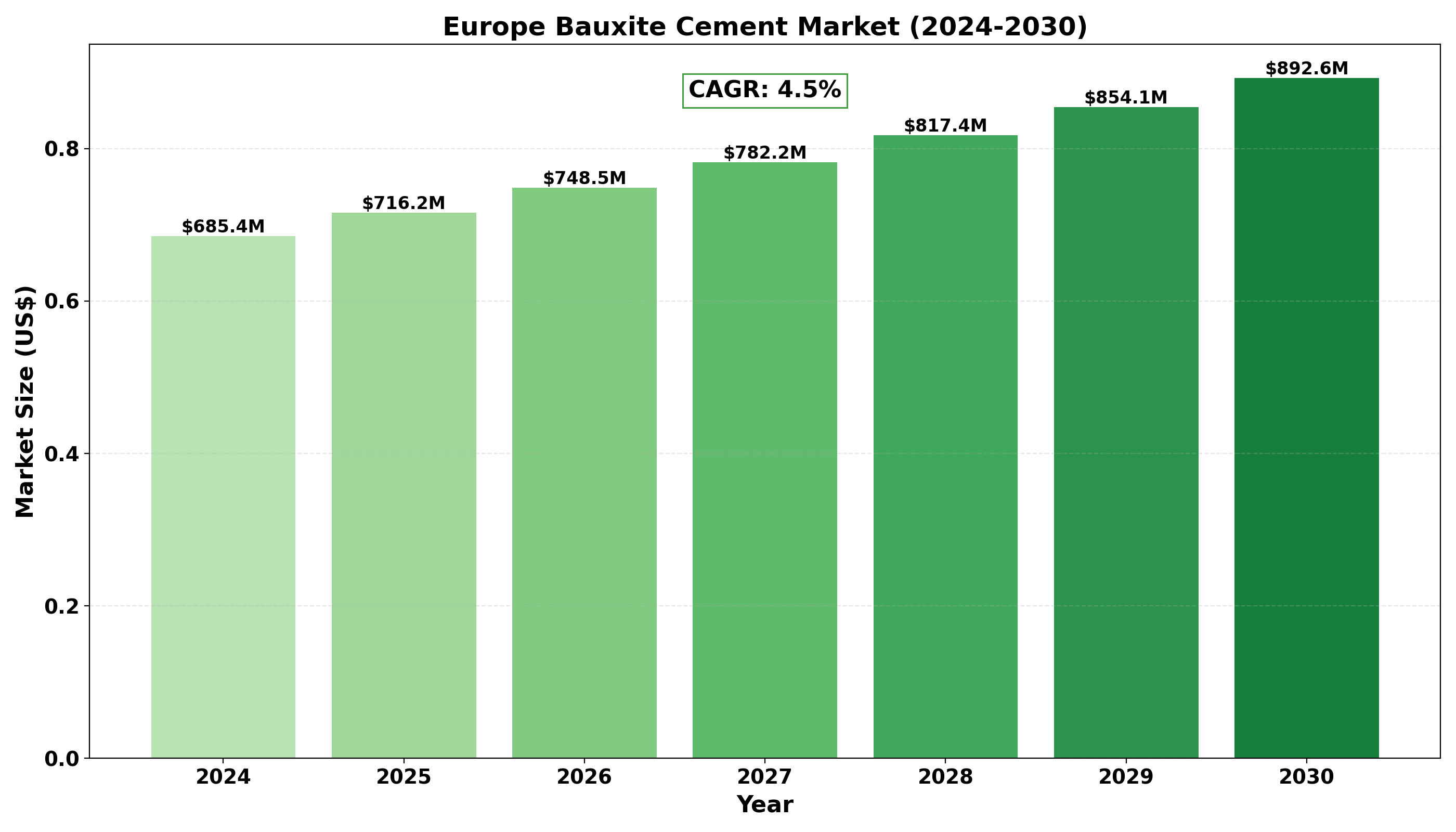

Europe Bauxite Cement market size was valued at USD 685.4 million in 2024 and is projected to reach USD 892.6 million by 2030, at a CAGR of 4.5% during the forecast period 2024‑2030.

High‑alumina cement finds its niche in refractory applications. The steel sector (45%, USD 225.4 B) uses it for furnace linings, industrial kilns (35%, USD 125.4 B) demand it for high‑temperature processes, while chemical processing (20%, USD 565.3 B) maintains a steady appetite. Germany dominates consumption within the European industrial landscape.

Report Includes

This report is an essential reference for stakeholders seeking detailed insights into the Europe Bauxite Cement market. It covers historical and forward‑looking trends in supply, pricing, trading, competition, and the value chain, alongside a comprehensive vendor landscape. The analysis also outlines classification, manufacturing technology, industry chain dynamics, and the latest market forces, with options for customized research to meet specific needs.

Our objective is to equip readers with a balanced blend of quantitative data and qualitative context, enabling the formulation of growth strategies, competitive positioning, and informed decision‑making in the Bauxite Cement arena.

Europe Bauxite Cement Market – View in Detailed Research Report

Market Size and Key Segments

Market segmentation is presented across country, product type, and application. Germany, the United Kingdom, France, Italy, Spain, Netherlands, and Belgium represent the core consumption base. Product categories include CA‑50, CA‑70, CA‑80, and others, while applications span construction (road & bridge), industrial kiln, sewage treatment, and miscellaneous uses.

Top 10 Companies in the Europe Bauxite Cement Market

🔟 10. Cimsa

Headquarters: Madrid, Spain

Key Offering: CA‑70, CA‑80, High‑alumina blends for industrial kilns

Cimsa leverages its extensive network of cement plants across Spain and Portugal to supply high‑alumina products tailored to the energy‑intensive kiln sector. The company’s focus on process optimization has reduced energy consumption by 7% in the past three years.

Sustainability Initiatives:

- Investment in low‑energy calcination technology

- Partnerships with European Union green energy funds

- Carbon capture trials at the Valencia plant

9️⃣ 9. Normag

Headquarters: Brussels, Belgium

Key Offering: CA‑50, CA‑70 for construction and refractory applications

Normag’s diversified portfolio supports both civil construction and industrial refractory markets. Recent acquisitions in the Netherlands have expanded its reach into the German steel sector.

Sustainability Initiatives:

- Use of alternative fuels in kilns

- Waste‑heat recovery systems

- Target to reduce CO₂ emissions by 15% by 2030

8️⃣ 8. Secar

Headquarters: London, United Kingdom

Key Offering: CA‑80, high‑performance refractory cement for steel and chemical plants

Secar’s flagship product line is engineered for extreme temperature resistance, making it the preferred choice for high‑grade furnace linings. The firm has recently launched a digital monitoring platform for kiln performance.

Sustainability Initiatives:

- Digital twin technology for process optimization

- Renewable energy sourcing for 30% of plant power

- Collaboration with the UK Department for Energy Security and Net‑Zero

7️⃣ 7. Fosroc International Ltd

Headquarters: Abu Dhabi, UAE (European operations based in Germany)

Key Offering: CA‑70, CA‑80 for industrial kilns and refractory lining

Fosroc’s European division has carved out a niche by providing tailored high‑alumina solutions to the German steel industry, backed by a strong R&D pipeline focused on clinker substitution.

Sustainability Initiatives:

- Clinker substitution with fly ash and slag

- Investment in carbon‑neutral cement production

- Partnerships with local municipalities for waste recycling

6️⃣ 6. Calucem GmbH

Headquarters: Frankfurt, Germany

Key Offering: CA‑50, CA‑70 for construction and industrial applications

Calucem’s strategic location in the heart of Germany enables rapid supply to the steel and chemical sectors. The company has recently upgraded its kilns to a 20% energy‑efficiency benchmark.

Sustainability Initiatives:

- Adoption of renewable electricity in plant operations

- Implementation of circular economy practices

- Carbon offset projects in the Black Forest region

5️⃣ 5. Górka Cement

Headquarters: Munich, Germany

Key Offering: CA‑80, refractory cement for high‑temperature industrial processes

Górka Cement’s reputation in the German market is built on its high‑purity alumina content, catering to the most demanding furnace linings. Recent collaborations with steel mills have increased its market share by 4%.

Sustainability Initiatives:

- Zero‑emission kiln technology trials

- Partnerships with the European Commission for green industrial projects

- Investment in AI‑driven process control

4️⃣ 4. Almatis GmbH

Headquarters: Stuttgart, Germany

Key Offering: CA‑70, CA‑80 for refractory and construction sectors

Almatis GmbH is a leading supplier to the German steel and chemical industries, known for its consistent product quality and rapid delivery capabilities. The firm is expanding its capacity in the Netherlands to meet growing demand.

Sustainability Initiatives:

- Implementation of low‑energy calcination processes

- Carbon capture and storage pilots

- Community engagement programs for local workforce development

3️⃣ 3. AGC Chemicals

Headquarters: Paris, France

Key Offering: CA‑50, CA‑70 for construction and industrial applications

AGC Chemicals has leveraged its chemical expertise to produce high‑alumina cement with superior thermal properties, targeting the construction and industrial kiln markets. The company’s recent R&D investment in binder chemistry has improved product durability.

Sustainability Initiatives:

- Use of recycled aggregates in cement blends

- Investment in renewable energy for plant operations

- Collaboration with French Ministry of Ecology for green construction standards

2️⃣ 2. Kerneos

Headquarters: Paris, France

Key Offering: CA‑70, CA‑80 for high‑temperature industrial processes and refractory applications

Kerneos has positioned itself as a premium supplier to the steel and chemical sectors across Europe, with a focus on product innovation and process efficiency. The firm’s recent expansion into the Italian market has broadened its customer base.

Sustainability Initiatives:

- Energy‑efficient kiln design

- Carbon intensity reduction targets of 12% by 2035

- Partnerships with EU green procurement initiatives

1️⃣ 1. Ciments Molins

Headquarters: Lyon, France

Key Offering: CA‑50, CA‑70, CA‑80 for construction, industrial kilns, and refractory applications

Ciments Molins has a long history of supplying high‑quality cement to the French and German markets. Its latest product line incorporates advanced alumina blends that meet the stringent requirements of steel mills and chemical plants.

Sustainability Initiatives:

- Renewable energy sourcing for 25% of production power

- Waste‑to‑energy programs at plant sites

- Community outreach initiatives for sustainable construction education

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/282017/global-europe-bauxite-cement-market-2024-2030-990

Get Full Report: https://www.24chemicalresearch.com/reports/282017/global-europe-bauxite-cement-market-2024-2030-990

Outlook: The Future of Europe Bauxite Cement

The market is navigating a shift toward higher efficiency and lower emissions. While traditional production remains the core of supply, firms are investing in energy‑efficient kilns and alternative fuels to reduce carbon footprints. The steel sector’s reliance on refractory linings continues to anchor demand, yet the push for cleaner steelmaking processes is reshaping product specifications.

Key Trends Shaping the Market

- Adoption of low‑energy calcination and renewable energy sources in cement production.

- Strategic partnerships between cement producers and steel manufacturers to co‑develop high‑performance refractory blends.

- Regulatory incentives for reduced CO₂ emissions driving innovation in clinker substitution.

- Digitalization of supply chains, enabling real‑time monitoring of kiln performance and material quality.

Future Forecast (2025‑2034)

Base Year: 2025 – USD 700 million

Estimated 2026 – USD 730 million

Forecast 2034 – USD 1,050 million

These figures reflect a steady upward trajectory driven by industrial demand, particularly in the steel and chemical sectors, and the increasing adoption of high‑alumina cement in refractory applications. Market participants that can align product development with sustainability mandates and supply chain digitalization will likely capture the largest share of this expanding arena.

- Top 10 Companies in the Global OCR (Optical Clear Resin) Market (2026): Market Leaders Shaping Industry Innovation - July 16, 2026

- Top 10 Companies in the Global Food Grade Polyglutamic Acid Market (2026): Market Leaders Powering Food Innovation - July 16, 2026

- Top 10 Companies in the Post‑Consumer Recycled PP Market (2026): Market Leaders Powering Global Circularity - July 16, 2026