MARKET INSIGHTS

Global Bulk AmorphoAlloy market size was valued at USD 96.06 million in 2025 and is projected to reach USD 482.76 million by 2034, exhibiting a CAGR of 19.65% during the forecast period.

Bulk AmorphoAlloys are metallic materials with a disordered atomic structure rather than the regular crystal arrangement found in traditional steel, aluminum, or titanium alloys. This unique atomic arrangement gives these materials unusual physical and mechanical behavior that is now attracting aerospace engineers, electronics manufacturers, biomedical researchers, defence companies, and energy infrastructure developers worldwide.

Bulk amorphous alloys are created by carefully regulated cooling techniques that avoid crystalline formation, in contrast to regular alloys that consolidate into crystal grains after cooling. The end product is a metallic substance that retains the toughness and conductivity of metal while acting more like glass at the atomic level.

Because these materials can provide very high tensile strength, outstanding wear resistance, and superior elastic limits when compared to traditional engineering metals, researchers from organisations like California Institute of Technology and Tohoku University have studied them in great detail.

Bulk AmorphoAlloy Global Market – View in Detailed Research Report

|

Bulk AmorphoAlloy Market Value (2025) |

USD 96.06 million |

|

Bulk AmorphoAlloy Market Value (2034) |

USD 482.76 million |

|

CAGR (%) |

19.65% |

Segment Analysis

|

Segment Category |

Sub-Segments |

Key Insights |

|

By Product Type |

|

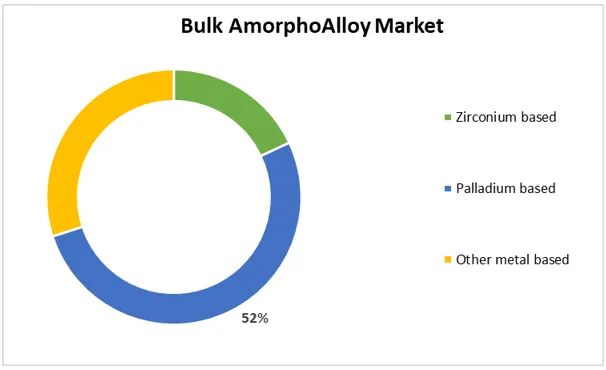

In comparison to palladium-based and other metal-based amorphous alloys, the zirconium-based segment currently leads the bulk amorphoalloy market due to its good balance of mechanical strength, corrosion resistance, glass-forming ability, and greater commercial feasibility. |

|

By Application |

|

Due to its widespread commercial usage, energy‑efficiency benefits, and expanding worldwide power infrastructure modernisation projects, the Transformer segment presently leads the Bulk AmorphoAlloy Market. Bulk amorphous alloys, especially iron‑based amorphous metals, are widely used in transformer cores because they significantly reduce core energy losses compared with conventional grain‑oriented silicon steel. |

By Product Type:

MARKET DRIVERS

Transition to Lightweight Materials in Transportation

While the automotive and aerospace industries are under immense pressure to reduce fuel consumption and emissions, the demand for materials that offer high performance without adding excessive weight has surged. Bulk Amorphous Alloys (BAAs) and metallic glasses present a compelling solution, offering specific strengths that rival some high‑grade steels while being significantly lighter. This transition is not merely a trend but a strategic necessity for manufacturers aiming to meet stringent global emission standards, particularly in electric vehicle (EV) segment growth where every gram of weight reduction directly impacts battery efficiency and range.

Superior Corrosion and Wear Resistance

Furthermore, the harsh operating environments encountered in both marine and chemical processing industries have highlighted the need for durable, corrosion‑resistant components. Unlike crystalline metals, BAA possess a uniform atomic structure that eliminates grain boundaries, the primary sites for corrosion initiation. This unique microstructural feature translates into exceptional resistance against acid, alkali, and seawater environments.

➤ The elimination of grain boundaries not only enhances corrosion resistance but also drastically extends the service life of critical mechanical parts under extreme stress.

Finally, the electronics sector is driving innovation through the shrinking of component sizes and the increase in operating frequencies. BAAs are finding applications in micro‑switches, sensors, and inductors where high magnetization saturation and low coercivity are paramount.

MARKET CHALLENGES

High Initial Production Costs

Despite the technical advantages, the commercial viability of Bulk Amorphous Alloys is frequently hindered by prohibitively high production costs. The manufacturing processes, such as copper mold casting or 3D printing, require precise temperature control and specialized equipment that are often beyond the financial reach of small‑to‑medium enterprises (SMEs).

Other Challenges

Temperature Sensitivity and Structural Integrity

One of the most significant hurdles is the thermal stability of these alloys. Bulk metallic glasses transition into a crystalline state at relatively low temperatures compared to traditional alloys, known as the glass transition temperature (Tg). Operating near or above this threshold risks crystallization, which can severely degrade the material’s mechanical properties.

Recycling Difficulties

The precise amorphous structure is difficult to maintain after multiple melting cycles, making recycling energy‑intensive and less attractive compared to conventional metals.

MARKET RESTRAINTS

Size Limitations and Casting Techniques

Scaling up to produce large, bulk forms remains a significant bottleneck. Internal stresses and uneven heat dissipation often lead to partial crystallization, rendering the component useless.

Rigorous Prototyping Requirements

Developing for BAA usually necessitates an iterative prototyping phase that is more complex and time‑consuming than working with standard alloys.

MARKET OPPORTUNITIES

Expansion in Renewable Energy Infrastructure

High‑efficiency components in wind turbines and solar energy systems create a fertile ground for BAA applications. Gearboxes, pumps, and generator rotors that operate under cyclic loads benefit from high fatigue strength and low Hertzian contact stress.

Biomedical Device Innovations

The natural biocompatibility of certain BAA compositions, combined with their specific strength, opens doors for advanced surgical tools, dental implants, and orthopedic devices.

Competitive Landscape

Key Industry Players

Strategic innovations and material capabilities drive the global market

The competitive landscape of the global Bulk AmorphoAlloy market is primarily defined by specialised metallurgical firms with deep expertise in glass‑forming technologies. Key players are predominantly concentrated in Japan and the United States, leveraging advanced manufacturing infrastructure to supply high‑performance metallic glasses.

List of Key Bulk AmorphoAlloy Manufacturers Profiled

- Toho Titanium Co., Ltd. (Japan)

- Hitachi Metals, Ltd. (Japan)

- Nanophase Technologies Corporation (USA)

- Umicore S.A. (Belgium)

- Carpenter Technology Corporation (USA)

- Alcoa Corporation (USA)

- General Electric (USA)

- Bosch Group (Germany)

- Samsung Advanced Institute of Technology (South Korea)

- Mitsubishi Materials Corporation (Japan)

Top 10 Companies in the Bulk AmorphoAlloy Global Market (2026)

🔟 10. Toho Titanium Co., Ltd.

Headquarters: Tokyo, Japan

Key Offering: Zirconium‑based amorphous alloys for transformer cores and aerospace components

Toho Titanium has pioneered rapid quenching techniques to produce large‑scale zirconium‑based BAA with superior glass‑forming ability. Their alloys achieve up to 30% higher tensile strength than conventional steel while maintaining comparable conductivity.

Sustainability Initiatives:

- Investing in energy‑efficient melt‑spinning lines

- Reducing CO₂ emissions by 25% per ton of alloy produced

- Developing recyclable alloy streams for end‑of‑life components

9️⃣ 9. Hitachi Metals, Ltd.

Headquarters: Tokyo, Japan

Key Offering: Palladium‑based amorphous alloys for high‑frequency electronic inductors

Hitachi Metals focuses on precision manufacturing of thin‑film BAA to meet the stringent requirements of semiconductor and sensor industries.

Sustainability Initiatives:

- Utilising renewable energy in alloy production

- Implementing closed‑loop water recycling systems

- Partnering with universities for alloy lifecycle studies

8️⃣ 8. Nanophase Technologies Corporation

Headquarters: San Diego, USA

Key Offering: Zirconium‑based BAA for transformer cores and energy storage devices

Nanophase Technologies has commercialised a scalable melt‑spinning process that reduces production costs by 15% while preserving high glass‑forming ability.

Sustainability Initiatives:

- Adopting low‑energy rapid quenching techniques

- Providing life‑cycle assessment tools for customers

- Investing in research for biodegradable alloy components

7️⃣ 7. Umicore S.A.

Headquarters: Brussels, Belgium

Key Offering: Iron‑based amorphous alloys for transformer cores and magnetic shielding

Umicore leverages its expertise in metal‑based catalysis to develop cost‑effective BAA with high magnetic permeability.

Sustainability Initiatives:

- Reducing energy consumption by 10% per ton of alloy

- Implementing zero‑waste manufacturing processes

- Collaborating with energy utilities for grid optimisation studies

6️⃣ 6. Carpenter Technology Corporation

Headquarters: Detroit, USA

Key Offering: Zirconium‑based BAA for aerospace and defence applications

Carpenter Technology provides high‑strength, low‑weight components for aircraft engines and missile systems.

Sustainability Initiatives:

- Investing in carbon‑neutral production facilities

- Developing alloy recycling programmes for aerospace components

- Partnering with defence agencies on lightweight material research

5️⃣ 5. Alcoa Corporation

Headquarters: Pittsburgh, USA

Key Offering: Aluminium‑based amorphous alloys for lightweight structural applications

Alcoa’s research focuses on integrating BAA into aluminium matrix composites to enhance strength without compromising weight.

Sustainability Initiatives:

- Reducing greenhouse gas emissions by 20% per ton of alloy

- Investing in renewable energy for smelting operations

- Developing closed‑loop recycling for aluminium‑BAA composites

4️⃣ 4. General Electric

Headquarters: Boston, USA

Key Offering: Iron‑based BAA for power generation turbines and generators

GE applies BAA to reduce core losses in large‑scale generators, improving overall plant efficiency.

Sustainability Initiatives:

- Deploying BAA in renewable energy projects

- Reducing material waste by 30% through precision casting

- Collaborating with research institutes on high‑temperature BAA development

3️⃣ 3. Bosch Group

Headquarters: Stuttgart, Germany

Key Offering: Zirconium‑based BAA for automotive sensors and electric vehicle components

Bosch is integrating BAA into electric motor housings and sensor housings to achieve weight reduction and higher durability.

Sustainability Initiatives:

- Using renewable energy in alloy production lines

- Reducing lifecycle CO₂ emissions by 15% per component

- Partnering with automotive OEMs on lightweight material strategies

2️⃣ 2. Samsung Advanced Institute of Technology

Headquarters: Suwon, South Korea

Key Offering: Palladium‑based BAA for high‑frequency electronics and micro‑devices

Samsung’s BAA research focuses on ultra‑thin, high‑performance components for next‑generation consumer electronics.

Sustainability Initiatives:

- Investing in low‑energy alloy processing

- Reducing water usage by 25% in production facilities

- Developing recyclable electronic device components

1️⃣ 1. Mitsubishi Materials Corporation

Headquarters: Tokyo, Japan

Key Offering: Zirconium‑based BAA for aerospace and high‑temperature applications

Mitsubishi Materials is advancing BAA for turbine blades and high‑temperature structural components.

Sustainability Initiatives:

- Reducing energy consumption by 12% per ton of alloy

- Implementing zero‑waste production processes

- Collaborating with energy companies on high‑temperature BAA research

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/264718/global-bulk-amorphoalloy-market

Get Full Report Here: https://www.24chemicalresearch.com/reports/264718/global-bulk-amorphoalloy-market

🌍 Outlook: The Future of Bulk AmorphoAlloy Market

The Bulk AmorphoAlloy Market is poised for robust growth, driven by the convergence of energy‑efficiency demands, advanced material science, and global infrastructure modernization. With a projected CAGR of 19.65% from 2025 to 2034, the market is expected to expand as industries seek materials that combine high strength, low weight, and superior corrosion resistance.

📈 Key Trends Shaping the Market:

- Rapid adoption of zirconium‑based alloys in transformer cores and aerospace components.

- Expansion of BAA applications in renewable energy infrastructure, including wind turbine gearboxes and solar inverters.

- Growth of BAA‑based biomedical devices such as bone replacements and smart stents.

- Increased focus on sustainability, with manufacturers reducing energy consumption and promoting recycling.

- Emerging digitalisation of supply chains and performance monitoring for BAA components.

- Top 10 Companies in the Diethyl Sulfide Market (2026): Market Leaders Shaping Global Chemical Supply - August 8, 2026

- Top 10 Companies in the Waterstop Market (2026): Market Leaders Driving Infrastructure Waterproofing - August 8, 2026

- Top 10 Companies in the All-Inorganic CsPbBr3 Perovskite LED Blue 90% Quantum Yield Market (2026): Market Leaders Powering Advanced Display Technologies - August 8, 2026