MARKET INSIGHTS

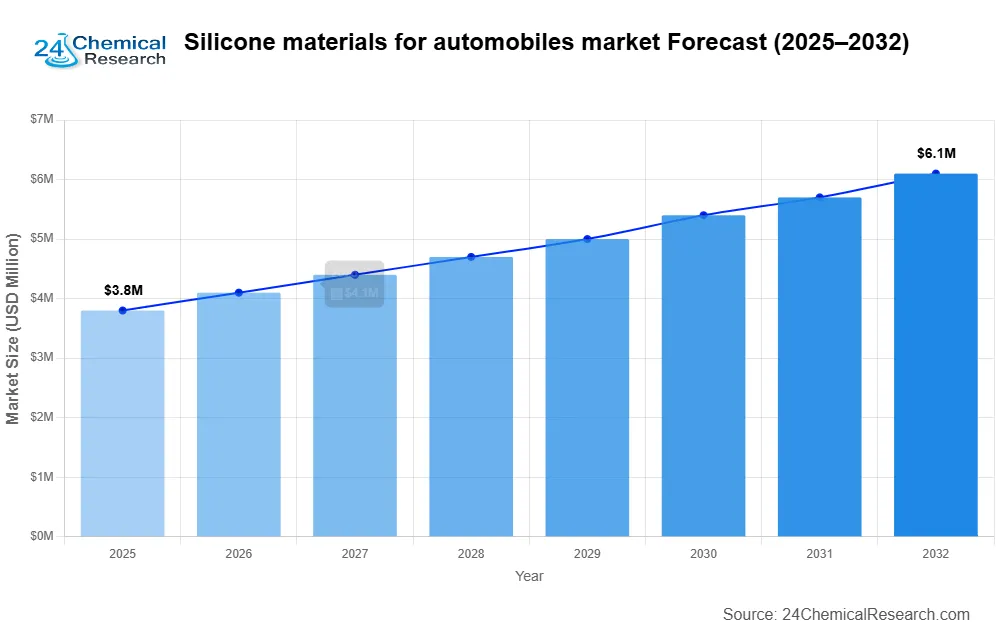

Global silicone materials for automobiles market size was valued at USD 3.84 billion in 2024 and is projected to reach USD 6.12 billion by 2032, exhibiting a CAGR of 6.9% during the forecast period.

Silicone materials are high-performance polymers widely used in automotive applications due to their exceptional thermal stability, flexibility, and chemical resistance. These materials include silicone elastomers, resins, gels, and oils, serving critical functions in sealing, bonding, vibration damping, and thermal management. Their versatility makes them indispensable in both conventional and electric vehicle production.

The market growth is driven by increasing automotive production, particularly in Asia, which accounted for 56% of global vehicle output in 2022. While traditional applications dominate, emerging opportunities in electric vehicles are accelerating demand for advanced silicone solutions in battery thermal management systems. Key industry players like Shin-Etsu, Dow, and Wacker Chemie are expanding their portfolios to meet these evolving needs through R&D investments and strategic partnerships.

Silicone Materials for Automobiles Market – View in Detailed Research Report

MARKET DYNAMICS

MARKET DRIVERS

Growing Electric Vehicle Production Accelerates Silicone Material Demand

The rapid expansion of electric vehicle (EV) manufacturing is creating substantial demand for advanced silicone materials. With global EV sales projected to surpass 45 million units annually by 2030, automakers increasingly rely on silicones for battery thermal management systems, electrical insulation, and durable sealing solutions. Silicone’s thermal stability (maintaining properties between -55°C to 230°C) makes it indispensable in high-temperature EV battery environments where safety is paramount. Major OEMs now specify silicone-based materials for approximately 75% of gasket and seal applications in next-generation electric platforms.

Stringent Automotive Safety Regulations Drive Material Innovation

Global automotive safety standards are compelling manufacturers to adopt premium silicone solutions that outperform conventional materials. Recent crash test protocols require improved fire resistance and impact absorption—properties where silicone elastomers demonstrate 40‑60% better performance than rubber alternatives. The European Union’s latest vehicle safety package (GSR2) specifically mandates enhanced flammability resistance in interior components, directly benefiting flame‑retardant silicone formulations. Industry analysts estimate these regulations will drive a 12‑15% annual growth in silicone adoption for safety-critical applications through 2028.

Lightweighting Initiatives Boost Silicone Adoption

Automakers striving to improve fuel efficiency are replacing metal components with silicone composites that offer comparable strength at 30‑50% weight reduction. The average vehicle now incorporates over 7 kilograms of silicone materials, representing a 22% increase since 2020. This trend is particularly pronounced in luxury and electric segments, where every 10% weight reduction can extend range by 6‑8%. Leading manufacturers are developing silicone-based adhesives that bond dissimilar materials while maintaining structural integrity, enabling mixed-material vehicle architectures without compromising crash performance.

MARKET RESTRAINTS

Volatile Raw Material Prices Create Cost Pressures

The silicone materials market faces significant challenges from fluctuating prices of key feedstocks like silicon metal and methanol, which account for 60‑70% of production costs. Recent supply chain disruptions have caused silicon metal prices to swing between USD 2,800‑USD 3,500 per metric ton, making long‑term pricing agreements difficult. These input cost variations are particularly problematic for small automotive suppliers operating on fixed‑price contracts, forcing some to absorb 15‑20% margin compression rather than risk losing OEM business.

Complex Recycling Requirements Limit End-of-Life Options

While silicone materials offer excellent durability, their chemical stability creates recycling challenges under emerging circular economy regulations. Current mechanical recycling methods recover only about 35% of silicone content from end-of-life vehicles, with the remainder typically landfilled. The European Union’s upcoming ELV Directive revisions may impose stricter material recovery targets, potentially requiring costly investments in chemical depolymerization technologies that can add USD 50‑USD 75 per vehicle in recycling costs.

Alternative Material Development Presents Competitive Threat

Advanced thermoplastic elastomers (TPEs) and bio-based polymers are capturing market share in applications where ultimate temperature resistance isn’t critical. These alternatives now offer 80‑90% of silicone’s performance at 30‑40% lower cost in seal and gasket applications. While silicones maintain dominance in extreme environments, material scientists estimate next-generation TPE formulations could displace 15‑20% of current silicone automotive applications within five years, particularly in interior and non‑critical exterior components.

MARKET OPPORTUNITIES

Automotive Electronics Expansion Creates New Application Frontiers

The proliferation of advanced driver assistance systems (ADAS) and autonomous vehicle technologies is driving unprecedented demand for specialized silicone materials. High-purity silicone gels are becoming essential for protecting sensitive electronic components from vibration and thermal cycling, with global demand projected to grow at 18% CAGR through 2030. Leading suppliers are developing electrically conductive silicone adhesives that simultaneously provide thermal management and electromagnetic interference shielding—a dual-function solution currently adopted in over 60% of premium vehicle radar systems.

Regional Manufacturing Shifts Open New Growth Markets

The gradual relocation of automotive production to Southeast Asia and Mexico creates substantial opportunities for local silicone material suppliers. With vehicle production in ASEAN countries expected to grow by 5‑7% annually, regional silicone demand could reach USD 850 million by 2027. Major manufacturers are establishing captive production facilities near emerging automotive hubs, reducing logistics costs by 20‑25% while improving just‑in‑time delivery capabilities that are critical for modern assembly plants.

Custom Formulation Services Differentiate Market Leaders

Automakers increasingly seek application-specific silicone solutions tailored to their proprietary vehicle architectures. This trend has spurred development of rapid prototyping services that can deliver custom silicone formulations in as little as 4‑6 weeks, compared to the traditional 12‑16 week development cycle. The premium pricing available for these engineered solutions (typically 25‑40% above standard grades) is attracting significant R&D investment, with leading suppliers now allocating 15‑20% of their development budgets to co‑engineering projects with major OEMs.

Segment Analysis:

By Type

Silicone Elastomer Segment Dominates Due to High Demand for Durable Automotive Components

The market is segmented based on type into:

- Silicone Elastomer

- Silicone Resin

- Silicone Gel

- Silicone Oil

- Others

By Application

Passenger Cars Segment Leads Due to Increasing Vehicle Production Globally

The market is segmented based on application into:

- Passenger Cars

- Commercial Vehicles

By Product Form

Liquid Silicone Rubber Gains Traction for Precision Automotive Parts

The market is segmented based on product form into:

- Liquid Silicone Rubber (LSR)

- Solid Silicone

- Gels & Pastes

- Coatings

By Function

Sealing & Bonding Applications Drive Significant Market Demand

The market is segmented based on function into:

- Sealing

- Bonding

- Thermal Management

- Electrical Insulation

Key Industry Players

Leading Companies Drive Innovation in Silicone Automotive Solutions

🔟 1. Shin‑Etsu Chemical Co., Ltd.

Headquarters: Tokyo, Japan

Key Offering: Silicone elastomers, sealants, and thermal management solutions for EVs

Shin‑Etsu is the world leader in silicone chemistry, supplying high-performance elastomers used in battery thermal management, electrical insulation, and vibration damping across the automotive sector. Their portfolio spans from low-viscosity gels to high-temperature resins, enabling OEMs to meet stringent safety and efficiency standards.

Sustainability & Growth Initiatives:

- Investing USD 150 million in R&D for flame-retardant and bio-based silicone formulations

- Strategic partnership with Panasonic to co-develop battery thermal interface materials

- Commitment to reduce carbon footprint by 30% in production by 2030

9️⃣ 2. Dow Inc.

Headquarters: Midland, Michigan, USA

Key Offering: High-performance silicone elastomers and specialty coatings for automotive interiors and exteriors

Dow’s silicone solutions are integral to lightweighting initiatives, providing superior impact absorption and fire resistance. The company’s focus on advanced composites supports EV manufacturers in reducing weight while maintaining structural integrity.

Sustainability & Growth Initiatives:

- Launch of a circular economy program to recycle used silicone components

- Partnership with Volkswagen to supply low-temperature silicone adhesives for electric drivetrains

- Investment in renewable energy for manufacturing facilities to lower operational emissions

8️⃣ 3. Wacker Chemie AG

Headquarters: Dresden, Germany

Key Offering: Flame-retardant silicone elastomers and thermal interface materials for battery packs

Wacker’s silicone solutions are engineered to meet the highest safety standards, enabling EV manufacturers to comply with GSR2 and other regulatory frameworks. Their R&D centers focus on high-temperature stability and reduced flammability.

Sustainability & Growth Initiatives:

- Acquisition of a Chinese specialty silicone producer to strengthen EV supply chain

- Development of bio-based silicone resins with lower environmental impact

- Targeted reduction of CO₂ emissions by 25% in production by 2035

7️⃣ 4. Momentive Performance Materials Inc.

Headquarters: Westlake, Ohio, USA

Key Offering: Liquid Silicone Rubber (LSR) for precision automotive components

Momentive’s LSR products are used in high-precision gaskets, seals, and vibration dampers. Their formulations offer excellent dimensional stability across wide temperature ranges, making them ideal for EV power electronics and sensor housings.

Sustainability & Growth Initiatives:

- Partnership with BMW to develop low-flammability LSR for electric drivetrain assemblies

- Investment in sustainable manufacturing practices, including waste heat recovery

- Launch of a rapid prototyping service for custom silicone solutions in 4‑6 weeks

6️⃣ 5. Elkem ASA

Headquarters: Oslo, Norway

Key Offering: Silicone resins and specialty coatings for automotive applications

Elkem’s silicone resins are used in high-performance coatings that protect vehicle interiors from UV degradation and enhance durability. Their focus on European markets includes compliance with REACH regulations and the European Green Deal.

Sustainability & Growth Initiatives:

- Joint venture with local Chinese producers to expand silicone resin capacity

- Investment in renewable energy for manufacturing sites

- Goal to achieve zero waste to landfill by 2030

5️⃣ 6. DuPont de Nemours, Inc.

Headquarters: Wilmington, Delaware, USA

Key Offering: Advanced silicone gels for thermal management in EV battery packs

DuPont’s silicone gels provide superior heat transfer and electrical insulation, critical for maintaining battery safety and performance. Their formulations are used in high-density battery modules and power electronics.

Sustainability & Growth Initiatives:

- Research into biodegradable silicone additives

- Collaboration with Tesla for next-generation battery thermal interface materials

- Reduction of water usage in production by 20% by 2032

4️⃣ 7. KCC Corporation

Headquarters: Seoul, South Korea

Key Offering: Silicone sealants and adhesives for automotive aftermarket and OEM markets

KCC supplies high-performance sealants used in gaskets, hoses, and body panels. Their competitive pricing and rapid delivery make them a preferred partner for emerging automotive hubs in Southeast Asia.

Sustainability & Growth Initiatives:

- Development of low VOC silicone formulations for compliance with global emission standards

- Expansion of manufacturing capacity in Vietnam to support local EV production

- Investment in AI-driven supply chain optimization

3️⃣ 8. CHT Group

Headquarters: Hamburg, Germany

Key Offering: Silicone-based adhesives for automotive electronics and sensors

CHT’s adhesives are critical for bonding sensor modules and high-voltage components. Their formulations provide excellent thermal conductivity and electrical insulation, supporting advanced driver assistance systems.

Sustainability & Growth Initiatives:

- Partnership with Audi to develop self-healing silicone coatings for exterior sensors

- Investment in renewable energy to power production facilities

- Goal to reduce plastic waste by 30% in packaging by 2035

2️⃣ 9. ELKAY Chemicals Pvt. Ltd.

Headquarters: Pune, India

Key Offering: Silicone resins and gels for automotive interior applications

ELKAY supplies silicone resins used in seat cushions, dashboards, and sound insulation. Their focus on the Indian market includes compliance with local safety standards and cost-competitive solutions for the growing domestic automotive industry.

Sustainability & Growth Initiatives:

- Launch of a low-cost, high-performance silicone gel for EV battery thermal management

- Investment in solar-powered production units to reduce energy costs

- Collaboration with local OEMs to develop custom silicone formulations

1️⃣ 10. SiSiB SILICONES

Headquarters: Shanghai, China

Key Offering: Specialty silicone oils and lubricants for automotive components

SiSiB provides silicone oils used in hydraulic systems, cooling circuits, and lubrication of moving parts. Their products are valued for high-temperature stability and low viscosity, essential for electric vehicle cooling systems.

Sustainability & Growth Initiatives:

- Development of biodegradable silicone lubricants for reduced environmental impact

- Partnership with BYD to supply silicone oils for battery cooling

- Investment in advanced polymerization technology to lower production costs by 15%

Download FREE Sample Report: Silicone Materials for Automobiles Market – View in Detailed Research Report

Get Full Report Here: Silicone Materials for Automobiles Market – View in Detailed Research Report

🌍 Outlook: The Future of Silicone Materials in Automobiles

As global automotive production continues to shift towards electrification and sustainability, silicone materials are poised to play a pivotal role in ensuring safety, efficiency, and performance. The combination of high thermal stability, lightweight characteristics, and compliance with evolving safety regulations positions silicone as a cornerstone material for next-generation vehicles.

📊 Key Trends Shaping the Market

- Rapid expansion of EV production driving demand for advanced thermal management silicones.

- Growing focus on lightweighting and material substitution leading to increased silicone adoption.

- Emergence of self-healing and conductive silicone coatings for sensor protection.

- Increased investment in sustainable and bio-based silicone formulations.

- Strategic partnerships between silicone suppliers and OEMs to co-develop custom solutions.

📈 Forecast (2025‑2034)

- Base Year (2025): USD 4.20 billion

- Estimated (2026): USD 4.55 billion

- Forecast (2034): USD 8.10 billion, reflecting a sustained CAGR of 6.9% over the period.

- Top 10 Companies in the Agar Market (2026): Market Leaders Powering Global Innovation - July 25, 2026

- Top 10 Companies in the Optical Brightener ER-I and ER-II Market (2026): Market Leaders Powering Global Demand - July 25, 2026

- Top 10 Companies in the Global Liquid Applied Membrane System Market (2026): Market Leaders Shaping Global Waterproofing Solutions - July 25, 2026