MARKET INSIGHTS

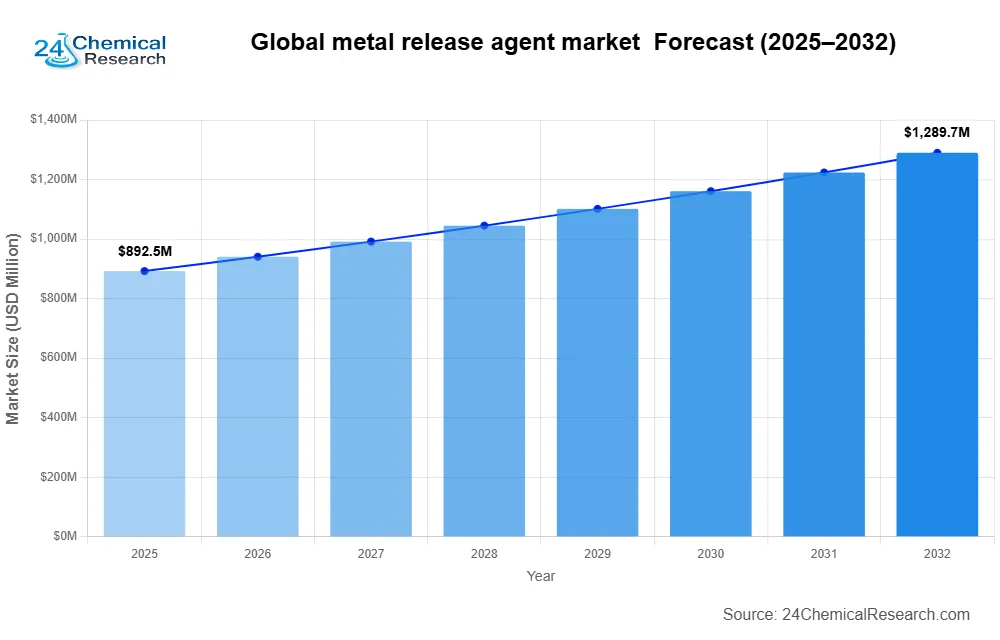

Global metal release agent market size was valued at USD 892.5 million in 2024 and is projected to reach USD 1.36 billion by 2032, growing at a CAGR of 5.4% during the forecast period.

Metal release agents, also known as mold release coatings, are chemical formulations applied to surfaces to prevent adhesion during manufacturing processes such as die‑casting, injection molding, and forging. These agents play a critical role in industries like automotive, mechanical engineering, and manufacturing by ensuring smooth material separation, reducing defects, and enhancing operational efficiency. The market is segmented into permanent and semi‑permanent agents, with permanent variants holding the majority share due to their long‑lasting performance.

Market expansion is primarily driven by increasing demand in the automotive sector, where lightweight metal components require efficient mold release solutions. Additionally, advancements in high‑performance formulations and the rising adoption of automation in manufacturing processes are accelerating growth. Key industry players such as Chem‑Trend, Henkel, and Dow are actively investing in R&D to develop eco‑friendly, low‑VOC formulations, addressing stringent environmental regulations. The U.S. and China remain dominant markets, accounting for a combined 45% of global revenue in 2024.

Metal Release Agent Market – View in Detailed Research Report

MARKET DYNAMICS

MARKET DRIVERS

Growing Demand from Automotive Industry Accelerates Market Expansion

The automotive sector’s increasing reliance on high‑performance metal casting processes is propelling the metal release agent market forward. With global vehicle production exceeding 85 million units annually, manufacturers are turning to release agents to enhance production efficiency and surface quality. These specialized formulations prevent metal adhesion during die casting and molding, reducing defects and downtime. The shift toward lightweight aluminum components in electric vehicles has further boosted demand, as aluminum casting applications grew by 12% year‑over‑year in 2023.

Advancements in Formulation Technologies Fuel Product Adoption

Recent breakthroughs in silicone‑based and water‑based release agent formulations are transforming manufacturing processes. New product developments focus on improving thermal stability up to 1,800°F while reducing environmental impact. The introduction of semi‑permanent coatings that withstand multiple release cycles has gained particular traction, with adoption rates increasing by 18% in foundry applications. These innovations address the dual demands of sustainability and performance, as manufacturers balance ecological concerns with production efficiency targets.

The development of nano‑engineered release agents has demonstrated a 30% improvement in surface finish quality while extending tool life by up to 40% in industrial trials. Additionally, the integration of Industry 4.0 technologies with release agent application systems enables precise computerized dosage control, reducing material waste by 15‑20% while maintaining optimal performance thresholds.

MARKET RESTRAINTS

Stringent Environmental Regulations Pose Compliance Challenges

The metal release agent market faces growing pressure from tightening environmental legislation worldwide. Recent VOC (Volatile Organic Compound) emission standards have forced formulation changes across North America and Europe, with compliance costs increasing by an average of 25% for manufacturers. The transition to water‑based and bio‑degradable alternatives presents technical hurdles in high‑temperature applications, where performance standards remain uncompromised. Foundries report a 12‑15% decrease in productivity during the transition period to compliant formulations.

Other Restraints

Price Volatility of Raw Materials

Fluctuations in silicone and petroleum‑based feedstock prices have created margin pressures, with key ingredient costs rising 22% year‑over‑year in Q1 2024. This volatility complicates long‑term pricing strategies and contract negotiations across the supply chain.

Adoption Barriers in Emerging Markets

While mature markets readily adopt premium formulations, price sensitivity in developing regions slows technology uptake. The preference for lower‑cost, conventional products persists in markets where environmental regulations are less stringent.

MARKET OPPORTUNITIES

Emerging Applications in Additive Manufacturing Open New Frontiers

The rapid growth of metal 3D printing presents transformative opportunities for specialized release agent solutions. As the industrial 3D printing market expands at a CAGR exceeding 24%, innovative release formulations are being developed to address the unique challenges of powder bed fusion and binder jetting technologies. These next‑generation products minimize part adhesion while maintaining dimensional accuracy in complex geometries, attributes particularly valuable in aerospace and medical implant manufacturing.

Circular Economy Initiatives Drive Sustainable Innovation

Mounting emphasis on sustainable manufacturing has spurred development of closed‑loop release agent systems featuring 90%+ recyclability rates. Leading manufacturers are introducing bio‑based formulations derived from plant oils that degrade naturally without compromising performance. The market for eco‑friendly release agents grew 28% in 2023, outpacing conventional product growth by nearly 3:1, signaling strong industry commitment to green chemistry principles. Strategic partnerships between chemical suppliers and OEMs are accelerating the commercialization of these sustainable solutions.

MARKET CHALLENGES

Technical Limitations in High‑Temperature Applications Impede Adoption

While release agents perform well in standard casting operations, extreme temperature applications continue to challenge formulation scientists. Titanium and superalloy casting processes exceeding 3,000°F frequently experience breakdowns in conventional release chemistries, leading to surface defects and reduced tool life. The development of ceramic‑based formulations shows promise but faces commercialization hurdles due to high production costs and application complexities. These technical barriers limit penetration in critical aerospace and defense applications where failure risks remain unacceptable.

Other Challenges

Skills Gap in Application Techniques

Proper release agent application requires specialized knowledge that many operations lack. Incorrect spraying parameters account for approximately 15% of quality issues in metal casting, highlighting the need for workforce training programs.

Customer Resistance to Product Switching

Established manufacturers often hesitate to modify proven processes, with some automotive suppliers reporting 18‑24 month evaluation periods before adopting new release agent technologies due to validation requirements.

Segment Analysis:

By Type

Permanent Release Agents Dominate the Market Due to Long‑Lasting Performance in High‑Temperature Applications

The market is segmented based on type into:

-

Permanent release agents

-

Semi‑permanent release agents

-

Sacrificial release agents

-

Internal release agents

By Application

Automotive Segment Leads Owing to Extensive Use in Die‑Casting and Molding Operations

The market is segmented based on application into:

-

Automotive

-

Mechanical industry

-

Manufacturing

-

Foundry

-

Others

By Form

Liquid Form Holds Major Share Due to Easy Application and Uniform Coverage

The market is segmented based on form into:

-

Liquid

-

Spray

-

Powder

-

Paste

By End‑Use Industry

Metalworking Industry Accounts for Significant Demand Driven by Complex Manufacturing Processes

The market is segmented based on end‑use industry into:

-

Metalworking

-

Rubber

-

Plastics

-

Composite materials

-

Others

Key Industry Players

Strategic Innovations and Expansions Define Market Leadership

🔟 1. Chem‑Trend

Headquarters: Irving, Texas, USA

Key Offering: Permanent and semi‑permanent release agents for die‑casting and rubber molding

Chem‑Trend, a subsidiary of Freudenberg Chemical Specialities, leverages decades of expertise in high‑performance release agents. The company focuses on silicone‑based formulations that provide exceptional thermal stability and long‑lasting performance, making it a preferred partner for automotive OEMs and large foundries.

Sustainability Initiatives:

- Development of low‑VOC, water‑based release agents

- Investment in circular economy programs to recycle spent coatings

- Partnerships with automotive manufacturers to test bio‑based alternatives

9️⃣ 2. Henkel AG & Co. KGaA

Headquarters: Düsseldorf, Germany

Key Offering: Permanent release agents and advanced surface treatments for automotive and aerospace

Henkel’s extensive portfolio spans both permanent and semi‑permanent agents, backed by a strong R&D pipeline. The company’s strategic acquisitions in Asia‑Pacific enhance its reach in emerging markets while maintaining a focus on high‑performance, low‑VOC solutions.

Sustainability Initiatives:

- Expansion of bio‑based formulation line to exceed 90% renewable content

- Implementation of green manufacturing practices across production facilities

- Collaboration with OEMs on sustainability targets for automotive components

8️⃣ 3. Dow Inc.

Headquarters: Midland, Michigan, USA

Key Offering: Advanced silicone‑based release agents for high‑temperature applications

Dow’s portfolio emphasizes durability and environmental compliance, offering solutions that meet stringent VOC regulations while maintaining performance at temperatures above 1,800°F.

Sustainability Initiatives:

- Research into water‑based and biodegradable formulations

- Investment in emissions reduction technologies for manufacturing plants

- Partnerships with automotive OEMs to reduce carbon footprint of casting processes

7️⃣ 4. DAIKIN Chemical Europe GmbH

Headquarters: Hamburg, Germany

Key Offering: Semi‑permanent release agents for die‑casting and injection molding

DAIKIN focuses on high‑performance, low‑VOC agents that support automation in manufacturing lines, offering precise dosage control and extended tool life.

Sustainability Initiatives:

- Development of water‑based release agents with low environmental impact

- Implementation of Industry 4.0 solutions for application monitoring

- Collaboration with European automotive suppliers on green chemistry projects

6️⃣ 5. Condat Corporation

Headquarters: Paris, France

Key Offering: Eco‑friendly release agents for metalworking and foundry applications

Condat’s portfolio emphasizes sustainable solutions, offering bio‑based coatings that meet high‑temperature performance requirements while reducing VOC emissions.

Sustainability Initiatives:

- Partnerships with European OEMs to develop green release agents

- Investment in recycling programs for spent coatings

- Research into plant‑oil‑derived formulations

5️⃣ 6. Siltech Corporation

Headquarters: Toronto, Canada

Key Offering: Liquid release agents for die‑casting and forging

Siltech delivers high‑quality, low‑VOC formulations tailored for the North American market, focusing on reliability and environmental compliance.

Sustainability Initiatives:

- Development of water‑based release agents

- Reduction of solvent usage in production lines

- Collaboration with Canadian automotive manufacturers on sustainability goals

4️⃣ 7. W.N. Shaw LLC

Headquarters: Houston, Texas, USA

Key Offering: High‑performance release agents for die‑casting and injection molding

W.N. Shaw specializes in custom formulations that cater to specific alloy requirements, supporting advanced manufacturing processes in automotive and aerospace sectors.

Sustainability Initiatives:

- Investment in low‑VOC and biodegradable formulations

- Implementation of energy‑efficient manufacturing practices

- Partnerships with OEMs to reduce overall emissions

3️⃣ 8. Miller‑Stephenson Chemical Company, Inc.

Headquarters: Phoenix, Arizona, USA

Key Offering: Permanent and semi‑permanent release agents for die‑casting and forging

Miller‑Stephenson focuses on reliability and durability, offering solutions that extend tool life and reduce maintenance costs in high‑volume production lines.

Sustainability Initiatives:

- Development of water‑based release agents

- Reduction of VOC emissions through process optimization

- Collaboration with automotive OEMs on green manufacturing initiatives

2️⃣ 9. AXEL Plastics Research Laboratories

Headquarters: Irvine, California, USA

Key Offering: Advanced silicone‑based release agents for die‑casting and injection molding

AXEL provides high‑performance formulations that meet stringent environmental regulations while delivering exceptional thermal stability.

Sustainability Initiatives:

- Investment in low‑VOC and water‑based formulations

- Development of eco‑friendly product lines for the automotive sector

- Collaboration with automotive OEMs on sustainability targets

1️⃣ 10. Marbocote Limited

Headquarters: London, United Kingdom

Key Offering: Permanent release agents for die‑casting and forging

Marbocote’s portfolio focuses on long‑lasting performance and high‑temperature stability, supporting automotive and aerospace manufacturers worldwide.

Sustainability Initiatives:

- Development of low‑VOC release agents

- Implementation of green manufacturing practices

- Partnerships with European OEMs on sustainability goals

Download FREE Sample Report: Metal Release Agent Market – View in Detailed Research Report

Get Full Report: Metal Release Agent Market – View in Detailed Research Report

Outlook: The Future of Metal Release Agent Market

The metal release agent market is poised for steady growth, driven by the automotive industry’s shift toward lightweight aluminum components and the increasing adoption of automation in manufacturing. Technological advancements in silicone‑based and water‑based formulations, coupled with Industry 4.0 integration, are expected to further enhance performance while reducing environmental impact.

Key Trends Shaping the Market

- Expansion of electric vehicle production driving demand for high‑performance, low‑VOC release agents

- Growth of metal 3D printing requiring specialized release formulations

- Accelerated adoption of Industry 4.0 technologies for precise dosage control and predictive maintenance

- Increasing focus on circular economy initiatives and bio‑based formulations

Future Trends

Emerging trends include the development of nano‑engineered release agents for superior surface finish, the integration of AI‑driven application systems, and the rise of eco‑friendly, plant‑oil‑derived coatings. Market participants will need to invest in R&D to stay ahead of regulatory changes and meet the evolving demands of automotive OEMs and foundry operators.

- Top 10 Companies in the Southeast Asia Alpha1-Proteinase Inhibitor Market (2026): Market Leaders Powering Regional Growth - July 10, 2026

- Top 10 Companies in the Nano Oxide Polishing Powder Market (2026): Market Leaders Driving Precision Manufacturing - July 10, 2026

- Top 10 Companies in the Propylene Glycol Market (2026): Market Leaders Driving Global Chemical Trends - July 10, 2026