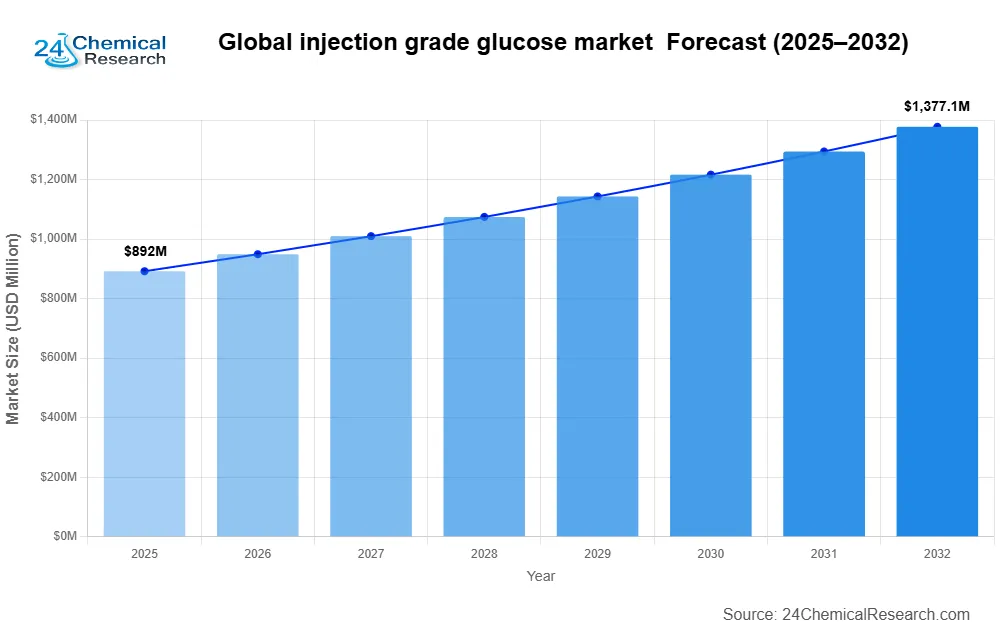

The Injection Grade Glucose Market reached a value of USD 892 million in 2024 and is on track to reach USD 1.38 billion by 2032, reflecting a CAGR of 6.4% over the forecast period. This trajectory underscores the sustained demand for sterile, high‑purity glucose solutions across a range of clinical settings.

Injection Grade Glucose Market – View in Detailed Research Report

Market Insights

Injection grade glucose, a pharmaceutical‑grade carbohydrate solution, is primarily administered intravenously. The sterile product adheres to rigorous pharmacopeial standards and serves as a vital energy source in hydration therapy, parenteral nutrition, and emergency hypoglycaemia treatment. It is available in two main forms—monohydrate and anhydrous—each with concentration ranges tailored to clinical needs.

Growth drivers include increasing hospital admissions, the rising prevalence of chronic diseases that necessitate fluid therapy, and expanding use in peritoneal dialysis solutions. The Asia‑Pacific region exhibits the fastest expansion thanks to improving healthcare infrastructure, while North America retains a dominant share of approximately 38% as of 2024. Leading players such as Cargill and CSPC Pharmaceutical Group are expanding capacity, particularly for the 5% and 10% dextrose solutions that account for over 65% of clinical usage.

Market Dynamics

Drivers

Demand for intravenous therapy continues to rise, with hospital and clinic usage of glucose injections growing for hydration, nutrition, and emergency care. The prevalence of chronic diseases requiring IV therapy has increased by about 18% over the past five years, reinforcing the need for pharmaceutical‑grade glucose solutions. Advances in medical protocols have solidified glucose injections as standard care for hypoglycaemia management and pre‑operative preparation.

Peritoneal dialysis procedures rely on high‑purity glucose solutions as osmotic agents, generating a reliable revenue stream. Global dialysis patient populations are projected to exceed 5 million by 2025, prompting expansion of treatment capacities and corresponding increases in glucose consumption. Quality improvements in dialysis solutions have further entrenched glucose as the preferred osmotic agent due to its safety profile and cost effectiveness.

Major drug manufacturers are dedicating 25–30% of R&D budgets to developing advanced parenteral nutrition products that incorporate injection grade glucose. The growing emphasis on clinical nutrition’s impact on patient outcomes has spurred formulary expansions across healthcare networks. Innovations in stabilization techniques have extended product shelf life while preserving potency, enabling broader distribution and market penetration.

Restraints

Stringent regulatory oversight imposes significant compliance costs. Facilities must adhere to current Good Manufacturing Practices (cGMP), requiring extensive documentation, testing protocols, and certifications. These requirements can elevate production costs by 15–20%, especially for smaller manufacturers. Regulatory audits and approval timelines often delay product launches, creating bottlenecks in supply chain responsiveness.

Price volatility in raw material supply chains, particularly corn and wheat starch, exhibits 12–18% quarterly fluctuations driven by agricultural market dynamics and geopolitical factors. This unpredictability compels manufacturers to maintain higher inventory buffers or engage in costly hedging strategies. Climate change impacts on crop yields further exacerbate supply uncertainties, with recent drought conditions reducing harvest outputs in key regions by approximately 7% annually.

Emerging synthetic plasma expanders and non‑glucose osmotic agents are gaining traction in specific medical applications. While glucose remains predominant in most protocols, some providers adopt novel solutions claiming improved patient outcomes or simplified administration. This diversification necessitates clinical studies to demonstrate comparative advantages and cost‑benefit ratios.

Opportunities

Developing nations are upgrading healthcare infrastructure, with 30–40% annual increases in hospital construction and medical equipment procurement. This expansion presents substantial opportunities for suppliers as facilities establish formularies and supply agreements. Local manufacturing partnerships can leverage cost advantages while meeting domestic production requirements increasingly mandated by governments for essential medical commodities.

Next‑generation hypertonic glucose solutions (20–50% concentrations) are gaining acceptance for specialized applications. These high‑value products command premium pricing while addressing unmet needs in emergency medicine and critical care. Investments in formulation technology can significantly enhance profit margins, with some specialty products achieving 35–45% gross margins compared to standard solutions.

Leading manufacturers are acquiring agricultural assets and starch processing facilities to secure upstream supply stability. This vertical integration strategy offers cost advantages and quality control benefits across the production cycle. Integrated producers achieve 12–15% greater operational efficiency compared to companies relying solely on third‑party suppliers.

Challenges

Maintaining aseptic processing conditions requires substantial capital expenditures. Cleanroom facilities and sterilization equipment account for 40–50% of initial plant investment costs, with ongoing validation and monitoring adding 8–10% to operating expenses. Contamination incidents can trigger costly recalls and regulatory sanctions, creating constant quality assurance pressures.

Injectable glucose solutions demand strict temperature control throughout the supply chain, with many formulations stable only within 2–8°C. This necessitates specialized cold‑chain infrastructure that adds 18–22% to distribution costs compared to ambient‑temperature pharmaceuticals. Reliable last‑mile delivery solutions for remote healthcare facilities remain an ongoing challenge.

Hospital purchasing consortia and government healthcare systems implement aggressive group purchasing strategies, reducing unit prices by 10–15% over the past three years. Manufacturers must balance these pricing pressures against rising input costs while maintaining profitability. Some producers respond by developing value‑added services, such as inventory management solutions, to differentiate their offerings beyond basic price competition.

Segment Analysis

By Type

Monohydrate Glucose Segment leads due to high stability and solubility in medical applications.

- Monohydrate Glucose

- Anhydrous Glucose

- Others

By Application

Pharmaceutical Injections Drive Market Growth With Increasing Demand for Emergency Care Solutions.

- Injections

- Peritoneal Dialysate

- Nutritional Formulations

- Others

By End‑User

Hospitals Dominate Consumption Patterns Due to High Volume IV Therapy Requirements.

- Hospitals

- Clinics

- Ambulatory Surgical Centers

- Home Healthcare

- Others

By Form

Liquid Formulation Preferred for Immediate Therapeutic Response in Critical Care.

- Liquid Solutions

- Powder

- Crystalline

Competitive Landscape

Key Industry Players

Global Injection Grade Glucose Market features a moderately competitive environment, with regional and multinational players vying for market share. Leading companies leverage product innovation, vertical integration, and strategic partnerships to strengthen their positions.

🔟 1. Cargill

Headquarters: United States

Key Offering: High‑purity monohydrate glucose solutions for intravenous therapy

Cargill’s extensive production facilities and stringent quality controls underpin its leadership in North America and Europe. The company’s recent investment in high‑purity variants has reinforced its market position, particularly for 5% and 10% dextrose solutions.

Sustainability & Growth Initiatives:

- Expansion of production capacity in North America

- Investment in advanced purification technologies

- Partnerships with hospitals to streamline supply chains

🔟 2. Shengtai Group

Headquarters: China

Key Offering: Cost‑competitive glucose solutions for domestic and regional markets

Shengtai Group’s strong foothold in the Asia‑Pacific region stems from localized manufacturing and distribution networks. The company’s focus on cost efficiency allows it to compete effectively against multinational entrants.

Sustainability & Growth Initiatives:

- Local sourcing of raw materials to reduce transportation emissions

- Implementation of energy‑efficient production processes

- Expansion of regional distribution centers

🔟 3. Qinhuangdao Lihua Starch

Headquarters: China

Key Offering: High‑purity anhydrous glucose for specialized applications

Qinhuangdao Lihua Starch focuses on capacity expansion to meet growing demand in emerging markets, particularly in China and India where chronic disease prevalence is rising.

Sustainability & Growth Initiatives:

- Investment in advanced starch processing facilities

- Partnerships with local pharmaceutical manufacturers

- Reduction of waste in production processes

🔟 4. Xiwang Sugar

Headquarters: China

Key Offering: Bulk glucose solutions for healthcare and pharmaceutical use

Xiwang Sugar leverages cost advantages to compete with multinational firms while expanding capacity to serve the growing demand for peritoneal dialysis solutions.

Sustainability & Growth Initiatives:

- Adoption of green manufacturing practices

- Collaboration with regional hospitals for supply chain optimization

- Continuous improvement of product purity standards

🔟 5. Kato Kagaku

Headquarters: Japan

Key Offering: Technologically refined glucose solutions compliant with international pharmacopeia standards

Kato Kagaku distinguishes itself through cutting‑edge refinement techniques, ensuring compliance with global standards and securing long‑term contracts with pharmaceutical giants.

Sustainability & Growth Initiatives:

- Investment in membrane filtration and chromatography technologies

- Real‑time quality monitoring systems

- Collaboration with global pharmaceutical partners

🔟 6. Global Sweeteners Holdings Limited

Headquarters: China

Key Offering: Specialty glucose formulations for niche medical applications

Through strategic acquisitions, Global Sweeteners expands its presence in specialty medical formulations, targeting high‑margin products.

Sustainability & Growth Initiatives:

- Acquisition of niche manufacturers

- Focus on high‑margin specialty products

- Expansion into emerging markets

🔟 7. Hunan Aiyuyue Biology

Headquarters: China

Key Offering: Innovative glucose solutions for biopharmaceutical applications

Hunan Aiyuyue Biology leverages R&D to develop glucose formulations tailored to biopharmaceutical needs, supporting vaccine and biologics production.

Sustainability & Growth Initiatives:

- Investment in biologics‑grade glucose production

- Partnerships with vaccine manufacturers

- Compliance with strict quality standards

🔟 8. CSPC Pharmaceutical Group

Headquarters: China

Key Offering: Broad portfolio of glucose solutions for clinical and pharmaceutical use

CSPC’s recent acquisition of a glucose syrup manufacturer secures its raw material supply chain, enhancing its capacity to meet market demand.

Sustainability & Growth Initiatives:

- Vertical integration of raw material sourcing

- Expansion of production facilities

- Strategic partnerships with regional hospitals

🔟 9. Yunnan Baiyao

Headquarters: China

Key Offering: Traditional Chinese medicine‑based glucose formulations for integrative therapy

Yunnan Baiyao extends its product line into glucose solutions, leveraging its expertise in herbal formulations to meet emerging integrative medicine trends.

Sustainability & Growth Initiatives:

- Integration of herbal and pharmaceutical production processes

- Focus on quality assurance and regulatory compliance

- Expansion into regional markets

🔟 10. Sinopec

Headquarters: China

Key Offering: Bulk glucose solutions for industrial and pharmaceutical applications

Sinopec’s diversified portfolio and extensive distribution network position it well to capture growing demand in both domestic and international markets.

Sustainability & Growth Initiatives:

- Investment in renewable energy for production facilities

- Partnerships with healthcare providers for supply chain optimization

- Focus on cost‑effective production processes

Download FREE Sample Report

Get Full Report

Outlook

The injection grade glucose market is poised to deepen its presence in both established and emerging regions. North America will continue to support a robust supply chain, while the Asia‑Pacific region’s rapid infrastructure development will drive further consumption. Companies that integrate upstream supply chains and invest in advanced purification technologies are likely to capture the highest margins.

Future Trends

- Increased adoption of hypertonic glucose solutions for critical care and emergency medicine.

- Expansion of vertical integration to secure raw material supply and reduce costs.

- Growth of specialty formulations as biopharmaceutical and vaccine production intensifies.

- Enhanced cold‑chain logistics solutions to support temperature‑sensitive products.

- Strategic collaborations between multinational and local manufacturers to enter emerging markets.

- Top 10 Companies in the Global Low Iron Quartz Sand for PV Glass Market (2026): Market Leaders Powering Solar Innovation - July 16, 2026

- Top 10 Companies in the Vinyl Acetate Monomer (VAM) Market (2026): Market Leaders Powering Global Growth - July 16, 2026

- Top 10 Companies in the Commercial Engineered Quartz Stone (EQS) Market (2026): Market Leaders Powering Global Commercial Spaces - July 16, 2026