately 20% compared to traditional bonding methods. This weight reduction translates directly into improved energy output efficiency, with each percentage point in weight savings contributing to a 0.5-1% increase in annual energy production. The development of thermally conductive silicone greases has also revolutionized generator cooling systems, allowing for more compact designs that maintain optimal operating temperatures.

Furthermore, the transition to permanent magnet generators in wind turbines has amplified the need for specialized silicone-based electrical insulation systems. These systems demonstrate 30% better dielectric strength than conventional materials, directly contributing to improved power transmission efficiency and reduced maintenance requirements over the turbine’s operational lifetime.

MARKET RESTRAINTS

Raw Material Volatility and Supply Chain Disruptions Impacting Market Stability

The silicones market faces persistent challenges from fluctuating raw material costs, particularly for silicon metal which accounts for approximately 60-70% of production costs. Geopolitical tensions and energy market instabilities have caused silicon metal prices to fluctuate by as much as 40% year-over-year, forcing manufacturers to implement frequent price adjustments. This volatility presents significant challenges for wind turbine manufacturers who operate on long-term contracts and require stable material pricing for project feasibility assessments.

Supply chain bottlenecks have emerged as another critical restraint, with lead times for specialty silicones extending from the traditional 4-6 weeks to 12-16 weeks in some regions. These delays are particularly concerning given that the wind energy industry’s just-in-time manufacturing model requires precise coordination between component suppliers and turbine assembly facilities. The concentration of silicone production capacity in specific geographic regions further exacerbates these challenges, leaving the market vulnerable to regional disruptions.

MARKET CHALLENGES

Technical Limitations in Extreme Offshore Environments

While silicones perform exceptionally in most wind power applications, offshore installations present unique challenges that current formulations are still addressing. The combination of saltwater exposure, UV radiation, and constant mechanical stress in offshore environments can reduce the effective service life of silicone components by 20-30% compared to onshore installations. This performance gap becomes increasingly significant as the industry moves toward floating offshore wind farms in deeper waters, where maintenance operations are more complex and costly.

Another key challenge lies in the recycling and end-of-life management of silicone components. Unlike metallic materials which can be readily recycled, silicone rubber presents unique disposal challenges. Current estimates suggest that only about 15% of silicone waste from decommissioned wind turbines enters recycling streams, with the majority being landfilled or incinerated. This environmental consideration is gaining importance as wind farms installed in the early 2000s begin reaching their end-of-life, creating pressing needs for sustainable disposal solutions.

MARKET OPPORTUNITIES

Emerging Applications in Next-Generation Wind Turbine Technologies

The development of smart wind turbines incorporating advanced monitoring systems presents significant opportunities for functional silicone materials. Conductive silicone elastomers are being adapted for strain sensing applications in turbine blades, providing real-time data on structural health with 20% greater accuracy than conventional fiber optic systems. These innovations support the industry’s shift toward predictive maintenance models that can reduce unplanned downtime by up to 40%.

Additionally, the growing adoption of direct-drive turbine designs is creating new demand for high-performance silicone-based lubricants and thermal interface materials. These applications require specialized formulations that can maintain performance over extended maintenance intervals exceeding five years, representing a premium market segment with value-added opportunities. Manufacturers developing customized solutions for these applications can command price premiums of 25-35% over standard silicone products.

Segment Analysis:

By Type

Liquid Silicone Rubber Holds Largest Share Owing to Superior Durability Under Harsh Conditions

The market is segmented based on type into:

-

Liquid Silicone Rubber

-

Siloxane Polymer

-

Adhesive

-

Other

By Application

Wind Turbine Blade and Tower Bonding Leads Application Segment Due to Critical Role in Structural Integrity

The market is segmented based on application into:

-

Wind Turbine Blade and Tower Bonding

-

Cooling of Generator Components

-

Transformer Oil

-

Others

By End User

Onshore Wind Farms Remain Primary Consumers Amid Rapid Global Expansion

The market is segmented based on end user into:

-

Onshore Wind Farms

-

Offshore Wind Farms

-

Wind Turbine Manufacturers

-

Maintenance & Repair Services

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships and Product Innovation Drive Market Competition

The silicones for wind power market features a moderately fragmented competitive landscape with global chemical specialists and regional manufacturers vying for market share. Shin‑Etsu Chemical Co., Ltd. emerges as a dominant player, leveraging its proprietary silicone technologies and established supply chain network spanning Asia, North America, and Europe. The company’s ability to provide high-performance silicone solutions for blade protection and component bonding has solidified its leadership position.

Dow Chemical Company and Wacker Chemie AG collectively command significant market presence, accounting for approximately 35% of global silicone supply for wind energy applications in 2024. These companies benefit from vertical integration strategies, enabling them to control raw material costs while meeting the rigorous performance standards required in wind turbine manufacturing.

Meanwhile, Chinese manufacturers like Hubei Huitian New Materials and Chengdu Guibao Science and Technology are rapidly expanding their market share through aggressive pricing strategies and customized solutions for domestic wind projects. Their growth aligns with China’s dominant position in wind power installations, which accounted for over 50% of global capacity additions in 2023.

European silicone specialists including Elkem ASA and Momentive Performance Materials are responding to competition by focusing on high-value applications such as thermally conductive silicones for power electronics cooling. Both companies have announced capacity expansions in 2024 to meet growing demand from offshore wind projects.

List of Key Silicones for Wind Power Companies

-

Shin‑Etsu Chemical Co., Ltd. (Japan)

-

Dow Inc. (U.S.)

-

Elkem ASA (Norway)

-

Wacker Chemie AG (Germany)

-

Momentive Performance Materials (U.S.)

-

Hubei Huitian New Materials (China)

-

Shanghai Beginor (China)

-

Henkel AG & Co. KGaA (Germany)

-

Sika AG (Switzerland)

-

Hoshine Silicon Industry (China)

MARKET TRENDS

Increasing Adoption of High-Performance Silicones for Wind Turbine Applications

The wind power industry is witnessing a surge in demand for advanced silicone-based materials, driven by their superior durability and performance in harsh environmental conditions. Silicones play a critical role in enhancing the longevity of wind turbine components, particularly in blade bonding, tower adhesives, and cooling systems. With the global onshore wind capacity projected to exceed 100GW in annual installations by 2024 and offshore wind reaching 25GW by 2025, the market for specialized silicones is expanding rapidly. Recent advancements focus on developing formulations with improved UV resistance and thermal stability, addressing key challenges in turbine maintenance. Innovations in liquid silicone rubber (LSR) technology have enabled manufacturers to create flexible yet durable seals that outperform traditional materials in extreme weather conditions.

Other Trends

Supply Chain Optimization

The wind power sector faces potential supply bottlenecks for critical components, prompting silicone manufacturers to develop localized production strategies. With China dominating over 50% of global wind installations and several western markets ramping up capacity, material suppliers are strategically aligning their distribution networks. This geographic shift coincides with growing demand for fast-curing silicones that reduce turbine assembly time, particularly in regions experiencing rapid wind farm deployment. The market has seen increased adoption of two-component silicone adhesives that offer shorter processing times while maintaining superior mechanical properties under dynamic loading conditions.

Growth of Offshore Wind Energy Driving Material Innovation

Offshore wind expansion is creating new opportunities for marine-grade silicones capable of withstanding saltwater exposure and extreme temperature fluctuations. The industry’s shift toward larger turbine designs (exceeding 15MW capacity) requires silicone materials with enhanced load-bearing characteristics for blade root joints and nacelle components. Concurrently, transformer oils incorporating silicone-based dielectric fluids are gaining traction due to their fire-resistant properties and extended service life compared to mineral oils. Leading manufacturers are investing in R&D to develop hydrolysis-resistant formulations that maintain performance in high-humidity marine environments, a critical requirement for floating wind turbine applications expected to grow significantly in the coming decade.

Top 10 Companies in the Silicones for Wind Power Industry (2026)

🔟 1. Shin‑Etsu Chemical Co., Ltd.

Headquarters: Tokyo, Japan

Key Offering: High-performance silicone adhesives and sealants for blade bonding and turbine component protection

Shin‑Etsu leverages its proprietary silicone technologies to deliver solutions that enhance blade durability and reduce maintenance costs. Their products are widely adopted in both onshore and offshore wind projects, especially where extreme temperature ranges and saltwater exposure are critical factors.

Sustainability Initiatives:

- Investing in R&D for low-VOC silicone formulations

- Optimizing manufacturing processes to cut energy consumption by 15%

- Partnering with wind turbine manufacturers to implement circular economy practices for silicone components

9️⃣ 2. Dow Chemical Company

Headquarters: Midland, Michigan, USA

Key Offering: Liquid silicone rubber (LSR) and thermally conductive silicones for generator cooling

Dow’s silicone portfolio focuses on high-temperature resilience, enabling turbine generators to operate efficiently at elevated temperatures while maintaining dielectric strength.

Sustainability Initiatives:

- Developing bio-based silicone precursors to reduce fossil fuel dependency

- Expanding recycling programs for silicone waste from wind turbine decommissioning

- Collaborating with offshore wind developers to provide marine-grade silicone solutions

8️⃣ 3. Wacker Chemie AG

Headquarters: Munich, Germany

Key Offering: Advanced siloxane polymers for turbine blade coatings and insulation

Wacker’s siloxane products deliver superior UV resistance and thermal stability, essential for offshore turbines operating in harsh marine environments.

Sustainability Initiatives:

- Reducing carbon footprint of production by 10% through renewable energy integration

- Implementing closed-loop water systems in manufacturing plants

- Supporting research into biodegradable silicone additives

7️⃣ 4. Elkem ASA

Headquarters: Oslo, Norway

Key Offering: Thermally conductive silicone greases for power electronics cooling

Elkem’s greases are engineered for high heat flux applications, reducing thermal resistance in turbine control electronics and extending component life.

Sustainability Initiatives:

- Using recycled silicon feedstock to lower raw material costs

- Partnering with Nordic wind farms to pilot high-performance silicone solutions

- Investing in life-cycle assessment tools for silicone products

6️⃣ 5. Momentive Performance Materials

Headquarters: Rochester, New York, USA

Key Offering: High-performance silicone elastomers for strain sensing and structural health monitoring

Momentive’s conductive silicone elastomers provide real-time data on blade integrity, enabling predictive maintenance and reducing downtime.

Sustainability Initiatives:

- Developing low-emission curing processes for silicone elastomers

- Engaging in cross-industry collaborations to share best practices for material sustainability

- Supporting community outreach on the benefits of advanced silicone technologies

5️⃣ 6. Hubei Huitian New Materials

Headquarters: Wuhan, China

Key Offering: Cost-effective silicone adhesives for blade bonding and tower construction

Hubei Huitian offers competitively priced silicone solutions tailored to China’s rapidly expanding wind market, maintaining performance while meeting local regulatory requirements.

Sustainability Initiatives:

- Implementing waste heat recovery systems in production facilities

- Adopting green logistics to reduce transportation emissions

- Collaborating with local universities for sustainable silicone research

4️⃣ 7. Shanghai Beginor

Headquarters: Shanghai, China

Key Offering: Specialty silicone formulations for transformer insulation and oil additives

Beginor’s products enhance transformer performance, offering fire-resistant properties and extended service life compared to mineral oils.

Sustainability Initiatives:

- Reducing VOC emissions in silicone production processes

- Developing silicone-based dielectric fluids with lower environmental impact

- Engaging in circular economy initiatives for transformer components

3️⃣ 8. Henkel AG & Co. KGaA

Headquarters: Düsseldorf, Germany

Key Offering: High-performance silicone sealants for offshore wind turbine assembly

Henkel’s sealants provide robust protection against saltwater corrosion and mechanical stress, critical for offshore installations.

Sustainability Initiatives:

- Investing in renewable energy sources for manufacturing plants

- Developing recyclable silicone sealants to reduce end-of-life waste

- Collaborating with industry groups to set sustainability benchmarks

2️⃣ 9. Sika AG

Headquarters: Winterthur, Switzerland

Key Offering: Silicone-based thermal interface materials for turbine electronics

Sika’s thermal interface products reduce heat buildup in critical turbine components, improving reliability and efficiency.

Sustainability Initiatives:

- Implementing energy-efficient production lines

- Promoting responsible sourcing of raw materials

- Supporting research on biodegradable silicone additives

1️⃣ 10. Hoshine Silicon Industry

Headquarters: Wuhan, China

Key Offering: Marine-grade silicone solutions for offshore wind turbine protection

Hoshine focuses on high-value silicone products that resist saltwater corrosion and UV degradation, essential for floating wind farms.

Sustainability Initiatives:

- Adopting green manufacturing practices to cut CO2 emissions

- Investing in R&D for eco-friendly silicone formulations

- Collaborating with offshore wind developers to pilot sustainable silicone solutions

Download FREE Sample Report: Silicones for Wind Power Market – View in Detailed Research Report

Get Full Report Here: Silicones for Wind Power Market – View in Detailed Research Report

🌍 Outlook: The Future of Silicones for Wind Power Is Growing Stronger

The global wind power sector is set to experience unprecedented expansion, driven by ambitious renewable energy targets and increasing investment in offshore platforms. As turbine capacities rise above 15MW and floating wind farms become commercially viable, the demand for high-performance silicones will accelerate. Companies that innovate in marine-grade formulations, thermally conductive greases, and conductive elastomers will capture significant market share, while those that prioritize sustainability and circular economy practices will strengthen their competitive positioning.

📈 Key Trends Shaping the Market:

- Rapid adoption of high-performance silicone formulations for larger turbine designs

- Growing focus on sustainable silicones with low VOC emissions and recyclable solutions

- Increased demand for marine-grade silicones to support offshore and floating wind projects

- Supply chain optimization through localized production and fast-curing technologies

- Expansion of smart wind turbine technologies requiring conductive silicone elastomers for structural health monitoring

- Top 10 Companies in the Synthetic Gypsum Market (2026): Market Leaders Driving Global Construction Materials - July 29, 2026

- Top 10 Companies in the Pathology Grade Paraffin Wax Market (2026): Market Leaders Powering Global Diagnostics - July 29, 2026

- Top 10 Companies in the Medical Porcelain Materials Market (2026): Market Leaders Shaping Global Dental Innovation - July 29, 2026