MARKET INSIGHTS

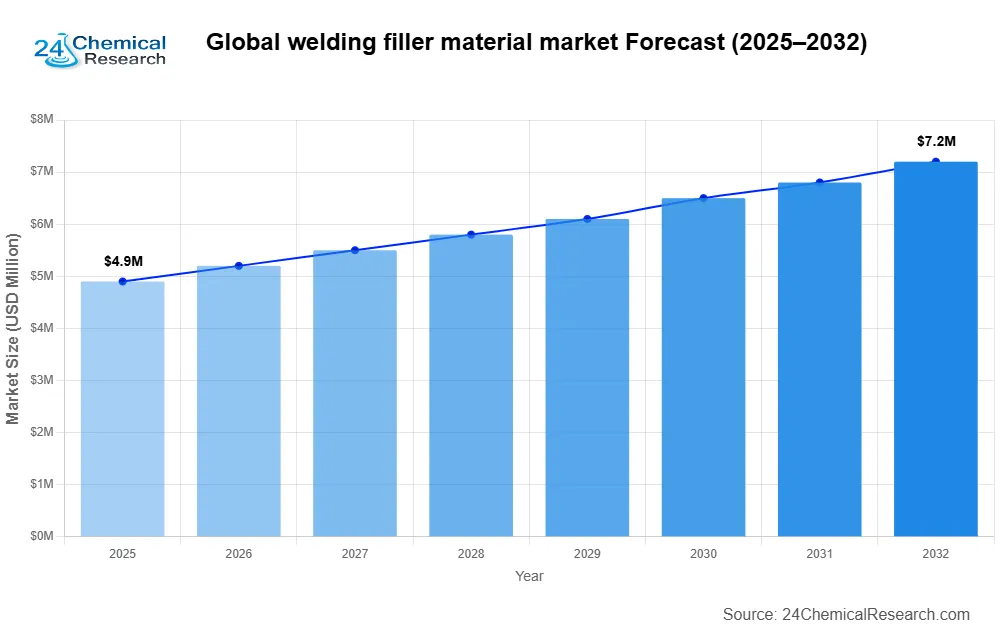

Global welding filler material market size was valued at USD 4.89 billion in 2024 and is projected to reach USD 7.23 billion by 2032, exhibiting a CAGR of 5.7% during the forecast period.

Welding filler materials are essential consumables used to join metal components by melting and fusing them together. These materials include welding wires, rods, and gases that enhance structural integrity and corrosion resistance in joints. The primary types of welding fillers are solid wires, flux-cored wires, stick electrodes, and shielding gases, each suited for specific applications across industries.

Market growth is driven by increasing construction activities and infrastructure development worldwide, particularly in emerging economies. The automotive and transportation sectors also contribute significantly due to rising demand for lightweight vehicle components. However, the market faces challenges from volatile raw material prices and stringent environmental regulations. Key players like Lincoln Electric, Illinois Tool Works, and Air Liquide dominate the industry through continuous product innovation and strategic acquisitions.

MARKET DYNAMICS

MARKET DRIVERS

Surge in Infrastructure Development Projects Accelerating Demand for Welding Solutions

Global welding filler material market is experiencing robust growth driven by accelerating infrastructure development across emerging economies. With construction activity projected to grow at 3-5% annually through 2030, demand for specialized welding consumables continues to rise. Major infrastructure initiatives like China's Belt and Road projects and India's National Infrastructure Pipeline are driving unprecedented demand for structural welding materials, particularly flux-cored wires and submerged arc welding consumables.

Advancements in Automotive Manufacturing Boosting Welding Material Adoption

The automotive sector's shift toward lightweight materials presents significant opportunities for welding filler innovations. As vehicle manufacturers increasingly adopt aluminum and advanced high-strength steels to meet stringent emissions standards, specialty filler metals capable of joining dissimilar materials are becoming indispensable. The transition to electric vehicles further fuels demand, with battery pack assembly requiring precise joining techniques that utilize sophisticated filler materials.

The growing emphasis on automation in automotive production also drives adoption of specialized welding wires optimized for robotic welding systems. These trends are particularly pronounced in North America and Europe, where automotive OEMs are investing heavily in next-generation manufacturing facilities.

Energy Sector Investments Creating Sustained Demand

Global energy infrastructure expansion, particularly in renewable energy and oil & gas sectors, continues to drive welding filler material consumption. Offshore wind farm construction requires corrosion-resistant filler metals capable of withstanding harsh marine environments. Similarly, pipeline projects across North America and the Middle East consume substantial quantities of specialized welding consumables designed for high-pressure applications. The transition to cleaner energy sources has increased demand for welding materials by approximately 18% in the power generation sector since 2020. As countries invest in energy security and transition initiatives, the requirement for high-performance welding consumables in critical infrastructure applications shows no signs of slowing down.

MARKET RESTRAINTS

Volatility in Raw Material Prices Disrupting Market Stability

The welding filler material market faces significant challenges from fluctuating raw material costs, particularly for nickel, chromium, and manganese alloys. These price variations create margin pressures for manufacturers and unpredictability for end-users. Recent geopolitical tensions and supply chain disruptions have exacerbated this situation, with some specialty alloy prices experiencing swings of up to 35% within single quarters.

Additional Constraints

Environmental Regulations

Increasingly stringent environmental regulations regarding fume emissions and hazardous material content are forcing manufacturers to reformulate products and invest in cleaner production technologies. Compliance costs for meeting new standards in regions like the EU and North America can amount to 8-12% of production expenses.

Trade Barriers

Protectionist trade policies and anti-dumping duties in key markets create artificial supply constraints and price disparities. These measures particularly impact international trade of stainless steel and nickel-based filler metals, limiting market access for some manufacturers.

MARKET CHALLENGES

Skilled Labor Shortage Threatening Industry Growth Potential

The welding industry faces a critical shortage of certified welders worldwide, with current workforce levels meeting only about 65% of industry demand. This deficit threatens to constrain market growth as manufacturers struggle to find personnel qualified to work with advanced filler materials and automated welding systems. The skills gap is particularly acute in developed markets where experienced welders are retiring faster than new workers enter the field.

Technological Adaptation Challenges

Small and medium-sized fabricators often lack the capital to upgrade equipment needed for advanced filler metal applications. This creates a two-tier market where only large corporations can fully leverage next-generation welding materials, limiting overall market penetration.

MARKET OPPORTUNITIES

Digital Transformation and Smart Manufacturing Creating New Value Propositions

The integration of Industry 4.0 technologies presents significant opportunities for welding filler material suppliers. Smart filler metals embedded with traceability markers enable digital quality assurance throughout the welding process. This innovation is gaining traction in aerospace and nuclear applications where documentation requirements are most stringent.

Investment in R&D for next-generation materials continues to accelerate, with particular focus on cold metal transfer technologies and ultra-low hydrogen electrodes. These developments address critical industry needs while creating premium product segments with higher margins.

Emerging applications in additive manufacturing also show promise, with specialized welding wires being adapted for directed energy deposition processes. This convergence of welding and 3D printing technologies could unlock new market segments worth an estimated $1.2 billion by 2028.

Segment Analysis:

By Type

Welding Wire Segment Dominates Due to Its Versatility and High Demand Across Industries

The market is segmented based on type into:

-

Welding Wire

-

Welding Rod

-

Filling Gas

-

Others

By Application

Building Construction Segment Leads Due to Rising Infrastructure Development Globally

The market is segmented based on application into:

-

Building Construction

-

Heavy Industrial

-

Transport

-

Other

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Invest in Innovation to Maintain Competitive Edge

Global welding filler material market exhibits a moderately consolidated structure, with established multinational corporations competing alongside regional specialists. Lincoln Electric currently dominates the sector, holding approximately 18% of the global market share in 2024. This leadership position stems from their comprehensive product portfolio spanning welding wires, rods and gases, coupled with an extensive distribution network across 50+ countries.

Illinois Tool Works and Air Liquide follow closely, collectively accounting for nearly 25% of market revenues. These industry giants benefit from vertical integration strategies, controlling everything from raw material sourcing to final product distribution. Their technical expertise in developing advanced alloys for specialized applications (particularly in aerospace and energy sectors) gives them a distinct competitive advantage.

Meanwhile, Asian manufacturers like FAR EAST ALLOY and Tianjin Bridge Welding Materials are gaining traction through cost-competitive strategies and expanding production capacities. The Chinese market alone witnessed seven new manufacturing facilities opening in 2023, signaling aggressive regional growth.

Recent market developments highlight strategic shifts across the sector:

- Lincoln Electric's $150 million investment in automated wire production lines (Q3 2023)

- The Linde Group's acquisition of three regional gas suppliers to strengthen filler gas distribution

- EWM's launch of next-generation flux-cored wires for underwater welding applications

These moves indicate that the market is entering an innovation-driven growth phase, with companies prioritizing both technological advancement and geographical expansion to capture market share in this $4.89 billion industry projected to grow at 5.7% CAGR through 2032.

List of Key Welding Filler Material Companies Profiled

-

Lincoln Electric (U.S.)

-

Illinois Tool Works (U.S.)

-

Air Liquide (France)

-

The Linde Group (Germany)

-

Praxair Incorporated (U.S.)

-

EWM (Germany)

-

FAR EAST ALLOY (China)

-

Yiyan Machinery (China)

-

North Seiko Welding Material (Japan)

-

Tianjin Bridge Welding Materials (China)

-

Leigong Welding Alloys (China)

-

Yingsheng Hanjiecailiao (China)

-

Xooz Machinery Equipment (China)

📈 Top 10 Companies in the Welding Filler Material Market (2026)

🔟 1. Lincoln Electric

Headquarters: Cleveland, Ohio, USA

Key Offering: Welding wires, rods, gases for industrial, automotive, and aerospace sectors

Lincoln Electric has long been a benchmark in welding consumables, delivering high-performance products that meet stringent quality and safety standards. Their portfolio spans MIG, TIG, and flux-cored solutions, enabling precise, high-speed welding across diverse applications.

Sustainability Initiatives:

- Investment in low-emission welding technologies

- Partnerships with automotive OEMs to reduce vehicle weight

- Continuous R&D for eco-friendly filler alloys

9️⃣ 2. Illinois Tool Works

Headquarters: Chicago, Illinois, USA

Key Offering: Flux-cored wires, solid wires, and specialized electrodes for heavy industry and construction

Illinois Tool Works leverages its integrated manufacturing ecosystem to deliver cost-effective, high-quality welding consumables. The company focuses on scalable solutions for large-scale infrastructure projects and heavy-duty applications.

Sustainability Initiatives:

- Optimizing production for reduced energy consumption

- Collaboration with construction firms to use lightweight welding solutions

- Development of recyclable electrode materials

8️⃣ 3. Air Liquide

Headquarters: Paris, France

Key Offering: High-purity shielding gases and specialty alloys for aerospace and energy sectors

Air Liquide provides essential gas solutions that enhance weld quality and corrosion resistance. Their focus on advanced gas blends supports high-temperature and marine environments.

Sustainability Initiatives:

- Reduction of CO2 emissions in gas production

- Investment in renewable gas technologies

- Support for green energy infrastructure projects

7️⃣ 4. The Linde Group

Headquarters: Neuss, Germany

Key Offering: Specialized gases and welding consumables for high-performance applications

The Linde Group combines gas expertise with welding technology to deliver solutions that meet stringent industrial standards, particularly in automotive and aerospace.

Sustainability Initiatives:

- Energy-efficient gas manufacturing

- Partnerships for low-emission welding processes

- Research into bio-based gas alternatives

6️⃣ 5. Praxair Incorporated

Headquarters: Chicago, Illinois, USA

Key Offering: High-purity gases and advanced welding consumables for industrial and marine applications

Praxair supports critical sectors with reliable gas solutions that improve weld integrity and reduce corrosion.

Sustainability Initiatives:

- Reduction of greenhouse gas emissions in gas production

- Investment in renewable energy for manufacturing plants

- Collaboration with marine operators for corrosion-resistant solutions

5️⃣ 6. EWM

Headquarters: Hannover, Germany

Key Offering: Flux-cored wires and specialized electrodes for automotive and industrial welding

EWM is recognized for its high-quality welding consumables that support precision and productivity in automotive manufacturing.

Sustainability Initiatives:

- Development of low-hydrogen electrodes

- Adoption of digital manufacturing processes

- Support for automotive lightweighting programs

4️⃣ 7. FAR EAST ALLOY

Headquarters: Shanghai, China

Key Offering: Cost-competitive welding rods and wires for construction and heavy industry

FAR EAST ALLOY expands its production capacity to meet growing demand in the rapidly developing Chinese market.

Sustainability Initiatives:

- Implementation of eco-friendly manufacturing processes

- Use of recyclable materials in electrode production

- Partnerships with local construction firms to promote sustainable welding

3️⃣ 8. Yiyan Machinery

Headquarters: Guangzhou, China

Key Offering: Welding machines and consumables tailored for small and medium enterprises

Yiyan Machinery focuses on providing affordable, high-performance solutions for SMEs, helping them adopt advanced welding technologies.

Sustainability Initiatives:

- Energy-efficient machine designs

- Support for local manufacturing through training programs

- Use of environmentally friendly materials in consumables

2️⃣ 9. North Seiko Welding Material

Headquarters: Tokyo, Japan

Key Offering: High-precision welding rods and wires for automotive and aerospace

North Seiko delivers premium welding consumables that meet the exacting standards of Japan’s automotive and aerospace industries.

Sustainability Initiatives:

- Investment in low-emission welding processes

- Research into advanced alloy compositions

- Collaboration with OEMs to reduce vehicle weight

1️⃣ 10. Tianjin Bridge Welding Materials

Headquarters: Tianjin, China

Key Offering: Specialized welding rods and flux-cored wires for bridge construction and heavy infrastructure

Tianjin Bridge Welding Materials supports large-scale infrastructure projects with robust, high-performance consumables.

Sustainability Initiatives:

- Adoption of green manufacturing practices

- Use of recyclable packaging for consumables

- Partnerships with engineering firms to promote sustainable construction

Download FREE Sample Report

Welding Filler Material Market – View in Detailed Research Report

🌍 Outlook: The Future of Welding Filler Materials

The welding filler material market is poised for steady expansion as global infrastructure projects, automotive electrification, and renewable energy initiatives continue to drive demand. Companies that invest in advanced alloys, automation, and digital traceability will capture significant market share, especially in high-growth regions such as Asia‑Pacific and North America.

📈 Future Trends Shaping the Market

- Accelerated adoption of automated welding systems across automotive and construction sectors

- Growth of additive manufacturing requiring specialized directed energy deposition wires

- Development of eco‑friendly, low‑hydrogen filler alloys to meet stringent environmental standards

- Integration of Industry 4.0 technologies for real‑time quality assurance and traceability

- Expansion of digital supply chains to streamline procurement and reduce lead times

- Top 10 Companies in the Global High Temperature Furnace Thermal Field Market (2026): Market Leaders Powering Global Industry - July 11, 2026

- Top 10 Companies in the Offshore Wind Turbine Monopile Market (2026): Market Leaders Powering Global Offshore Wind - July 11, 2026

- Top 10 Companies in the Russia Wood Pellets Market (2026): Market Leaders Driving Sustainable Heating - July 11, 2026