MARKET INSIGHTS

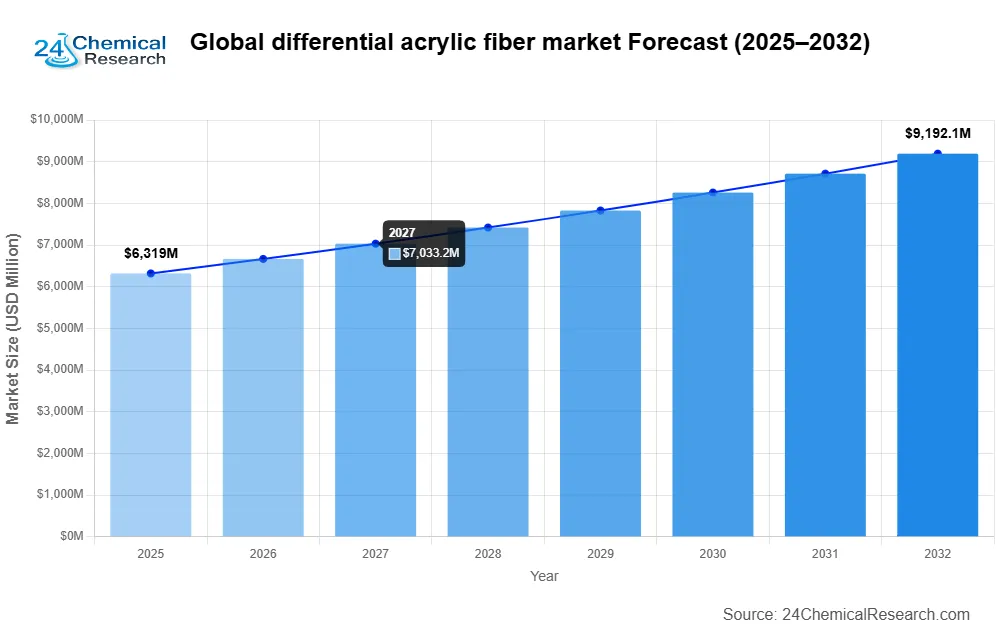

Global differential acrylic fiber market was valued at USD 6,319 million in 2024 and is projected to reach USD 8,899 million by 2032, growing at a CAGR of 5.5% during the forecast period.

Differential acrylic fiber is a specialized synthetic fiber engineered with modified chemical structures or enhanced processing techniques to achieve superior properties compared to conventional acrylic fibers. These fibers exhibit key characteristics including higher tensile strength, improved elasticity, reduced moisture absorption, and enhanced flame resistance. The product variants include flame retardant acrylic fiber, ultra‑high shrinkage acrylic fiber, and other specialty types.

The market growth is primarily driven by increasing demand from the textile industry, particularly for applications in clothing fabrics, industrial textiles, and home furnishings. The flame retardant segment is witnessing significant traction due to stringent safety regulations across various industries. While Asia‑Pacific dominates the market share, North America and Europe maintain strong positions due to advanced manufacturing capabilities and high‑performance textile requirements. Key players like Asahi Kasei, Toray, and Aditya Birla are investing in R&D to develop innovative fiber variants, further propelling market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Demand for Flame Retardant Textiles to Accelerate Market Growth

Global differential acrylic fiber market is experiencing significant growth driven by rising safety regulations and demand for flame retardant textiles across industrial and residential applications. Flame retardant acrylic fibers, which can withstand temperatures exceeding 600°C, are increasingly being adopted in protective clothing, automotive interiors, and home furnishings. The industrial textiles segment alone accounted for over 32% of the market share in 2024, with projections indicating this sector will grow at a CAGR of 6.2% through 2032. Recent advancements in polymer modification techniques have enabled manufacturers to enhance the thermal stability of acrylic fibers without compromising comfort or durability, making them ideal for safety‑critical applications.

Expansion of Technical Textile Sector to Fuel Product Adoption

Technical textiles incorporating differentiated acrylic fibers are gaining traction across multiple industries, with the global technical textiles market projected to exceed $260 billion by 2027. These specialized fibers offer superior dimensional stability, chemical resistance, and weatherability compared to conventional acrylic fibers, making them particularly valuable in filtration, medical, and construction applications. The Asia‑Pacific region has emerged as a key growth area, with China’s technical textile sector expanding at nearly 8% annually. Major manufacturers are investing heavily in R&D to develop acrylic fibers with customized properties such as enhanced moisture wicking for sportswear or improved antimicrobial characteristics for healthcare textiles.

Sustainability Initiatives Driving Innovation in Acrylic Fiber Production

Environmental concerns are prompting manufacturers to develop more sustainable production methods for differentiated acrylic fibers. The textile industry accounts for approximately 10% of global carbon emissions, creating strong incentives for eco‑friendly alternatives. Recent breakthroughs include the development of bio‑based acrylic precursors and closed‑loop recycling systems that can recover over 85% of solvent used in fiber production. Several leading brands have committed to sourcing at least 50% of their acrylic fibers from sustainable production processes by 2026, creating significant market opportunities for manufacturers investing in green technologies.

MARKET RESTRAINTS

Volatility in Raw Material Prices to Challenge Market Stability

The differential acrylic fiber market faces significant pressure from fluctuating prices of key raw materials including acrylonitrile, which constitutes approximately 85% of fiber composition. Acrylonitrile prices have shown volatility exceeding 30% year‑over‑year, driven by supply chain disruptions and shifting petrochemical feedstock costs. This instability creates pricing challenges throughout the value chain, particularly for small and medium manufacturers operating with thin margins. The situation is further complicated by geopolitical factors affecting acrylonitrile exports from major producing regions, forcing many fiber producers to maintain higher inventory levels as a buffer against supply shocks.

Competition from Alternative Synthetic Fibers to Limit Market Penetration

While differentiated acrylic fibers offer unique properties, they face intense competition from other synthetic fibers such as modified polyester and nylon. These alternatives have captured significant market share in applications where cost is prioritized over performance characteristics, with polyester prices currently 25-30% lower than premium acrylic fibers. Furthermore, continuous improvements in polyester fiber technology—particularly in flame retardancy and moisture management—are eroding some of acrylic’s traditional competitive advantages. Market analysis suggests polyester fibers gained nearly 3% market share in technical textile applications between 2022 and 2024, primarily at the expense of acrylic fibers.

MARKET OPPORTUNITIES

Emerging Applications in Smart Textiles to Create New Revenue Streams

The integration of differentiated acrylic fibers into smart textile systems presents substantial growth potential. Conductive acrylic fibers capable of withstanding multiple wash cycles are being developed for wearable electronics, with the global smart textiles market projected to reach $15 billion by 2028. Recent innovations include acrylic‑based fibers that can monitor vital signs or change properties in response to environmental stimuli. Leading sportswear brands have begun incorporating these advanced fibers into performance apparel, creating high‑value niche markets where acrylic fibers command premium pricing.

Geographic Expansion in Developing Markets to Drive Volume Growth

Rapid urbanization and rising disposable incomes in emerging economies are creating significant opportunities for market expansion. Countries in Southeast Asia and Africa are experiencing textile demand growth rates exceeding 7% annually, with particular strength in home furnishing and automotive applications. Localized production strategies are proving effective, with several major manufacturers establishing regional manufacturing hubs to better serve these growing markets. Industry forecasts suggest these developing regions could account for over 40% of global differential acrylic fiber demand by 2030, representing a massive opportunity for companies willing to invest in local partnerships and distribution networks.

MARKET CHALLENGES

Stringent Environmental Regulations to Increase Compliance Costs

The acrylic fiber industry faces mounting regulatory pressure regarding solvent emissions and wastewater treatment, particularly in developed markets. New environmental legislation in the European Union and North America requires manufacturers to invest in emissions control systems that can increase production costs by 12-15%. These regulations are prompting facility upgrades across the industry, with estimated capital expenditures exceeding $500 million globally through 2026. Small manufacturers without adequate financial resources may struggle to meet these requirements, potentially leading to market consolidation as larger players acquire compliant production assets.

Supply Chain Complexities to Impact Production Efficiency

The specialized nature of differentiated acrylic fiber production creates unique supply chain vulnerabilities. Many proprietary additives and modifiers required for specialized fibers come from single‑source suppliers, creating potential bottlenecks. Transportation disruptions have become more frequent, with ocean freight delays increasing average lead times by 18-22 days compared to pre‑pandemic levels. These challenges are particularly acute for just‑in‑time manufacturing operations, forcing many producers to reevaluate their inventory management strategies and supplier diversification policies.

MARKET TRENDS

Growth of Functional Textiles Driving Demand for Differential Acrylic Fibers

Global differential acrylic fiber market is experiencing robust growth, projected to expand from $6.3 billion in 2024 to $8.9 billion by 2032, at a compound annual growth rate of 5.5%. This upward trajectory is primarily fueled by increasing demand for high‑performance textiles across multiple industries. Unlike conventional acrylic fibers, differentiated variants offer enhanced properties such as flame resistance, ultra‑high shrinkage capabilities, and improved moisture management. The apparel sector accounts for approximately 42% of total consumption, while industrial applications are growing at 6.8% annually due to stricter safety regulations worldwide.

Other Key Market Trends

Flame Retardant Segment Dominance

Flame retardant acrylic fibers currently represent 38% of the specialty segment and are expected to maintain leadership through 2032. This growth is directly tied to construction boom in emerging markets and revised fire safety standards in commercial spaces. Particularly in Asia‑Pacific regions, governments are mandating flame‑resistant materials in public infrastructure projects, creating sustained demand. The segment’s CAGR of 6.2% outstrips conventional acrylic fibers by nearly 2 percentage points, reflecting the premium placed on safety‑enhanced textiles.

Material Innovation and Sustainability Pressures

Manufacturers face dual pressures to develop both high‑performance and eco‑friendly differentiated acrylic fibers. While traditional production methods remain prevalent, over 15 major producers have committed to bio‑based alternatives by 2026. This shift responds to EU textile circularity policies and growing brand commitments to sustainable sourcing. Notably, Toray and Aditya Birla have introduced polymer modification technologies that reduce water consumption by 30% during fiber production without compromising functional characteristics. However, scalability remains a challenge, with recycled‑content differential fibers currently commanding 28% price premiums over conventional equivalents.

Regional Production Shifts Impacting Market Dynamics

The geographic concentration of differential acrylic fiber production is undergoing significant transformation. While China currently supplies 46% of global output, Southeast Asian nations are rapidly expanding capacity to capitalize on trade diversification strategies. Vietnam and Indonesia have seen combined investments exceeding $700 million in acrylic fiber facilities since 2022, primarily targeting export markets. Concurrently, North American producers are focusing on high‑value specialty fibers for defense and medical applications, where profit margins are 40-50% higher than commodity‑grade fibers. This regional specialization is creating distinct pricing and supply chain dynamics across market segments.

COMPETITIVE LANDSCAPE

Key Industry Players

Specialty Fiber Manufacturers Expand Capacities to Meet Growing Demand

Global differential acrylic fiber market features moderately consolidated competition, with Asahi Kasei and Toray Industries emerging as dominant players due to their technological expertise and diversified product portfolios. These companies collectively held approximately 25-30% market share in 2024, according to industry analyses.

Aksa AkrilikTong‑Hwa maintains strong market presence through vertical integration strategies, controlling raw material supply chains while serving textile markets worldwide. Meanwhile, Aditya Birla Group leverages its extensive distribution networks across Asia‑Pacific and Europe, particularly in flame‑retardant fiber segments which are projected to grow at 6-7% CAGR through 2032.

The competitive intensity is increasing as mid‑size manufacturers like Japan Exlan and Indian Acrylics invest aggressively in product differentiation. Recent capacity expansions in Southeast Asian markets demonstrate strategic shifts toward cost‑competitive production bases while maintaining quality standards comparable to traditional manufacturing centers.

Strategic collaborations are reshaping the marketplace, with notable examples including Toray’s joint ventures with Chinese producers to strengthen positions in industrial textile applications. Environmental considerations are driving R&D investments, as evidenced by Taekwang Industrial’s development of eco‑friendly dyeing compatible fibers in 2023-2024.

List of Key Differential Acrylic Fiber Companies Profiled

-

Aksa AkrilikTong‑Hwa (Turkey)

-

Asahi Kasei (Japan)

-

KANEKA (Japan)

-

Aditya Birla (India)

-

Taekwang Industrial (South Korea)

-

Japan Exlan (Japan)

-

Indian Acrylics (India)

-

Vardhman (India)

-

Toray (Japan)

-

Toyobo (Japan)

-

Dupont (U.S.)

Segment Analysis:

By Type

Flame Retardant Acrylic Fiber Segment Leads Due to Rising Demand in Safety‑Critical Applications

The market is segmented based on type into:

-

Flame Retardant Acrylic Fiber

-

Ultra‑High Shrinkage Acrylic Fiber

-

High Tenacity Acrylic Fiber

-

Antibacterial Acrylic Fiber

-

Others

By Application

Clothing Fabrics Segment Dominates Due to Superior Comfort and Durability Characteristics

The market is segmented based on application into:

-

Clothing Fabrics

-

Industrial Textiles

-

Home Textiles

-

Technical Textiles

-

Others

By End User

Apparel Industry Segment Holds Largest Share Due to Fashion Trends and Performance Requirements

The market is segmented based on end user into:

-

Apparel Industry

-

Automotive Industry

-

Construction Industry

-

Healthcare Sector

-

Others

Regional Analysis: Differential Acrylic Fiber Market

North America

The North American differential acrylic fiber market is characterized by strong demand from industrial applications and shifting consumer preferences toward performance textiles. The U.S. dominates regional consumption, particularly for flame‑retardant variants used in protective clothing and technical textiles. Stringent safety regulations in industries like oil & gas and firefighting drive innovation in fiber modifications. While the market remains mature, there is notable growth in specialty applications such as aerospace composites and smart textiles. Competition remains intense, with key suppliers continuously expanding their product portfolios through R&D investments.

Europe

Europe maintains a technologically advanced market focused on sustainability and high‑value applications. Germany and Italy lead in consumption, particularly for ultra‑high shrinkage fibers used in premium knitwear and automotive textiles. EU REACH regulations have accelerated the development of eco‑friendly production methods, with manufacturers investing in closed‑loop recycling systems. The regional market faces pricing pressures from Asian imports but maintains competitive advantages through superior product performance and certifications. Recent capacity expansions by major players indicate confidence in long‑term demand from technical textile sectors.

Asia‑Pacific

As the largest and fastest‑growing market, Asia‑Pacific accounts for over 60% of global differential acrylic fiber consumption. China’s massive textile industry and infrastructure development projects fuel demand across multiple segments, particularly industrial textiles. India emerges as a significant growth hotspot due to expanding domestic manufacturing capabilities and rising technical textile adoption. While price competition remains fierce, manufacturers are gradually shifting toward higher‑value specialty fibers to improve margins. Regional players increasingly collaborate with global brands to upgrade technology and meet international quality standards.

South America

The South American market shows uneven growth patterns, with Brazil representing the most developed differential acrylic fiber sector. Economic instability has slowed investments, but niche opportunities exist in industrial applications and counterfeit‑resistant fiber solutions. Local production remains limited, creating import dependency for specialized grades. However, initiatives to strengthen textile manufacturing capabilities may stimulate regional demand. Challenges include currency volatility and competition from Asian suppliers, though trade agreements could improve market access for premium fiber products.

Middle East & Africa

This region presents evolving opportunities, particularly in technical textile applications for oilfield and construction sectors. Turkey has emerged as a regional manufacturing hub, benefiting from proximity to European and African markets. While overall market penetration remains low compared to other regions, infrastructure development projects drive demand for flame‑retardant and high‑performance fibers. The lack of local production capabilities creates import opportunities, though logistics costs and payment risks deter some suppliers. Long‑term prospects appear promising as industrialization progresses.

Report Scope

This report presents a comprehensive analysis of the global and regional markets for Differential Acrylic Fiber, covering the period from 2025 to 2034. It includes detailed insights into the current market status and outlook across various regions and countries, with specific focus on:

-

Sales, sales volume, and revenue forecasts

-

Detailed segmentation by type and application

In addition, the report offers in-depth profiles of key industry players, including:

-

Company profiles

-

Product specifications

-

Production capacity and sales

-

Revenue, pricing, gross margins

-

Sales performance

It further examines the competitive landscape, highlighting the major vendors and identifying the critical factors expected to challenge market growth.

As part of this research, we surveyed Differential Acrylic Fiber companies and industry experts. The survey covered various aspects, including:

-

Revenue and demand trends

-

Product types and recent developments

-

Strategic plans and market drivers

-

Industry challenges, obstacles, and potential risks

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Differential Acrylic Fiber Market?

> Global Differential Acrylic Fiber market was valued at USD 6,319 million in 2024 and is projected to reach USD 8,899 million by 2032, growing at a CAGR of 5.5% during the forecast period.

Which key companies operate in Global Differential Acrylic Fiber Market?

> Key players include Aksa Akrilik, Asahi Kasei, KANEKA, Aditya Birla, Taekwang Industrial, Japan Exlan, Indian Acrylics, Vardhman, Toray, and Toyobo, among others. In 2024, the global top five players accounted for approximately 45% of the market revenue.

What are the key growth drivers?

> Key growth drivers include rising demand for specialty textiles, increasing adoption in industrial applications, and advancements in fiber technology. The flame retardant acrylic fiber segment is expected to witness significant growth due to stringent safety regulations.

Which region dominates the market?

> Asia‑Pacific dominates the market, accounting for over 50% of global consumption, driven by strong textile manufacturing in China and India. North America follows as the second‑largest market due to high demand for technical textiles.

What are the emerging trends?

> Emerging trends include development of eco‑friendly acrylic fibers, increasing R&D investments for high‑performance fibers, and growing adoption in automotive textiles. Manufacturers are focusing on sustainable production processes to meet environmental regulations.

Differential Acrylic Fiber Market – View in Detailed Research Report

Differential Acrylic Fiber Market – View in Detailed Research Report

🌍 Outlook: The Future of Differential Acrylic Fiber Market

Global differential acrylic fiber market is projected to grow from USD 6,319 million in 2024 to USD 8,899 million by 2032, driven by rising demand for high‑performance textiles and stringent safety regulations. The flame‑retardant segment, representing 38% of the specialty market, is expected to lead growth with a CAGR of 6.2% due to increased adoption in construction, automotive, and protective apparel. Sustainability initiatives and the shift toward bio‑based fibers are anticipated to further accelerate market expansion, especially in Asia‑Pacific and North America.

📈 Future Trends Shaping the Market

- Rapid adoption of smart textile technologies incorporating conductive differential acrylic fibers.

- Expansion of regional manufacturing hubs in Southeast Asia and Africa to meet local demand.

- Increased regulatory focus on solvent emissions and closed‑loop recycling systems.

- Growing collaboration between fiber manufacturers and apparel brands to develop high‑performance, eco‑friendly fabrics.

- Continued investment in R&D for flame‑retardant and ultra‑high shrinkage fibers to capture emerging market segments.

- Top 10 Companies in the Adhesive Anchors Market (2026): Market Leaders Powering Global Construction - July 3, 2026

- Top 10 Companies in the Molybdenum Disulfide (MoS?) Nanoflower as Lubricant Additive for Engine Oil Market (2026): Market Leaders Powering Global Innovation - July 3, 2026

- Top 10 Companies in the Latin America Automotive Metal Fasteners Market (2026): Market Leaders Powering Global Automotive - July 3, 2026