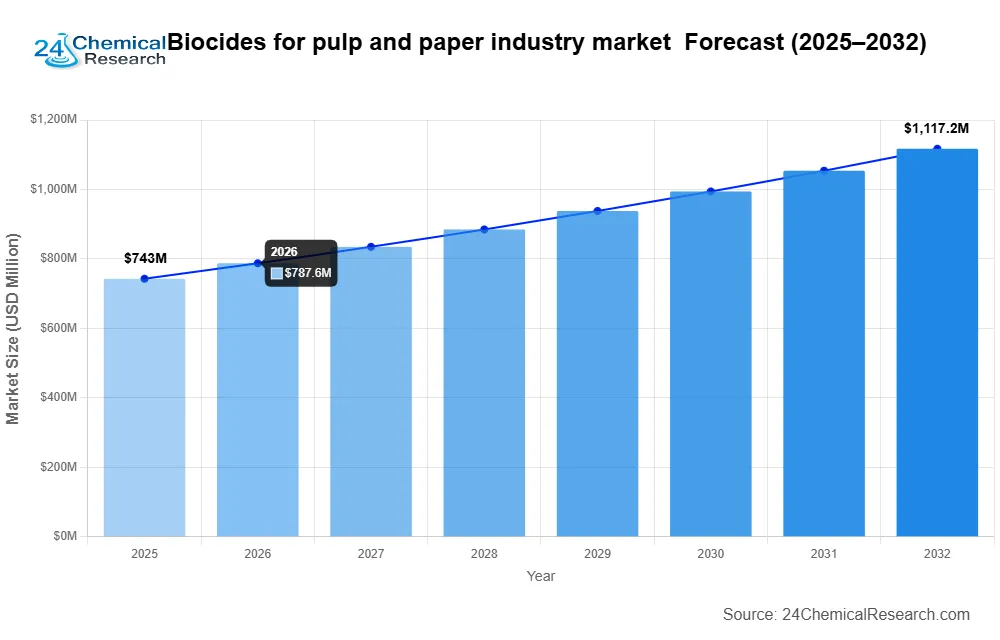

The Biocides for Pulp and Paper Industry Market was valued at USD 743 million in 2024 and is projected to reach USD 1.12 billion by 2032, growing at a 6.0% CAGR during the forecast period (2025–2034). This growth is driven by increasing paper production in emerging economies, stricter hygiene regulations in food packaging, and a shift toward sustainable biocide solutions.

As the pulp and paper industry evolves toward greener production and tighter microbial control, the spotlight is on the key biocide suppliers who are driving innovation, efficiency, and sustainability. In this blog, we profile the Top 10 Companies in the Biocides for Pulp and Paper Industry Market—a mix of global leaders, specialty manufacturers, and emerging players shaping the future of industrial antimicrobial solutions.

Biocides for Pulp and Paper Industry Market – View in Detailed Research Report

MARKET INSIGHTS

Global biocides for pulp and paper industry market size was valued at USD 743 million in 2024 and is projected to reach USD 1.12 billion by 2032, growing at a CAGR of 6.0% during the forecast period.

Biocides are chemical formulations crucial for microbial control in pulp and paper manufacturing processes. These specialized products prevent bacterial and fungal growth that can cause slime formation, equipment corrosion, and product quality issues. Key product categories include oxidizing biocides (chlorine dioxide, hydrogen peroxide), non-oxidizing biocides (isothiazolinones, DBNPA), and organic acids, each serving distinct antimicrobial functions across production stages.

Market growth is primarily driven by increasing paper production in emerging economies, where output rose 3.5% annually since 2020, coupled with stricter hygiene regulations in food packaging applications. However, environmental concerns regarding biocide residues pose challenges, prompting manufacturers like BASF and Nouryon to develop eco-friendly alternatives. Recent developments include Kemira’s 2023 launch of a next-generation halogen-free biocide system, demonstrating the industry’s shift toward sustainable solutions without compromising antimicrobial efficacy.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Sustainable Paper Products to Accelerate Biocide Adoption

Global shift toward sustainable paper production is driving significant growth in the biocides market, with the pulp and paper industry increasingly adopting microbial control solutions to meet environmental standards. As consumers and regulators demand eco-friendly paper products, manufacturers are investing in advanced biocide formulations that minimize environmental impact while effectively controlling microbial growth. The market for sustainable packaging is projected to grow at over 7% annually through 2030, creating substantial demand for compatible biocides. These specialized formulations help mills maintain production efficiency while reducing their carbon footprint through optimized chemical usage.

Expansion of Packaging Industry to Fuel Market Growth

The exponential growth of e-commerce and packaged goods is creating robust demand for paper-based packaging, subsequently driving biocide consumption. With the global packaging market expected to exceed $1.2 trillion by 2028, paper mills are expanding production capacities to meet this demand. Biocides play a critical role in maintaining paper quality throughout the supply chain, preventing microbial degradation that could compromise packaging integrity. The food packaging segment alone accounts for approximately 35% of biocide consumption in the paper industry, as strict hygiene standards require effective microbial control during production and storage.

Furthermore, emerging technologies in biocide formulations are enabling longer‑lasting protection with reduced environmental impact. Recent developments include: multi‑action biocides that target diverse microbial species while maintaining compliance with stringent environmental regulations in major markets. Manufacturers are increasingly focusing on region‑specific formulations to address varying regulatory requirements across North America, Europe, and Asia‑Pacific markets.

MARKET CHALLENGES

Stringent Environmental Regulations Present Compliance Challenges

The biocides market faces increasing pressure from evolving environmental regulations, particularly in Europe and North America. Regulatory frameworks such as the EU Biocidal Products Regulation (BPR) and EPA guidelines in the United States impose strict limitations on chemical usage, requiring extensive testing and documentation for product approvals. Compliance costs for new biocide formulations can exceed $1 million, creating significant barriers for market entry and product development. Furthermore, certain traditional biocidal compounds are being phased out due to environmental concerns, forcing manufacturers to invest heavily in alternative formulations.

Other Challenges

Microbial Resistance Development

Repeated use of similar biocidal compounds has led to increasing microbial resistance in paper mills, requiring higher treatment doses or more expensive combination products. Industry surveys indicate over 25% of mills report reduced efficacy of traditional biocides due to resistance development.

Raw Material Price Volatility

Fluctuations in key chemical feedstock prices continue to impact manufacturing costs, with some active ingredients experiencing 15-20% annual price variations. This volatility makes long‑term cost planning difficult for both suppliers and end‑users.

MARKET RESTRAINTS

High Switching Costs and Long Approval Processes Limit Market Expansion

The biocides market faces significant constraints due to the substantial investments required for product switching and lengthy regulatory approval timelines. Paper mills typically conduct extensive trials before adopting new biocidal products, with evaluation periods often lasting 6-12 months. This cautious approach, combined with the capital‑intensive nature of pulp and paper operations, creates inertia that limits the adoption of innovative solutions. Additionally, the development cycle for new biocidal formulations can extend 3-5 years from concept to commercial availability due to rigorous testing requirements.

Moreover, the industry’s conservative approach to operational changes means established products maintain dominant market positions even when more advanced alternatives become available. This phenomenon is particularly pronounced in mature markets where mills prioritize production stability over potential efficiency gains from new biocide technologies.

MARKET OPPORTUNITIES

Development of Bio‑based and Smart Biocides to Open New Market Segments

Emerging bio‑based biocides and smart delivery systems represent significant growth opportunities, particularly in environmentally sensitive markets. Plant‑derived antimicrobial compounds are gaining traction, with some formulations demonstrating comparable efficacy to traditional chemicals while offering improved biodegradability. The market for green biocides is projected to grow at nearly 9% CAGR through 2030 as sustainability becomes a key purchasing criterion. Smart biocides with time‑release mechanisms and condition‑activated properties are also showing promise for optimizing chemical usage and reducing environmental discharge.

Additionally, digital monitoring systems for microbial control are creating complementary opportunities: advanced sensor technologies now enable real‑time monitoring of microbial activity, allowing for precision dosing of biocides that can reduce chemical usage by up to 30% while maintaining effective protection. Partnerships between chemical manufacturers and technology providers are expected to accelerate the development of these integrated solutions, creating new value propositions for paper producers facing increasing cost and sustainability pressures.

Segment Analysis:

By Type

Organic Biocides Dominate the Market Due to Their Broad‑Spectrum Microbial Control and Environmental Compliance

The market is segmented based on type into:

-

Inorganic Biocides

-

Organic Biocides

By Application

Paper Mills Segment Holds the Largest Share Due to High Demand for Microbial Control in Production Processes

The market is segmented based on application into:

-

Packaging Materials

-

Paper Mill

-

Other

By Function

Slimicides Segment Leads Due to Their Extensive Use in Controlling Microbiological Growth

The market is segmented based on function into:

-

Slimicides

-

Microbicides

-

Others

By Form

Liquid Formulations Prevail Due to Ease of Application in Pulp and Paper Processes

The market is segmented based on form into:

-

Liquid

-

Powder

-

Others

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Companies Drive Market Growth Through Innovation and Strategic Expansion

Global biocides for pulp and paper industry market is characterized by a moderately consolidated competitive landscape, with established players dominating revenue shares while regional competitors maintain strong footholds in specific geographies. Kemira Oyj and BASF SE collectively held over 25% of the market share in 2023, leveraging their extensive product portfolios and global distribution networks.

Lanxess has emerged as another key player, particularly in the European market, where stringent environmental regulations have driven demand for high‑performance, eco‑friendly biocides. The company’s recent acquisition of Emerald Kalama Chemical significantly strengthened its position in specialty antimicrobial solutions for paper production.

Meanwhile, Nouryon and Buckman are focusing on R&D investments, developing next‑generation biocidal formulations that address both efficacy requirements and sustainability concerns. Buckman’s Optimyze® technology platform, for instance, has gained traction as an innovative solution for slime control in paper mills.

The competitive intensity is further heightened by medium‑sized players like Siddharth Chemicals and Vink Chemicals, which compete aggressively on price while expanding their presence in emerging Asian markets. Recent industry shifts show larger players responding through strategic partnerships and localized production facilities to maintain their competitive edge.

List of Prominent Biocide Manufacturers in Pulp & Paper Industry

-

Kemira Oyj (Finland)

-

BASF SE (Germany)

-

Lanxess AG (Germany)

-

Nouryon (Netherlands)

-

Ecolab Inc. (U.S.)

-

Buckman Laboratories (U.S.)

-

DuPont de Nemours, Inc. (U.S.)

-

Siddharth Chemicals (India)

-

Vink Chemicals (Germany)

-

Aries Chemical (U.S.)

MARKET TRENDS

Stringent Environmental Regulations to Drive Demand for Sustainable Biocides

Global biocides market for the pulp and paper industry is witnessing a significant shift toward environmentally friendly solutions due to tightening regulations on chemical usage in industrial applications. Regulatory bodies in regions such as North America and Europe have implemented stricter guidelines for biocidal product approvals, pushing manufacturers to develop low‑toxicity and biodegradable formulations. For instance, the European Union’s Biocidal Products Regulation (BPR) mandates rigorous safety assessments for antimicrobial chemicals, accelerating innovation in bio‑based alternatives. This trend is further supported by consumer demand for sustainable paper products, with over 60% of manufacturers now prioritizing eco‑certified biocides to maintain compliance while ensuring microbial control in production processes.

Other Trends

Expansion in Emerging Markets

Rapid industrialization in Asia‑Pacific and Latin America is fueling demand for pulp and paper products, subsequently boosting biocide adoption. Countries like China and India are investing heavily in packaging and tissue paper manufacturing, with the regional market projected to grow at a CAGR of 7.2% through 2032—outpacing the global average. Local mills increasingly rely on cost‑effective biocidal treatments to maintain operational efficiency, particularly in humid climates where microbial growth poses persistent challenges. However, inconsistent regulatory frameworks in these regions create variability in product acceptance, presenting both opportunities and hurdles for suppliers.

Technological Advancements in Formulation Chemistry

Innovations in synergistic biocide blends are transforming microbial management strategies within pulp mills. Recent developments include time‑release chemistries that prolong antimicrobial activity while reducing dosage frequencies by up to 40%, significantly lowering operational costs. Furthermore, the integration of smart monitoring systems with IoT‑enabled sensors allows real‑time detection of microbial contamination, enabling precise biocide dosing. Leading suppliers are also investing in halogen‑free compositions to minimize equipment corrosion—critical given that microbial‑induced corrosion accounts for approximately 25% of maintenance costs in paper production facilities.

Regional Analysis: Biocides for Pulp and Paper Industry Market

North America

The North American biocides market for the pulp and paper industry is driven by stringent environmental regulations, particularly U.S. EPA guidelines on wastewater treatment and chemical usage in manufacturing processes. The region emphasizes sustainable biocidal solutions with low environmental impact, such as halogen‑based and oxidizing biocides. Major paper‑producing countries like the U.S. and Canada are investing in microbial control technologies to improve operational efficiency and comply with regulatory standards. Despite market maturity, growth persists due to the expansion of specialty paper segments and recycled paper production, which require advanced biocidal treatments. Key players like Ecolab and Buckman maintain strong positions through tailored solutions for slime and microbial control.

Europe

Europe’s market is characterized by strict regulatory oversight under EU BPR (Biocidal Products Regulation) and REACH, which mandate rigorous testing and approval processes for biocidal products. The shift toward eco‑friendly alternatives, such as non‑oxidizing biocides and bio‑based formulations, is accelerating, particularly in countries like Germany and Sweden, where sustainability is a priority. However, high compliance costs and longer approval timelines pose challenges for manufacturers. The region’s focus on recycled paper production further drives biocide demand, as reclaimed fibers are more susceptible to microbial contamination. Companies like Kemira and BASF lead innovation in water treatment biocides to address these needs.

Asia‑Pacific

As the fastest‑growing regional market, Asia‑Pacific accounts for over 40% of global consumption due to rapid expansion of paper mills in China, India, and Indonesia. Cost‑effective inorganic biocides (e.g., chlorine dioxide) dominate here, though stricter environmental policies are gradually encouraging a shift toward organic alternatives. China’s ‘Two Mountains’ policy, emphasizing ecological protection, exemplifies this trend. India’s packaging sector growth also fuels demand, albeit with price sensitivity favoring local suppliers like Siddharth Chemicals. Challenges include fragmented regulations and inconsistent enforcement, but long‑term potential remains robust with increasing pulp production capacity.

South America

The market in South America is emerging, supported by Brazil’s thriving pulp exports and Argentina’s growing packaging industry. While conventional biocides are prevalent due to lower costs, multinational players like Nouryon are introducing advanced formulations for large‑scale mills. Economic instability and currency fluctuations, however, restrain investments in high‑end products. Regulatory frameworks are less stringent compared to North America or Europe, though Brazil’s CONAMA resolutions are gradually tightening wastewater discharge norms, creating incremental opportunities for compliant biocide suppliers.

Middle East & Africa

This region shows nascent but promising growth, with Turkey and South Africa leading biocide adoption in paper mills. Limited local production capacity creates reliance on imports, while water scarcity issues emphasize the need for efficient microbial control in recycling processes. The UAE’s focus on sustainable industrial growth under initiatives like ‘Operation 300bn’ could drive future demand. However, market penetration remains low due to underdeveloped pulp industries and a preference for cost‑effective solutions over advanced technologies.

Report Scope

This report presents a comprehensive analysis of the global and regional markets for Biocides for Pulp and Paper Industry, covering the period from 2024 to 2032. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

-

Sales, sales volume, and revenue forecasts

-

Detailed segmentation by type and application

In addition, the report offers in‑depth profiles of key industry players, including:

-

Company profiles

-

Product specifications

-

Production capacity and sales

-

Revenue, pricing, gross margins

-

Sales performance

It further examines the competitive landscape, highlighting the major vendors and identifying the critical factors expected to challenge market growth.

As part of this research, we surveyed Biocides for Pulp and Paper Industry companies and industry experts. The survey covered various aspects, including:

-

Revenue and demand trends

-

Product types and recent developments

-

Strategic plans and market drivers

-

Industry challenges, obstacles, and potential risks

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Biocides for Pulp and Paper Industry?

-> Global biocides for pulp and paper industry market was valued at USD 743 million in 2024 and is projected to reach USD 1.12 billion by 2032, growing at a CAGR of 6.0% during the forecast period.

Which key companies operate in Global Biocides for Pulp and Paper Industry?

-> Key players include Kemira, BASF, Dupont, Lanxess, Nouryon, Ecolab, and Buckman, among others.

What are the key growth drivers?

-> Key growth drivers include increasing paper production, stringent hygiene regulations, and rising demand for sustainable biocides.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include eco‑friendly biocides, advanced microbial control solutions, and regulatory compliance innovations.

🔟 1. Kemira Oyj

Headquarters: Finland

Key Offering: Halogen‑free biocide systems, liquid and powder formulations for pulp and paper mills

Kemira has pioneered next‑generation halogen‑free biocide solutions that deliver robust microbial control while minimizing environmental impact. Their portfolio includes high‑efficiency oxidizing and non‑oxidizing agents tailored for pulp, paper, and wastewater treatment applications.

Sustainability Initiatives:

- Development of bio‑based biocides with low toxicity and high biodegradability

- Investment in closed‑loop water treatment systems for paper mills

- Collaboration with research institutions to optimize formulation performance

9️⃣ 2. BASF SE

Headquarters: Germany

Key Offering: Oxidizing biocides, non‑oxidizing agents, and advanced antimicrobial blends for pulp and paper

BASF’s extensive product portfolio supports microbial control across all stages of pulp and paper production. Their focus on high‑performance, low‑toxicity formulations aligns with tightening regulatory requirements and sustainability goals.

Sustainability Initiatives:

- Development of low‑toxicity biocides for water‑sensitive processes

- Integration of digital monitoring for precision dosing

- Commitment to reduce carbon footprint across manufacturing

8️⃣ 3. Lanxess AG

Headquarters: Germany

Key Offering: Specialty antimicrobial solutions, including isothiazolinone‑based biocides for paper and packaging

Lanxess’s recent acquisition of Emerald Kalama Chemical has strengthened its position in eco‑friendly biocides, offering high‑performance solutions for the pulp and paper industry.

Sustainability Initiatives:

- Expansion of non‑oxidizing biocide portfolio

- Partnerships with local mills to customize formulations

- Focus on regulatory compliance and eco‑certification

7️⃣ 4. Nouryon

Headquarters: Netherlands

Key Offering: Advanced biocidal formulations, including DBNPA and organic acid blends for pulp and paper

Nouryon invests heavily in R&D to develop next‑generation biocides that balance efficacy with environmental performance.

Sustainability Initiatives:

- Development of bio‑based alternatives for conventional chemicals

- Optimization of production processes for lower energy consumption

- Collaboration with industry partners on sustainability metrics

6️⃣ 5. Ecolab Inc.

Headquarters: United States

Key Offering: Comprehensive microbial control solutions for pulp and paper, including liquid and powder biocides

Ecolab’s solutions focus on reducing microbial contamination in water systems and enhancing product quality in paper mills.

Sustainability Initiatives:

- Water‑efficiency programs for paper mills

- Low‑toxicity biocide development

- Digital platforms for real‑time monitoring of microbial loads

5️⃣ 6. Buckman Laboratories

Headquarters: United States

Key Offering: Slimicides and microbicides for pulp and paper, including the Optimyze® platform

Buckman’s Optimyze® technology provides precision dosing and advanced slimicide solutions that reduce chemical usage while maintaining microbial control.

Sustainability Initiatives:

- Smart delivery systems for time‑release biocides

- Integration of IoT sensors for process optimization

- Commitment to lower environmental impact of manufacturing

4️⃣ 7. DuPont de Nemours, Inc.

Headquarters: United States

Key Offering: Broad range of biocides for pulp, paper, and wastewater treatment

DuPont’s portfolio includes high‑efficiency oxidizing and non‑oxidizing agents that meet stringent regulatory standards.

Sustainability Initiatives:

- Development of biodegradable biocides

- Partnerships for circular economy solutions in paper production

- Focus on reducing chemical footprints in manufacturing

3️⃣ 8. Siddharth Chemicals

Headquarters: India

Key Offering: Cost‑effective inorganic biocides for pulp and paper mills

Siddharth Chemicals serves the rapidly expanding Indian market with affordable, high‑performance biocides.

Sustainability Initiatives:

- Local production to reduce transportation emissions

- Efficient manufacturing processes to lower energy use

- Compliance with emerging environmental regulations in India

2️⃣ 9. Vink Chemicals

Headquarters: Germany

Key Offering: Specialty biocides for pulp, paper, and packaging, including organic acid blends

Vink Chemicals focuses on high‑quality, eco‑friendly biocides tailored to European regulatory frameworks.

Sustainability Initiatives:

- Development of low‑toxicity formulations

- Collaboration with European mills on sustainability targets

- Investment in green manufacturing technologies

1️⃣ 10. Aries Chemical

Headquarters: United States

Key Offering: Advanced antimicrobial solutions for pulp and paper, including oxidizing and non‑oxidizing agents

Aries Chemical provides innovative biocides that meet the evolving needs of the pulp and paper industry.

Sustainability Initiatives:

- Research on bio‑based biocide alternatives

- Efficient production processes to reduce waste

- Commitment to regulatory compliance and environmental stewardship

Download FREE Sample Report: Biocides for Pulp and Paper Industry Market

Get Full Report: Biocides for Pulp and Paper Industry Market

🌍 Outlook: The Future of Biocides in the Pulp and Paper Industry

As global demand for sustainable paper products continues to rise, the biocides market is poised for steady growth. Key drivers include the expansion of e‑commerce, stringent hygiene regulations, and the shift toward eco‑friendly manufacturing processes. Innovations in smart delivery systems, digital monitoring, and bio‑based formulations will further accelerate adoption, especially in emerging markets where cost‑effective solutions are critical.

📈 Future Trends Shaping the Market

- Adoption of smart biocides with time‑release mechanisms to reduce chemical usage

- Integration of IoT sensors for real‑time microbial monitoring and precision dosing

- Expansion of bio‑based and green biocide portfolios to meet regulatory and consumer demands

- Collaboration between chemical manufacturers and technology providers to create integrated solutions

- Top 10 Companies in the PVDF for Lithium Battery Adhesives Market (2026): Market Leaders Powering Global Energy Storage - July 5, 2026

- Top 10 Companies in the Latin America Sericin Market (2026): Market Leaders Powering Global Sericin - July 5, 2026

- Top 10 Companies in the FEP-coated Polyimide Film Market (2026): Market Leaders Powering Global Innovation - July 5, 2026