MARKET INSIGHTS

Lawn gardening consumables are the replenishable products used to establish, feed, protect and finish lawns, garden beds and container plantings, items that need regular replacement rather than durable tools.

They include fertilisers and soil amendments, grass and flower seeds, mulches and topsoils, weed and pest control products, seed treatments and starter soils, water additives and plant nutrients, peat and compost products, and single‑use materials such as seed tapes, tree stakes, and seasonal soil covers.

|

Lawn Gardening Consumables Market Value (2025) |

USD 24.8 billion |

|

Lawn Gardening Consumables Market Value (2032) |

USD 37.6 billion |

|

CAGR (%) |

4.7% |

Imagine your neighbour turning a postage‑stamp front yard into a busy native pollinator patch with a cheap packet of native wildflower seed, or a city park replacing monthly pesticide sprays with targeted biological controls to attract birds. Instead, those little refill items are the market behind every green revival and backyard makeover.

Simple consumables, from a bag of slow‑release fertiliser to a micro‑mulch blanket, drive how quickly outdoor areas can alter, how much care costs, and how green a neighbourhood looks at the end of the season.

Key Takeaways:

- Fertilisers dominate because they directly enable growth, feed depleted soils, and give immediate visible results that justify repeat purchases.

- Residential leads: homeowners and renters are the main repeat purchasers, driven by landscaping trends, home improvement funding, and social‑media‑fueled lawn makeovers.

Lawn and Gardening Consumables Market – View in Detailed Research Report

MARKET DYNAMICS

MARKET DRIVERS

Growing Urbanization and Home Gardening Trends Accelerate Market Expansion

Global urban population has surpassed 4.4 billion people, creating unprecedented demand for residential green spaces. This urban density, combined with increasing disposable incomes, is driving remarkable growth in home gardening activities. Approximately 55% of urban households now participate in some form of gardening, creating sustained demand for fertilisers, seeds, and plant care products. Professional landscaping services are also experiencing a boom, particularly in North America where the commercial landscaping market grew by nearly 6.3% annually from 2020 to 2024.

Climate Change Concerns Fuel Eco‑Friendly Product Innovation

Environmental consciousness among consumers has reached new heights, with 72% of gardeners now preferring organic or sustainable products. This shift is prompting manufacturers to develop innovative solutions like slow‑release fertilisers, biocontrol pesticides, and water‑retentive growth media. The organic lawn care segment is projected to grow at a CAGR of 8.1% through 2032, significantly outpacing conventional products. Recent product launches include phosphate‑free fertilisers and bee‑friendly herbicides that meet stringent environmental regulations while maintaining efficacy.

➤ The biodegradable mulch film market, while currently representing just 15% of total mulch sales, is expected to triple in value by 2028 as municipalities implement strict plastic regulations.

Furthermore, the integration of smart gardening technologies with traditional consumables is creating new growth avenues. Sensor‑based fertilisation systems and app‑connected pest control solutions are gaining traction, particularly among tech‑savvy younger homeowners who value convenience and data‑driven plant care.

MARKET RESTRAINTS

Regulatory Pressures and Input Cost Volatility Constrain Growth

The industry faces mounting regulatory challenges as over 40 countries have implemented stricter controls on synthetic pesticides and fertilisers in the past five years. Compliance costs have risen approximately 18‑22% since 2020, disproportionately affecting small and mid‑sized manufacturers. Concurrently, raw material prices remain highly volatile – key ingredients like urea and potash have seen price fluctuations exceeding 35% annually, making inventory management and pricing strategies increasingly complex.

Other Restraints

Labor Shortages

The landscaping industry reports 12‑15% vacancy rates for skilled workers in major markets, limiting service expansion and product adoption. This shortage is particularly acute for specialised roles like turf management specialists and arborists, where certification requirements create entry barriers.

Weather Variability

Unpredictable weather patterns, including extended droughts in traditional gardening regions, are altering consumption patterns. Areas affected by water restrictions have seen 20‑25% declines in traditional lawn care product sales, though drought‑resistant alternatives are gaining ground.

MARKET CHALLENGES

Consumer Misconceptions and Product Efficacy Concerns Create Adoption Barriers

Despite technological advancements, many consumers remain skeptical about newer gardening solutions. A recent survey revealed that 43% of homeowners distrust organic pest control effectiveness, while 61% overestimate fertiliser application rates. This knowledge gap leads to product misuse and dissatisfaction, particularly with premium‑priced sustainable alternatives. Manufacturers must invest heavily in education while combating deep‑rooted gardening traditions that favour conventional methods.

Additionally, the market faces persistent issues with product standardisation and labeling accuracy. Cases of mislabelled organic content or exaggerated performance claims have led to increased regulatory scrutiny and consumer reluctance. The industry reports an average of 3‑5 major product recalls annually related to labeling inaccuracies or contamination concerns.

MARKET OPPORTUNITIES

Smart Gardening Integration and Premium Subscription Models Open New Revenue Streams

The convergence of IoT technologies with traditional gardening practices presents a $2.8 billion opportunity by 2028. Connected soil sensors that sync with automated fertilisation systems are gaining particular traction, with adoption rates growing 28% year‑over‑year in premium residential segments. Leading manufacturers are partnering with tech firms to develop integrated solutions that combine consumables with digital monitoring for optimised plant health.

Meanwhile, subscription‑based lawn care services are disrupting traditional retail models. These services, which deliver customised product blends based on soil tests and seasonal needs, have achieved 75% customer retention rates in pilot markets. The model proves particularly effective for time‑constrained urban professionals who value convenience but lack gardening expertise. Early adopters report 30‑40% higher annual customer spending compared to traditional DIY purchasers.

➤ Regional specialty products tailored to microclimates represent another untapped opportunity, with drought‑resistant grass seed blends for arid regions demonstrating 50% faster growth than standard varieties.

The commercial sector also shows strong potential, particularly in the sports turf and golf course segments, where precision turf management systems demand high‑performance consumables. These professional markets typically generate 3‑5 times the revenue per acre compared to residential applications, with greater tolerance for premium‑priced specialty products.

Segment Analysis:

| Segment Category | Sub‑Segments | Key Insights |

|---|---|---|

| By Type | Fertilisers

Seeds

Pesticides

Others

|

Fertilisers dominate due to their critical role in providing essential nutrients for plant growth and soil health. |

| By Application |

|

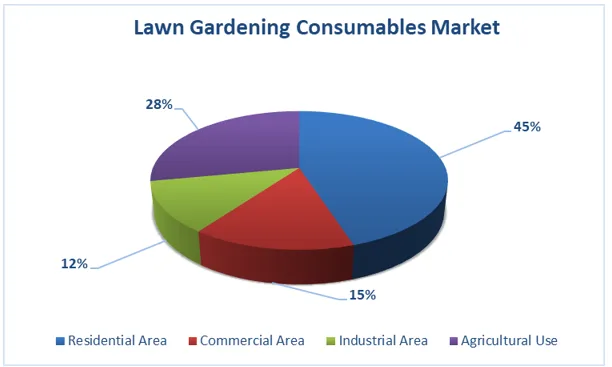

Residential Area leads due to increasing home gardening and landscaping activities among homeowners. |

| By End User |

|

Homeowners and Individual Consumers account for the largest share driven by rising interest in personal outdoor spaces. |

| By Distribution Channel | Online Retail

Offline Retail

|

Offline Retail leads consumption due to hands‑on product selection and immediate availability for consumers. |

By Application:

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The competitive landscape of the Lawn and Gardening Consumables market is semi‑consolidated, featuring a mix of large multinational corporations, medium‑sized specialists, and smaller regional players. BASF SE stands out as a leading force in this space, driven by its extensive range of fertilisers, pesticides, and seeds, coupled with a robust global footprint that spans North America, Europe, Asia‑Pacific, and beyond. The company’s commitment to sustainable agriculture solutions has solidified its position, particularly in eco‑friendly pest control and nutrient management products that align with growing consumer demands for environmentally responsible options.

Corteva Agriscience and The Andersons, Inc. also commanded substantial market shares in 2024. Their success stems from innovative offerings tailored to both residential and commercial users, including high‑performance grass seeds and organic fertilisers that support resilient lawn growth. Because of strong distribution networks and focus on research‑driven product development, these firms have effectively captured segments like urban gardening and professional landscaping, where demand for reliable consumables continues to rise.

Furthermore, ongoing growth strategies such as geographic expansions into emerging markets in Asia‑Pacific and South America, alongside frequent new product launches—like advanced bio‑based pesticides—are poised to significantly boost their market presence through the forecast period ending in 2032. This dynamic approach helps them navigate challenges like regulatory pressures on chemical usage while capitalising on trends toward sustainable gardening practices.

Meanwhile, Espoma Company and Premier Tech are bolstering their standings through heavy investments in R&D, key partnerships with retailers, and expansions into organic and natural consumables. For instance, Espoma’s emphasis on soil amendments and natural fertilisers has resonated with eco‑conscious homeowners, ensuring steady growth amid a market projected to expand from USD 10,840 million in 2023 to USD 14,268 million by 2032 at a CAGR of 3.10%. These efforts not only enhance product diversity but also foster long‑term loyalty in a competitive environment where innovation and sustainability are paramount. However, smaller players must contend with supply chain disruptions and raw material volatility, prompting strategic alliances to maintain viability. Overall, the landscape encourages collaboration and adaptation, as companies vie to meet the evolving needs of residential, commercial, and industrial applications worldwide.

List of Key Lawn and Gardening Consumables Companies Profiled

- BASF SE (Germany)

- Corteva Agriscience (U.S.)

- The Andersons, Inc. (U.S.)

- J.R. Simplot Company (U.S.)

- Espoma Company (U.S.)

- Premier Tech (Canada)

- Agrium Inc. (Nutrien Ltd.) (Canada)

- Ferry‑Morse Seed Company (U.S.)

- Ace Hardware Corporation (U.S.)

Top 10 Companies in the Lawn and Gardening Consumables Market (2026)

-

BASF SE

Headquarters: Ludwigshafen, Germany

Key Offering: Comprehensive fertiliser, pesticide, and seed portfolio with a focus on sustainability.BASF’s global R&D network drives continuous innovation, delivering slow‑release fertilisers and bio‑based pesticides that meet stringent environmental standards. The company’s robust distribution network ensures high market penetration across North America, Europe, and Asia‑Pacific.

Sustainability & Growth Initiatives:

- Investing €1.5 billion in bio‑based product development by 2030.

- Expanding its organic fertiliser line to capture the 72% of consumers favouring eco‑friendly solutions.

- Partnering with smart‑gardening platforms to integrate data‑driven fertilisation systems.

-

Corteva Agriscience

Headquarters: Raleigh, North Carolina, USA

Key Offering: High‑performance grass seeds, organic fertilisers, and precision pest control.Corteva’s focus on research‑driven solutions positions it as a leader in urban and commercial landscaping. The company’s “Green‑Growth” initiative aligns with the growing demand for low‑water, high‑efficacy products.

Sustainability & Growth Initiatives:

- Launching a plant‑based herbicide line by 2028.

- Expanding into emerging markets in Asia‑Pacific with tailored seed blends.

- Investing in IoT‑enabled soil sensors to reduce chemical usage.

-

The Andersons, Inc.

Headquarters: McKinney, Texas, USA

Key Offering: Premium grass seeds, organic fertilisers, and turf management solutions.The Andersons leverages its deep expertise in turf science to deliver products that meet the rigorous demands of sports turf and golf courses.

Sustainability & Growth Initiatives:

- Developing drought‑resistant seed blends for arid regions.

- Collaborating with universities for precision agronomy research.

- Integrating digital monitoring into fertiliser application.

-

J.R. Simplot Company

Headquarters: Boise, Idaho, USA

Key Offering: Bulk fertilisers, seed blends, and specialty soil amendments.Simplot’s extensive manufacturing capacity supports large‑scale commercial landscaping and agricultural clients, while its commitment to sustainable farming practices drives product innovation.

Sustainability & Growth Initiatives:

- Reducing greenhouse gas emissions by 20% in production by 2035.

- Investing in regenerative agriculture programmes.

- Expanding the use of recycled packaging.

-

Espoma Company

Headquarters: Portland, Oregon, USA

Key Offering: Natural fertilisers, composts, and soil amendments.Espoma’s focus on organic, non‑synthetic products appeals to eco‑conscious homeowners and small‑scale growers.

Sustainability & Growth Initiatives:

- Expanding the range of peat‑free composts.

- Partnering with local farms for regenerative sourcing.

- Launching a subscription service for seasonal fertiliser mixes.

-

Premier Tech

Headquarters: Montreal, Quebec, Canada

Key Offering: Organic fertilisers, soil conditioners, and specialty seed blends.Premier Tech’s emphasis on R&D and eco‑friendly formulations positions it as a key player in the North American organic segment.

Sustainability & Growth Initiatives:

- Developing bio‑based pest control solutions.

- Investing in smart‑gardening app integration.

- Expanding distribution through e‑commerce partnerships.

-

Agrium Inc. (Nutrien Ltd.)

Headquarters: Saskatoon, Saskatchewan, Canada

Key Offering: High‑yield fertilisers, seed blends, and precision agronomy tools.Agrium’s global reach and advanced analytics enable it to deliver tailored solutions to both commercial and residential markets.

Sustainability & Growth Initiatives:

- Launching a low‑phosphate fertiliser line.

- Investing in carbon‑capture technologies for production.

- Expanding its digital agronomy platform.

-

Ferry‑Morse Seed Company

Headquarters: Lubbock, Texas, USA

Key Offering: Premium seed blends for lawns, gardens, and sports turf.Ferry‑Morse’s focus on high‑quality seed technology supports both residential and commercial clients.

Sustainability & Growth Initiatives:

- Developing drought‑tolerant seed varieties.

- Implementing sustainable seed‑production practices.

- Partnering with local municipalities for green‑space projects.

-

Ace Hardware Corporation

Headquarters: Boise, Idaho, USA

Key Offering: Retail distribution of fertilisers, seeds, and gardening consumables.Ace Hardware’s extensive retail network and focus on customer education drive market penetration and repeat sales.

Sustainability & Growth Initiatives:

- Expanding the range of eco‑friendly gardening products.

- Launching in‑store workshops on sustainable gardening.

- Implementing a loyalty programme for frequent buyers.

Download FREE Sample Report: Lawn and Gardening Consumables Market – View in Detailed Research Report

Get Full Report Here: Lawn and Gardening Consumables Market – View in Detailed Research Report

Outlook

The Lawn and Gardening Consumables market is set to expand from USD 24.8 billion in 2025 to USD 37.6 billion by 2032, reflecting a robust CAGR of 4.7%. Growth will be driven by rising urbanisation, increasing disposable income, and a strong shift towards eco‑friendly products. Smart‑gardening technologies and subscription models will create new revenue streams, while regulatory pressures will continue to shape product innovation.

Future Trends

- Smart‑gardening integration with IoT and data analytics.

- Subscription‑based lawn care services targeting urban professionals.

- Expansion of organic and non‑toxic fertiliser lines.

- Growth of regional specialty products for microclimates.

- Increased focus on drought‑resistant seed blends and water‑retentive media.

- Digital platforms for personalised product recommendations.

- Top 10 Companies in the High Purity Composites Market (2026): Market Leaders Driving Global Innovation - July 13, 2026

- Europe Cure in Place Gasket Material Market (2026): Market Leaders Powering Growth - July 13, 2026

- Top 10 Companies in the Two‑Sided Conductive Tape Market (2026): Market Leaders Driving Innovation - July 13, 2026