MARKET INSIGHTS

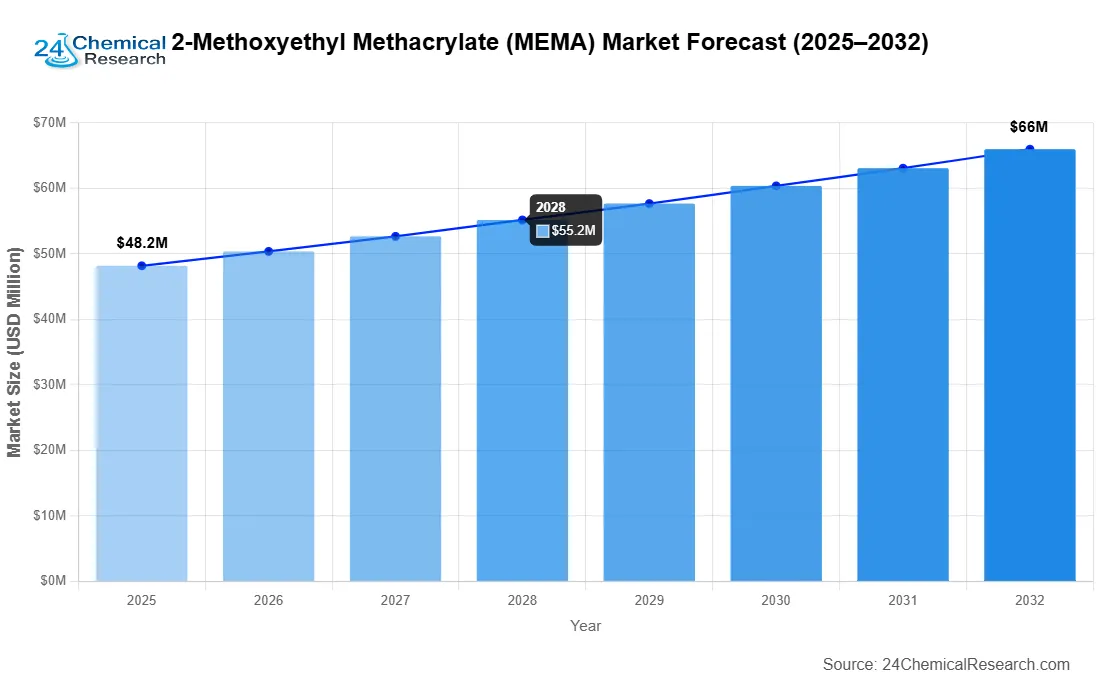

Global 2-Methoxyethyl Methacrylate (MEMA) market was valued at USD 46.2 million in 2024 and is projected to reach USD 48.2 million in 2025 to USD 68.9 million by 2032, growing at a CAGR of 4.6% during the forecast period.

2-Methoxyethyl Methacrylate (CAS 6976-93-8) is a colorless transparent liquid with the molecular formula C7H12O3. This methacrylate ester compound serves as a functional monomer with critical applications in photosensitive resins, coatings, adhesives, and specialized industries like photolithography and medical materials. Its unique properties enable use in high-performance coatings and emerging fields such as microelectronics manufacturing.

Market growth is driven by increasing demand from ocean coating applications, where MEMA’s corrosion-resistant properties are highly valued, particularly in marine infrastructure. The biological materials segment is also expanding due to rising healthcare investments, with MEMA being utilized in biocompatible polymer formulations. However, supply chain fluctuations in raw materials like methacrylic acid present moderate challenges. Key players including Mitsubishi Chemical and Fushun Donglian Anxin Chemical are focusing on production capacity expansions to meet the growing regional demand from Asia-Pacific markets.

2-Methoxyethyl Methacrylate (MEMA) Market – View in Detailed Research Report

MARKET DYNAMICS

MARKET DRIVERS

Expanding Applications in Photolithography and Microelectronics to Fuel Demand

Semiconductor industry’s rapid advancement is creating significant demand for MEMA in photolithography applications. As chip manufacturers push toward smaller nanometer nodes, the need for high-precision photoresists containing MEMA has grown substantially. The global semiconductor photoresist market, which relies heavily on methacrylate monomers, is projected to maintain a CAGR of over 6% through 2030. MEMA’s unique properties – including excellent adhesion, resolution, and etching resistance – make it indispensable for advanced photolithography processes. Major foundries are expanding production capacities, with planned investments exceeding $200 billion in new fabrication facilities worldwide, directly driving MEMA consumption.

Growth in Marine Coatings Market to Accelerate Adoption

The marine coatings sector presents a robust growth opportunity for MEMA, particularly in antifouling applications where its chemical resistance and durability are highly valued. With global seaborne trade volumes expected to grow by 3-4% annually, coupled with increasing environmental regulations on biocidal coatings, MEMA-based alternatives are gaining traction. The compound’s ability to reduce biofouling while meeting stringent VOC regulations has led coating manufacturers to reformulate products with MEMA-containing polymers. The marine coatings market is anticipated to reach $6 billion by 2027, with Asia-Pacific accounting for over 50% of demand, creating substantial opportunities for MEMA suppliers in this region.

Biomedical Material Innovations Creating New Application Areas

Advancements in biomedical materials are opening new avenues for MEMA utilization, particularly in drug delivery systems and bioadhesives. The polymer’s biocompatibility and tunable properties make it suitable for controlled-release formulations and medical device coatings. The global drug delivery market, valued at over $500 billion, is witnessing increased adoption of methacrylate-based polymers for targeted therapies. Furthermore, developments in dental composites and bone cements are incorporating MEMA derivatives, with the dental materials segment alone projected to grow at 5% annually through 2030. These emerging applications position MEMA as a versatile monomer with expanding healthcare applications.

MARKET RESTRAINTS

Volatility in Raw Material Prices Impacting Production Costs

The MEMA market faces significant challenges from fluctuating prices of key raw materials like methacrylic acid and ethylene oxide. Over the past two years, raw material costs have seen swings of up to 40%, forcing manufacturers to absorb margin pressures or adjust prices frequently. Such instability discourages long-term contracts and makes budgeting difficult for downstream users, ultimately slowing market growth.

Other Restraints

Environmental Regulations

Increasingly stringent VOC and chemical manufacturing regulations pose compliance challenges for MEMA producers. The EU’s REACH regulations and similar frameworks in North America and Asia require substantial investments in emission control technologies, adding to production costs.

Supply Chain Vulnerabilities

Geopolitical tensions and trade restrictions have exposed vulnerabilities in the global chemical supply chain, affecting MEMA availability. Recent disruptions in key shipping lanes and export controls on precursor chemicals have led to regional shortages and extended lead times.

MARKET CHALLENGES

Technical Limitations in High-Performance Applications

While MEMA offers numerous advantages, certain technical limitations constrain its adoption in cutting-edge applications. In semiconductor lithography, the push toward extreme ultraviolet (EUV) technologies requires photoresists with exceptional sensitivity and resolution—parameters where MEMA-based formulations sometimes fall short compared to newer specialty monomers. Similarly, in biomedical applications, concerns about long-term stability under physiological conditions limit MEMA’s use in implantable devices. Ongoing R&D investments are essential to maintain competitiveness.

Workforce and Knowledge Gaps

The specialized nature of methacrylate chemistry has created knowledge gaps in the workforce, particularly in regions experiencing rapid industrial expansion. The pool of chemists and engineers proficient in methacrylate polymerization has not kept pace with industry growth, leading to operational inefficiencies and quality control issues at some production facilities.

MARKET OPPORTUNITIES

Development of Green Chemistry Alternatives

The shift toward sustainable chemistry presents significant opportunities for MEMA innovation. Bio-based routes to MEMA production using renewable feedstocks are gaining attention, with several pilot projects demonstrating technical feasibility. The global green chemicals market, projected to exceed USD20 billion by 2027, could provide a substantial growth avenue for MEMA producers investing in sustainable production methods and circular economy initiatives.

Emerging Markets Present Untapped Potential

Developing economies in Southeast Asia, Africa, and Latin America represent largely untapped markets for MEMA applications. As these regions industrialize and their electronics, automotive, and construction sectors expand, demand for high-performance materials including MEMA is expected to surge. Strategic market entry through local partnerships or production joint ventures could enable suppliers to capitalize on this growth potential while navigating regional regulatory and logistical challenges.

MARKET TRENDS

Expansion of High-Performance Coatings Drives Market Growth

Global 2-Methoxyethyl Methacrylate (MEMA) market is experiencing robust growth, largely driven by its increasing application in high-performance coatings, particularly in marine and industrial environments. MEMA’s unique properties—excellent adhesion, weather resistance, and durability under harsh conditions—make it an ideal component in anticorrosive coatings for ships, offshore platforms, and coastal infrastructure. With the marine coatings market projected to grow at a steady rate of 4–6% annually, the demand for MEMA is expected to rise in parallel. Regulatory pressures to reduce volatile organic compounds (VOCs) in coatings further accelerate adoption of MEMA-based formulations, offering lower environmental impact compared to traditional alternatives.

Other Trends

Growing Role in Biomedical Applications

The biomedical sector is emerging as a key consumer of MEMA, particularly in the development of biocompatible materials for medical devices, drug delivery systems, and tissue engineering. MEMA’s ability to enhance the hydrophilicity and flexibility of polymers makes it valuable for contact lenses, wound dressings, and orthopedic implants. The global biomedical materials market, valued at over $130 billion, underscores the vast potential for MEMA in this segment. Advancements in 3D printing technology are unlocking new opportunities, as MEMA-based resins are increasingly used to create patient-specific medical devices with high precision and biocompatibility.

Increasing Adoption in Microelectronics and Photolithography

The electronics industry is another major driver for the MEMA market, with rising demand for high-resolution photoresists used in semiconductor manufacturing. As the push for miniaturization in microelectronics continues, MEMA’s role in formulating advanced photolithography materials becomes critical—enabling the production of smaller, more efficient chips. The semiconductor industry, which surpassed $600 billion in revenue, relies heavily on specialty chemicals like MEMA to maintain technological progress. The expansion of flexible electronics and printed circuit boards (PCBs) further broadens MEMA’s applications, reinforcing its position as a vital material in next-generation electronic components.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Innovation & Strategic Partnerships to Capture Growth

🔟 1. Mitsubishi Chemical Corporation

Headquarters: Tokyo, Japan

Key Offering: Functional monomer MEMA for high-performance photoresists, marine coatings, and biomedical polymers

Mitsubishi Chemical leverages its extensive production capabilities and R&D expertise in methacrylate chemistry to supply high-purity MEMA grades (≥99%) to semiconductor foundries and marine coating manufacturers worldwide. The company’s advanced purification processes ensure superior adhesion and etching resistance, meeting the stringent requirements of next-generation lithography.

Sustainability Initiatives:

- Investing in renewable feedstock projects to reduce fossil-based inputs.

- Deploying closed-loop water recycling in production plants.

- Partnering with semiconductor fabs to develop low-VOC photoresist formulations.

9️⃣ 2. Fushun Donglian Anxin Chemical Co., Ltd.

Headquarters: Fushun, China

Key Offering: Cost-competitive MEMA for coatings, adhesives, and specialty polymers

Fushun Donglian Anxin focuses on large-scale production of MEMA, targeting the booming Chinese marine coating and PCB manufacturing sectors. The company has recently expanded its capacity by 25% and introduced a new high-purity line to capture the semiconductor market.

Sustainability Initiatives:

- Implementing energy-efficient distillation units.

- Reducing VOC emissions through advanced scrubbing systems.

- Collaborating with local universities on green methacrylate research.

8️⃣ 3. Shanghai Hechuang Chemical Co., Ltd.

Headquarters: Shanghai, China

Key Offering: MEMA for industrial coatings and specialized adhesives

Shanghai Hechuang has built a reputation for rapid product customization, enabling coating manufacturers to tailor MEMA-based formulations to specific marine or automotive applications. The firm’s agile supply chain allows quick response to market shifts.

Sustainability Initiatives:

- Adopting biobased methacrylic acid feedstocks.

- Optimizing plant emissions to meet China’s 2025 air quality targets.

- Engaging in joint ventures with European coating firms for low-VOC solutions.

7️⃣ 4. Qingdao ZKHT Chemical Co., Ltd.

Headquarters: Qingdao, China

Key Offering: MEMA for marine antifouling and high-performance coatings

Qingdao ZKHT has strengthened its position through strategic partnerships with Japanese and Korean specialty chemical distributors, focusing on high-purity MEMA for the marine coatings segment. The company’s robust logistics network supports rapid delivery across Asia-Pacific.

Sustainability Initiatives:

- Investing in biorefinery projects to produce renewable methacrylic acid.

- Implementing zero-waste policies in the production line.

- Collaborating with marine research institutes on antifouling efficacy.

6️⃣ 5. Qingdao RENAS Polymer Material Co., Ltd.

Headquarters: Qingdao, China

Key Offering: Bio-compatible MEMA grades for medical device applications

Qingdao RENAS specializes in developing MEMA derivatives that meet stringent biocompatibility standards for drug delivery systems, contact lenses, and orthopedic implants. The company’s R&D team works closely with hospitals and research institutions to validate performance.

Sustainability Initiatives:

- Utilizing bio-based feedstocks for MEMA synthesis.

- Conducting life-cycle assessments for medical polymer products.

- Partnering with global pharma companies to scale production.

5️⃣ 6. Korea Petrochemicals Co., Ltd.

Headquarters: Seoul, South Korea

Key Offering: MEMA for advanced electronics and high-performance coatings

Korea Petrochemicals focuses on high-purity MEMA for the Korean semiconductor and display markets, supplying to major foundries and OLED manufacturers. The company emphasizes strict quality control and rapid turnaround times.

Sustainability Initiatives:

- Implementing hydrogen-based ethylene oxide production.

- Reducing carbon footprint through energy-efficient processes.

- Collaborating with the Korean Ministry of Environment on green chemistry standards.

4️⃣ 7. Sinopec Chemical Co., Ltd.

Headquarters: Beijing, China

Key Offering: MEMA for bulk industrial coatings and adhesives

Sinopec Chemical supplies MEMA to large-scale coating manufacturers across Asia and Europe. The company’s strategic location near petrochemical hubs enables cost-effective production.

Sustainability Initiatives:

- Investing in catalytic conversion of methacrylic acid to reduce waste.

- Adopting green solvent technologies in polymerization.

- Supporting regional recycling programs for chemical waste.

3️⃣ 8. BASF SE

Headquarters: Ludwigshafen, Germany

Key Offering: MEMA for high-performance coatings and specialty polymers

BASF’s MEMA portfolio serves the European automotive, aerospace, and electronics sectors. The company focuses on high-purity grades and offers custom formulation services.

Sustainability Initiatives:

- Developing bio-based methacrylic acid from renewable resources.

- Reducing VOC emissions through advanced catalytic processes.

- Partnering with EU research projects on sustainable coatings.

2️⃣ 9. Dow Chemical Company

Headquarters: Midland, United States

Key Offering: MEMA for advanced photoresists and industrial coatings

Dow Chemical supplies MEMA to semiconductor fabs and industrial coating manufacturers in North America and Latin America. The company’s focus on quality and reliability supports critical infrastructure projects.

Sustainability Initiatives:

- Implementing green chemistry principles across the production chain.

- Investing in renewable energy for manufacturing facilities.

- Collaborating with the US Department of Energy on carbon reduction.

1️⃣ 10. LG Chem

Headquarters: Seoul, South Korea

Key Offering: MEMA for battery electrolytes, coatings, and biomedical polymers

LG Chem’s MEMA portfolio supports the growing demand for high-performance materials in electric vehicle batteries, advanced coatings, and medical devices. The company’s integrated R&D and production capabilities enable rapid scaling.

Sustainability Initiatives:

- Developing bio-based methacrylate routes for battery materials.

- Reducing water usage through closed-loop systems.

- Partnering with global NGOs on sustainable chemical manufacturing.

2-Methoxyethyl Methacrylate (MEMA) Market – View in Detailed Research Report

2-Methoxyethyl Methacrylate (MEMA) Market – View in Detailed Research Report

🌍 Outlook: The Future of 2-Methoxyethyl Methacrylate (MEMA) Market

The MEMA market is poised for steady growth driven by expanding applications in microelectronics, marine coatings, and biomedical materials. Key drivers include:

- Continued investment in semiconductor fabrication facilities worldwide.

- Increasing demand for low-VOC and bio-compatible coatings.

- Strategic capacity expansions by leading manufacturers.

- Growing focus on circular economy and green chemistry initiatives.

📈 Key Trends Shaping the Market:

- Adoption of high-purity MEMA (≥99%) for advanced lithography and aerospace applications.

- Development of bio-based MEMA to meet sustainability targets.

- Expansion of MEMA usage in 3D printing resins for medical devices.

- Strategic partnerships between chemical producers and semiconductor fabs to co-develop specialized formulations.

- Increased regulatory focus on VOC and chemical safety, driving innovation in low-emission processes.

- Top 10 Companies in the Unwrought Copper Market (2026): Leaders Shaping Global Supply - July 11, 2026

- Top 10 Companies in the Global Nuclear Grade Zirconium Alloy Market (2026): Market Leaders Driving the Nuclear Materials Sector - July 11, 2026

- Top 10 Companies in the Precision Ceramic Balls Market (2026): Market Leaders Powering Global Innovation - July 11, 2026