MARKET INSIGHTS

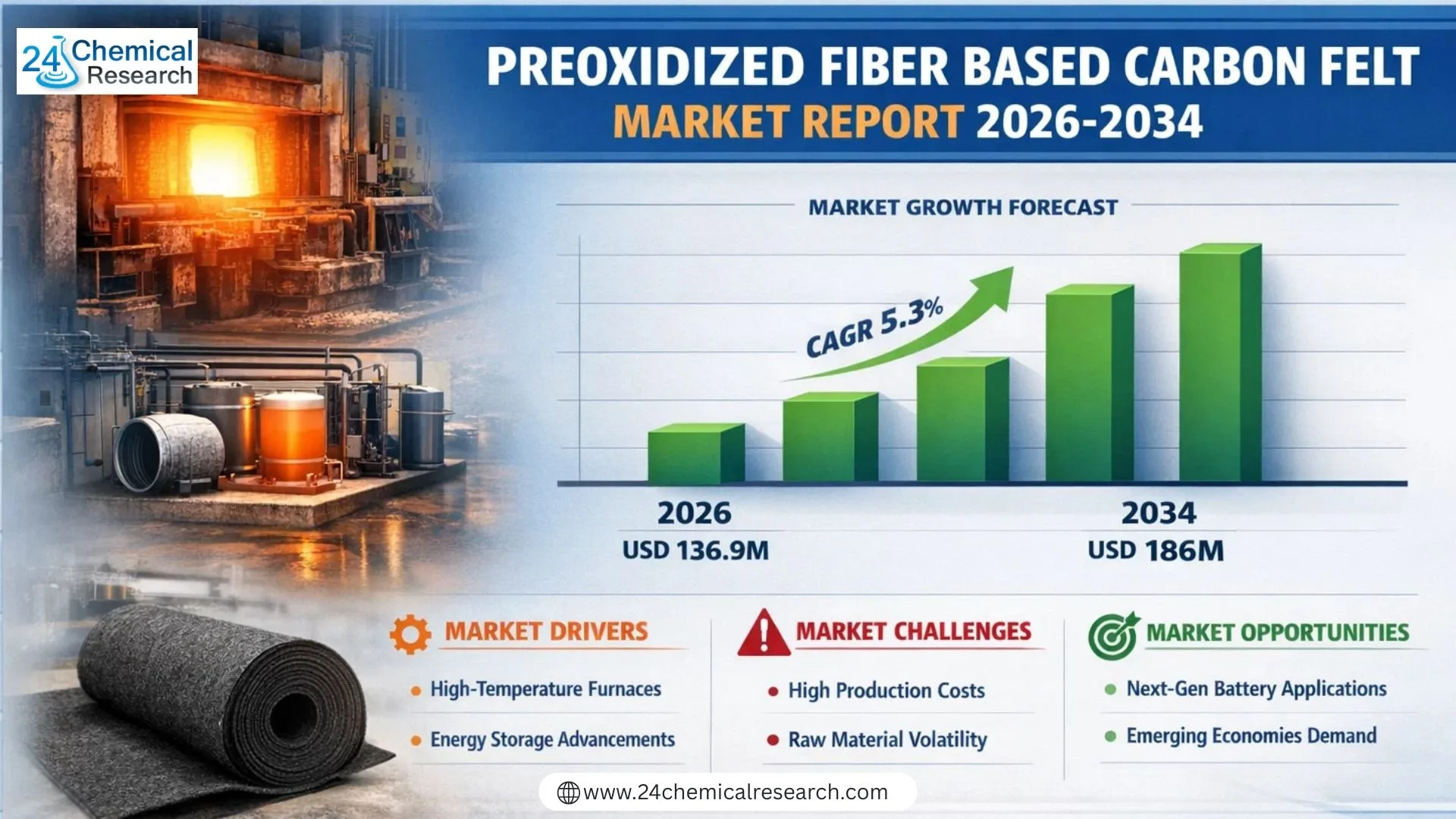

Global preoxidized fiber-based carbon felt market was valued at USD 130 million in 2025. The market is projected to grow from USD 136.9 million in 2026 to USD 186 million by 2034, exhibiting a compound annual growth rate (CAGR) of 5.3% during the forecast period.

Pre-oxidized fiber-based carbon felt is a high-performance engineered material produced from precursor fibers, primarily polyacrylonitrile (PAN), which undergo a critical thermal stabilization process known as pre-oxidation. This process fundamentally alters the fiber's molecular structure, creating a thermally stable, ladder-like configuration that provides exceptional heat resistance and flame retardancy. This intermediate material is essential, serving as the foundational precursor for manufacturing high-grade carbon felt through subsequent carbonization, which further enhances its properties for demanding applications.

The market growth is primarily driven by increasing demand from the industrial and electronics sectors, where the material's superior thermal insulation, chemical inertness, and mechanical stability are critical. Furthermore, advancements in manufacturing technologies and the expansion of high-temperature industrial processes are contributing to market expansion. The market is characterized by the presence of key global players such as SGL Carbon, AvCarb, and Toray, who continue to innovate and expand their product portfolios to meet evolving industry requirements.

Preoxidized Fiber-Based Carbon Felt Market – View in Detailed Research Report

Preoxidized fiber-based carbon felt is the cornerstone of advanced thermal management solutions across high-temperature industrial processes, advanced filtration systems, and next-generation energy storage technologies. Its unique combination of heat resistance, flame retardancy, chemical inertness, and mechanical robustness makes it indispensable for modern high-tech applications.

MARKET DRIVERS

Robust Demand from High-Temperature Industrial Furnaces

The primary driver for the preoxidized fiber-based carbon felt market is its critical role as thermal insulation material in high-temperature industrial applications. These felts offer exceptional thermal stability, low thermal conductivity, and excellent resistance to thermal shock, making them indispensable in metallurgical, semiconductor, and crystal growth furnaces operating above 1000°C. The expanding manufacturing base in these sectors, particularly in the Asia-Pacific region, directly fuels consumption.

Advancements in Energy Storage Technologies

The global push towards clean energy is significantly boosting the market. Preoxidized fiber-based carbon felt serves as a key electrode material in vanadium redox flow batteries (VRFBs), a promising technology for large-scale energy storage. The growing deployment of renewable energy sources like solar and wind, which require efficient storage solutions to manage intermittency, is creating substantial demand for VRFBs and their components.

➤ Material performance is paramount; the preoxidation stage crucially determines the final carbon fiber's microstructure, directly impacting the felt's mechanical strength and electrical conductivity in end-use applications.

Furthermore, the material's use in advanced filtration systems for corrosive chemicals and hot gases presents a steady growth avenue. Its chemical inertness and high-temperature durability make it superior to many alternative filtering media in harsh industrial environments.

MARKET CHALLENGES

High Production Costs and Raw Material Price Volatility

A significant challenge facing the market is the relatively high cost of production. The manufacturing process for preoxidized fiber-based carbon felt is energy-intensive, involving precise stabilization (preoxidation) and carbonization stages. Fluctuations in the prices of precursor materials, primarily polyacrylonitrile (PAN), directly impact profit margins for manufacturers and the final product's cost, which can deter price-sensitive customers.

Other Challenges

Technical and Performance Limitations

While excellent for insulation, the material's mechanical strength can be lower than that of rigid carbon-carbon composites, limiting its use in structural applications under heavy load. Achieving consistent density and uniformity across large felt panels also remains a technical hurdle for producers.

Competition from Alternative Materials

The market faces competition from other high-temperature insulation materials like ceramic fibers and graphite foams, which can offer comparable performance in certain temperature ranges, often at a lower cost, pressuring the adoption of carbon felt.

MARKET RESTRAINTS

Stringent Environmental and Workplace Safety Regulations

The production process of carbon materials, including preoxidized fiber, is subject to increasingly strict environmental regulations concerning emissions and waste management. Furthermore, handling the fine fibers requires stringent workplace safety measures to prevent inhalation, adding to operational compliance costs. These regulations can slow down the establishment of new production facilities and increase overhead for existing ones.

Capital-Intensive Nature of End-Use Industries

The growth of the market is intrinsically linked to capital expenditure in its key end-use sectors, such as steel, aerospace, and large-scale energy storage. Economic downturns or reduced investment in these capital-intensive industries can lead to project delays or cancellations, directly restraining the demand for high-performance materials like preoxidized carbon felt.

MARKET OPPORTUNITIES

Expansion in Next-Generation Battery Applications

Beyond VRFBs, there is significant R&D focus on utilizing carbon felt in other emerging battery chemistries, such as zinc-bromine flow batteries and even certain lithium-based systems. The unique porous structure of the felt provides an ideal scaffold for electrochemical reactions, opening up a vast potential market as energy storage technology evolves.

Development of Composite and Hybrid Materials

A key opportunity lies in the development of composite materials that combine carbon felt with polymers, ceramics, or other carbon forms. These hybrids can enhance specific properties like abrasion resistance, oxidation protection, or catalytic activity, creating tailored solutions for niche applications in aerospace, automotive, and chemical processing industries, thereby commanding premium prices.

Geographical Market Penetration

There is substantial potential for market growth in emerging economies where industrial modernization and energy infrastructure development are accelerating. Establishing local manufacturing partnerships or distribution networks in regions like Southeast Asia, Latin America, and the Middle East can capture new demand as these regions increase their investment in high-tech manufacturing and renewable energy projects.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Polyacrylonitrile-based felt dominates the market as it serves as the most prevalent precursor material, offering an optimal balance of mechanical strength, thermal stability, and processability which makes it highly suitable for the demanding carbonization process. This segment benefits from the well-established supply chain for PAN fibers and the extensive manufacturing experience that yields consistent, high-performance felt products. The material's superior ability to form a stable ladder-like structure during pre-oxidation is a key qualitative advantage that underpins its market leadership. |

| By Application |

|

Industrials represent the most significant application area, driven by the material's critical function as high-temperature insulation in furnaces, as a key component in advanced filtration systems for corrosive environments, and within chemical processing equipment. The high thermal resistance and chemical inertness of the felt are paramount for these demanding industrial applications. Its versatility also extends to use as reinforcement in composites and in specialized thermal management solutions, making it an indispensable material across heavy industries where durability under extreme conditions is a non-negotiable requirement. |

| By End User |

|

Metal and Glass Manufacturing is a leading end-user segment due to the extensive use of high-temperature industrial furnaces that require reliable and efficient insulation linings. The material's ability to withstand prolonged exposure to intense heat while maintaining structural integrity is critical for energy efficiency and process stability in melting, heat treatment, and sintering operations. The growing focus on advanced materials processing and energy conservation in these industries further solidifies the demand for high-performance preoxidized fiber-based carbon felt, positioning this segment for sustained relevance. |

| By Form Factor |

|

Rolls and Sheets constitute the most commonly supplied form factor, prized for their unparalleled versatility and ease of integration into various manufacturing and construction processes. This format allows for straightforward cutting and shaping on-site to fit complex furnace linings, insulation layers, and composite tooling. The flexibility of rolls facilitates transportation and storage, while the standardized dimensions of sheets provide consistency for engineers and fabricators. The adaptability of this form factor to a wide range of thicknesses and densities makes it the foundational product shape that caters to the broadest set of application requirements. |

| By Performance Grade |

|

High-Temperature Grade is a critical performance segment, specifically engineered to deliver exceptional thermal stability and resistance to oxidation at extreme temperatures encountered in advanced industrial processes. This grade is characterized by a carefully controlled pre-oxidation and carbonization process that maximizes the material's ability to perform in environments where standard grades would rapidly degrade. It is the preferred choice for the most demanding applications in semiconductor manufacturing, specialized metallurgy, and aerospace components, where failure is not an option. The development of these advanced grades reflects the market's push towards higher efficiency and reliability in extreme-condition applications. |

Key Industry Players

-

SGL Carbon (Germany)

-

Toray Industries, Inc. (Japan)

-

Mitsubishi Chemical Corporation (Japan)

-

AvCarb (United States)

-

CAPLINQ (International)

-

TANJI (China)

-

MIGE NEW MATERIAL (China)

-

FLYING (China)

-

PUXIANG (China)

-

TIANFU (China)

Top 10 Companies in the Preoxidized Fiber-Based Carbon Felt Market (2026)

10️⃣ 1. SGL Carbon

Headquarters: Dresden, Germany

Key Offering: High-performance carbon fibers, carbon felt, graphite electrodes

SGL Carbon is a global leader in carbon-based solutions, providing a broad portfolio of high-grade carbon materials for aerospace, energy storage, and high-temperature industrial applications. Their carbon felt products are engineered for maximum thermal resistance and structural integrity, making them ideal for furnace linings and advanced filtration systems.

Sustainability & Growth Initiatives:

- Investments in carbon-neutral production processes

- Partnerships with renewable energy projects to supply electrode materials

- R&D focus on low-temperature carbonization techniques to reduce energy consumption

9️⃣ 2. Toray Industries, Inc.

Headquarters: Tokyo, Japan

Key Offering: Advanced carbon fibers, carbon felt, composite materials

Toray combines cutting-edge materials science with large-scale manufacturing to deliver high-performance carbon felt for aerospace, automotive, and energy storage sectors. Their focus on lightweight, high-temperature materials supports the development of next-generation batteries and high-efficiency furnaces.

Sustainability & Growth Initiatives:

- Development of bio-based PAN fibers for sustainable carbon felt

- Strategic alliances with battery manufacturers for VRFB components

- Commitment to reducing CO₂ emissions in production facilities

8️⃣ 3. Mitsubishi Chemical Corporation

Headquarters: Tokyo, Japan

Key Offering: Carbon fibers, carbon felt, specialty chemicals

Mitsubishi Chemical supplies high-grade carbon felt for industrial furnaces and advanced filtration systems. Their integrated R&D and manufacturing capabilities allow rapid scaling to meet growing demand in the energy storage and metallurgy sectors.

Sustainability & Growth Initiatives:

- Investment in green chemistry for PAN production

- Partnerships with steel manufacturers to reduce furnace energy consumption

- Expansion of VRFB electrode supply chains

7️⃣ 4. AvCarb

Headquarters: Cleveland, USA

Key Offering: Carbon felt for fuel cells, batteries, and high-temperature industrial applications

AvCarb focuses on niche applications such as fuel cell electrodes and high-temperature insulation for industrial processes. Their products are known for high purity and consistent electrical conductivity, essential for large-scale energy storage solutions.

Sustainability & Growth Initiatives:

- Collaboration with U.S. energy companies to supply VRFB electrodes

- Research into recyclable carbon felt components

- Investment in advanced manufacturing technologies to lower production costs

6️⃣ 5. CAPLINQ

Headquarters: Singapore

Key Offering: Carbon felt for aerospace, automotive, and energy storage sectors

CAPLINQ specializes in high-temperature carbon felt for aerospace and automotive components, providing lightweight, thermally stable solutions for critical systems such as brake pads and turbine blades.

Sustainability & Growth Initiatives:

- Partnerships with automotive OEMs to reduce vehicle weight

- Development of low-emission production processes

- Expansion into emerging markets in Southeast Asia

5️⃣ 6. TANJI

Headquarters: Shanghai, China

Key Offering: Carbon felt for industrial furnaces and filtration systems

TANJI is a leading Chinese manufacturer of high-performance carbon felt, serving the rapidly expanding steel and metallurgy industries in Asia. Their products are tailored for extreme temperature environments and high-precision applications.

Sustainability & Growth Initiatives:

- Investment in energy-efficient pre-oxidation facilities

- Collaboration with Chinese steel mills to reduce furnace energy consumption

- Expansion of product lines to include high-purity grades for batteries

4️⃣ 7. MIGE NEW MATERIAL

Headquarters: Guangzhou, China

Key Offering: Carbon felt for industrial and energy storage applications

MIGE NEW MATERIAL focuses on delivering cost-competitive, high-quality carbon felt to the Chinese market, with a strong emphasis on process optimization and yield improvement.

Sustainability & Growth Initiatives:

- Implementation of waste heat recovery systems in production plants

- R&D on low-cost PAN alternatives

- Strategic alliances with local steel manufacturers

3️⃣ 8. FLYING

Headquarters: Shenzhen, China

Key Offering: Carbon felt for high-temperature industrial processes

FLYING supplies high-performance carbon felt for industrial furnaces and advanced filtration systems, focusing on large-scale production to meet the demands of the Chinese and ASEAN markets.

Sustainability & Growth Initiatives:

- Adoption of renewable energy sources for plant operations

- Development of high-temperature grades for aerospace applications

- Expansion of production capacity in China and Vietnam

2️⃣ 9. PUXIANG

Headquarters: Wuhan, China

Key Offering: Carbon felt for industrial furnaces and energy storage

PUXIANG offers a range of carbon felt products for high-temperature industrial furnaces and VRFB electrode manufacturing, with a focus on high purity and consistent performance.

Sustainability & Growth Initiatives:

- Collaboration with battery manufacturers to supply electrode substrates

- Investments in carbon recycling programs

- Optimization of pre-oxidation energy consumption

1️⃣ 10. TIANFU

Headquarters: Chengdu, China

Key Offering: Carbon felt for high-temperature industrial and aerospace applications

TIANFU is a key supplier of carbon felt for high-temperature industrial processes, focusing on lightweight, high-performance materials for aerospace and defense sectors.

Sustainability & Growth Initiatives:

- Partnerships with aerospace OEMs to reduce component weight

- Investment in low-energy carbonization technologies

- Expansion into international markets through joint ventures

Download FREE Sample Report: Preoxidized Fiber-Based Carbon Felt Market – View in Detailed Research Report

Get Full Report: Preoxidized Fiber-Based Carbon Felt Market – View in Detailed Research Report

Outlook: The Future of Preoxidized Fiber-Based Carbon Felt

The preoxidized fiber-based carbon felt market is poised for sustained growth, driven by the expansion of high-temperature industrial processes, the shift towards clean energy, and the increasing demand for advanced filtration media. With a projected CAGR of 5.3%, the market will continue to expand as new applications in energy storage, aerospace, and automotive industries emerge.

Future Trends

- Integration of bio-based PAN fibers to reduce carbon footprint and production costs.

- Advancement of composite hybrids combining carbon felt with polymers and ceramics for enhanced mechanical and thermal properties.

- Growth of next-generation flow battery chemistries (zinc-bromine, lithium-based) requiring tailored carbon felt substrates.

- Expansion into emerging markets such as Southeast Asia, Latin America, and the Middle East, driven by industrial modernization and renewable energy infrastructure.

- Increased focus on digital manufacturing and process optimization to improve yield, reduce energy consumption, and lower production costs.

- Top 10 Companies in the Metal Concrete Fibers Market (2026): Market Leaders Powering Global Infrastructure - July 22, 2026

- Top 10 Companies in the Inorganic Biocompatible Materials Market (2026): Market Leaders Powering Global Innovation - July 22, 2026

- Top 10 Companies in the Global Dimming Glass Market (2026): Market Leaders Powering Smart Building Innovation - July 22, 2026